Veterinary Vaccines Market

Global Industry analysis, Size, Share, Growth, Trends, and Forecast 2026-2031

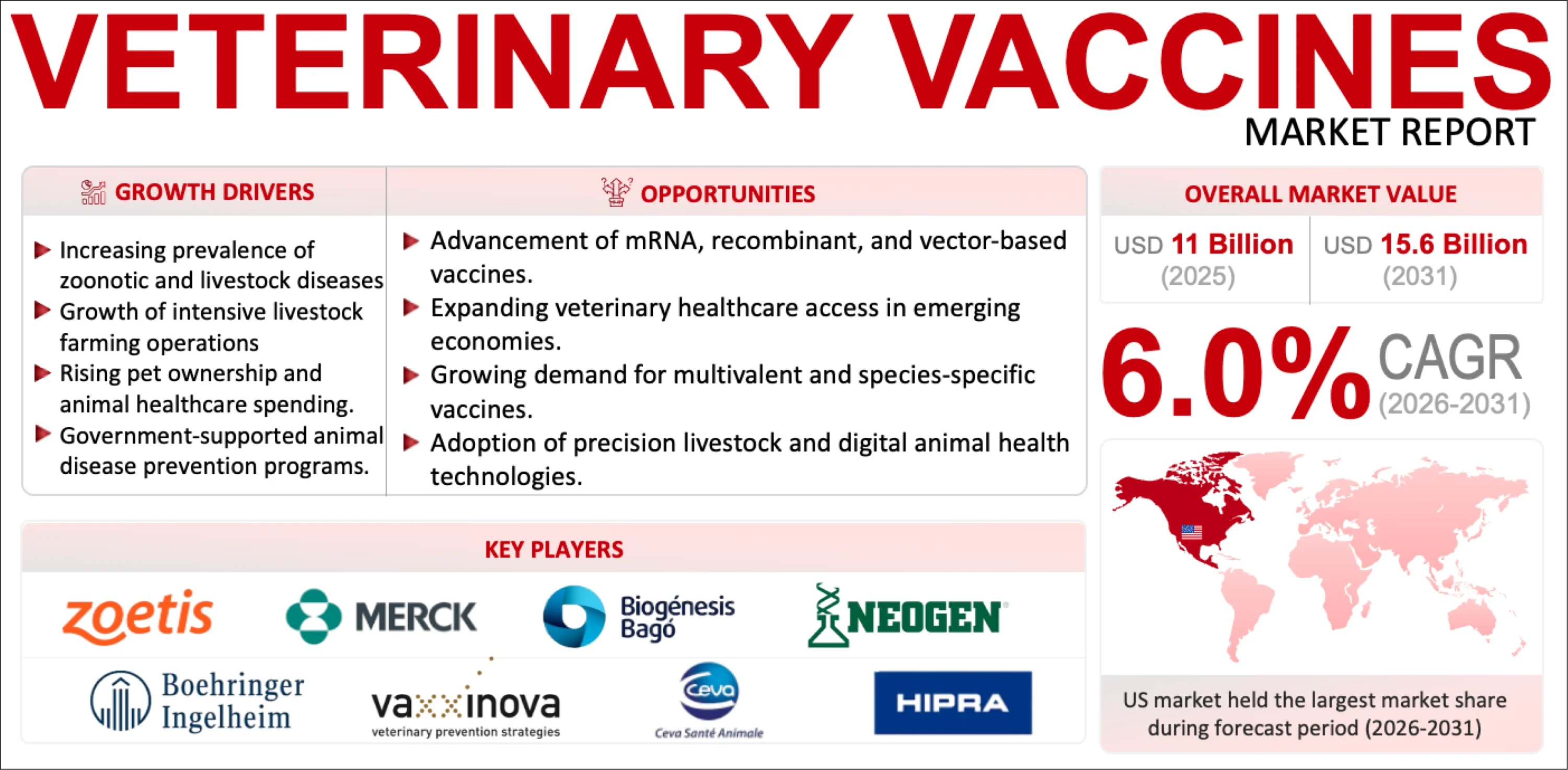

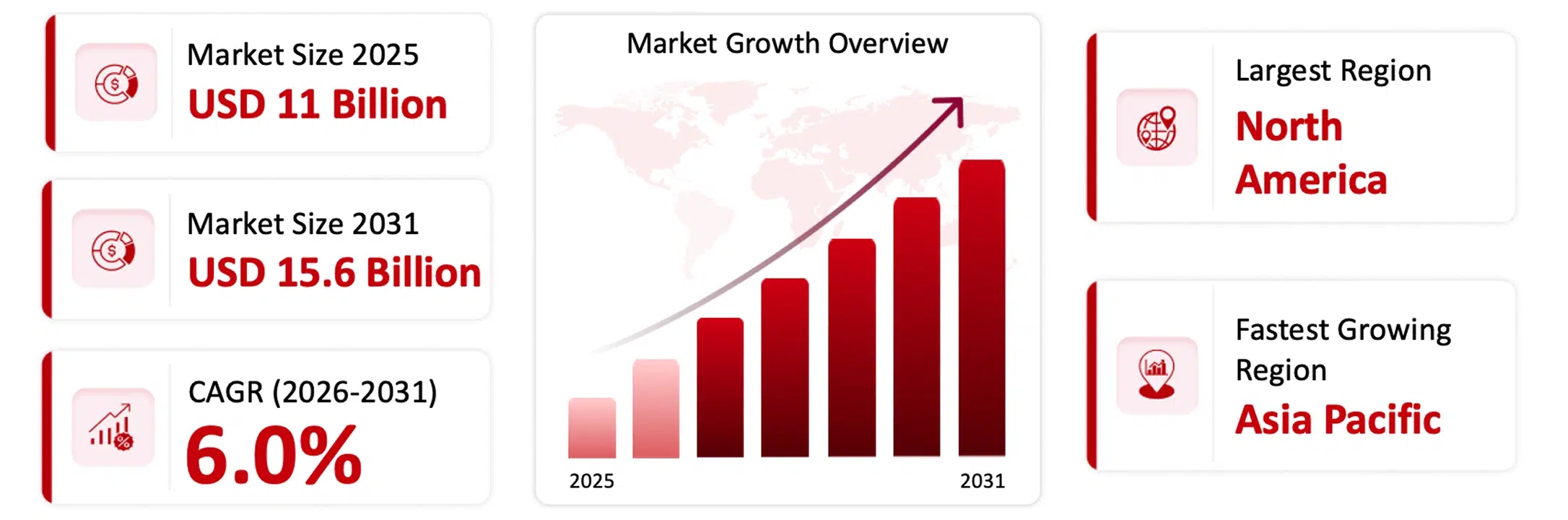

The Global Veterinary Vaccines Market is Projected to Reach USD 15.6 Billion by 2031, Growing at a CAGR of 6% During the Forecast Period.

| Market Size 2025 | Market Size 2031 | CAGR (2026-2031) | Largest Region | Fastest Growing Region |

|---|---|---|---|---|

| USD 11 billion | USD 15.6 billion | 6% | North America | Asia Pacific |

Market Overview

There has been a steady growth in the global veterinary vaccine market due to the following drivers: increasing concern for animal health, an increased number of zoonotic (animal-to-human) diseases, and the desire for better production of food from livestock and improved care of pets. More use of advanced technologies to produce and distribute veterinary vaccines (such as recombinant and DNA-based vaccines) and improvements to cold chain systems have allowed more veterinarians and farmers to use vaccines and encourage their clients to vaccinate their animals. Finally, various governments and organizations are promoting vaccine use with many new programs and increased education and outreach about the importance of preventive health care for animals, which has contributed to the continued growth of the veterinary vaccine industry in both developed and developing countries. The market was valued at USD 11 billion in 2025 and is projected to reach USD 15.6 billion by 2031, growing at a CAGR of 6% during the forecast period (2026-2031).

Technology Overview

Developments in the fields of recombinant DNA technology, live attenuated vaccine design, and adjuvants are contributing to greater safety, efficacy, and duration of protection provided by animal vaccines. Utilization of multivalent vaccines that provide protection against various animal diseases within a single shot can assist in the more effective management of diseases among livestock and companion animals. Besides, there have been developments in vaccines based on vectors, mRNA technologies, and thermally stable formulas that enhance the stability, efficacy, and efficiency of animal vaccination.

Increasing integration of animal health management through digital livestock monitoring systems and precision farming practices also provides a great advantage in implementing effective vaccination programs through early disease detection, herd health monitoring, and optimizing vaccination schedules.

Key Growth Drivers

- The rising occurrence of zoonotic diseases, such as avian influenza, foot-and-mouth disease, and swine fever, is fueling the requirement for successful veterinary vaccination programs worldwide.

- The rising number of pets, along with the growing concern about preventive healthcare for animals, is propelling the usage of companion animal vaccines in developed and developing countries.

- The ongoing innovations in recombinant vaccines, vectors, and multivalent vaccines are enhancing vaccine effectiveness, safety, and coverage among various animal species.

- The rising practice of commercial livestock production and growing emphasis on increasing animal productivity, food safety, and herd health management are boosting vaccine use in the livestock industry.

- Animal disease control programs, mandatory vaccination schemes, and investments in veterinary healthcare are contributing to market growth.

Veterinary Vaccines Market Key Highlights

Need deeper insights on this market?

Get full report access with detailed forecasts, competitive analysis, and segmentation.

Veterinary Vaccines Market Trends

With rising concern about animal wellness, food security, and prevention of zoonotic diseases, investments in the veterinary vaccines market are increasing substantially. Some important trends like the use of recombinant vaccines, vector vaccines, multivalent vaccines, mRNA vaccines, and thermostable vaccines are opening up newer avenues for growth within the field of livestock and companion animals’ health and well-being. Furthermore, the use of precision livestock farming methods, herd management systems, and preventative veterinary care has helped enhance the effectiveness of vaccination processes and other related measures. Prominent players operating within the veterinary vaccines market include names like Zoetis Inc., Merck & Co., Inc., Boehringer Ingelheim International GmbH, Elanco Animal Health Incorporated, and Ceva Santé Animale.

Veterinary Vaccines Industry Trends – Recombinant and Multivalent Vaccine Technologies

Improvements in recombinant DNA technology and multivalent vaccines are driving changes within the market for veterinary vaccines. Vaccines that can provide animals protection against different kinds of diseases after a single injection are being developed by manufacturers. In addition, recombinant vaccines and vectored vaccines are being employed by companies for the purpose of providing enhanced safety, effectiveness, and target-specificity benefits in poultry, pigs, cows, and pets.

A demand for mass protection from diseases, higher livestock production rates, and minimal use of antibiotics is spurring innovation among leading players like Zoetis Inc., Merck & Co., Inc., and Boehringer Ingelheim International GmbH. Next-generation vaccine technologies such as recombinant vaccines, mRNA vaccines, and intranasal vaccines are being developed by companies to help manage various diseases in animals.

Asia Pacific Veterinary Vaccines Market Trends Insights

The demand for veterinary vaccines is booming in Asia Pacific as countries’ economies are growing alongside the demand for livestock products. Countries such as China, India, Japan, and South Korea are seeing significant increases in poultry & dairy production, aquaculture, and swine farming contributing to the increase in demand for veterinary vaccines.

There is a greater awareness in the governments of the importance of vaccinating animals, in addition to having more food safety regulations; thereby increasing the demand for vaccination programs. Additionally, improvements in the veterinary health care infrastructure throughout Asia will provide new opportunities for manufacturers of veterinary vaccines, which also relates to the increasing adoption of preventative health care practices for animals in developing countries within Asia. Some of the major participants involved are Ceva Santé Animale, Elanco Animal Health Incorporated, and HIPRA, who are currently expanding their capabilities for manufacturing and selling veterinary vaccines in Asia Pacific.

Key Players in the Veterinary Vaccines Market

Leading companies in the veterinary vaccines market are focusing on innovation, strategic partnerships, and expansion of health-centric features to strengthen their market position.

Strategic Activities Within the Veterinary Vaccines Market

Hipra, S.A. (Spain) collaborated with Llamas Laboratories and Services (Argentina) strengthens its diagnostic service to improve animal health in Argentina. The main objective of this alliance is to strengthen and optimize the diagnostic service for animal production in Argentina. This will be achieved by expanding the range of locally available tests, increasing the value of results for decision-making, and reducing turnaround times, among other advantages.

Vaxxinova International B.V. (Netherlands) acquired the Avishield® poultry vaccine portfolio from Dechra Pharmaceuticals Limited (UK), along with Dechra’s poultry vaccine research and development team based in Zagreb, Croatia. This strategic acquisition enables Vaxxinova to expand its global footprint by adding a complete range of live vaccines for Infectious Bronchitis (IB), Gumboro Disease (IBD), and Newcastle Disease (ND) to its offerings.

Boehringer Ingelheim International GMBH (Germany) launched VAXXITEK® HVT+IBD+H5 is a new trivalent vaccine for poultry that offers protection against Marek’s disease, Infectious Bursal Disease and H5 avian influenza in just one shot. With VAXXITEK® HVT+IBD+H5, Boehringer Ingelheim is expanding its proven VAXXITEK® range with a new vaccine that protects against three severe poultry diseases: Marek’s disease, Infectious Bursal Disease, and H5 avian influenza.

Ceva Santé Animale (France) collaborated with Touchlight Genetics Limited (England) for the development and manufacture of new dbDNA vaccines and therapeutics across a broad range of animal health indications. The partnership brings together the world-leading development and commercialization capability of Ceva with Touchlight’s best-in-class dbDNA technology which enables rapid, high purity enzymatic DNA production and eliminates antibiotic resistance genes.

Veterinary Vaccines Market Insights

Growth in the market for veterinary vaccines is being driven by greater awareness about animal disease prevention, animal production efficiency, and the health of companion animals. There is an increased concern about zoonotic diseases and food safety as well.

Vaccines are commonly applied to livestock and companion animals in veterinary practice as a preventive measure against bacteria, viruses, and parasites. The important fields include poultry, cattle, swine, fish, and pets.

Growing livestock populations, increasing pet ownership, and rising awareness regarding preventive animal healthcare are major growth drivers for the market. Technological advancements in recombinant, vector-based, and multivalent vaccines are also improving vaccine effectiveness and disease coverage.

There has been significant growth in the markets of recombinant vaccines, thermostable vaccines, and precision vaccination techniques. Nevertheless, high development costs, stringent regulatory approval procedures, and cold chain logistics pose considerable barriers to market expansion.

Asia Pacific is likely to exhibit highest CAGR in the veterinary vaccines market owing to high livestock production, increase in the consumption of animal proteins, and animal disease management initiatives by government organizations. Countries including China, India, and Japan significantly contribute towards the growth of the regional market.

Veterinary Vaccines Market Dynamics

Drivers: Rising Prevalence of Animal Diseases Is Accelerating Veterinary Vaccine Adoption.

Rising cases of zoonotic diseases, bacteria, and viruses in farm and companion animals have spurred the need for veterinary vaccines across the world. With the rising concern for food security, livestock production, and preventive animal health care, farmers and pet owners are increasingly looking toward vaccinating their animals. Moreover, government disease control programs and increased commercial livestock farming are adding to market expansion.

Opportunities: Expansion of Advanced and Preventive Animal Healthcare Solutions

Rise in awareness about preventive vet care and innovations in recombinant vaccines, vector vaccines, and multi-valent vaccines are resulting in strong growth potential in the market. Higher pet ownership rates, higher protein consumption, and growth in aquaculture and poultry industry are contributing further to the growth in demand for vaccines.

Challenges: Stringent Regulations and Cold Chain Requirements Remain Key Barriers.

Regulatory approval and the prolonged duration of vaccine development remain barriers to market expansion. Moreover, the cost associated with cold chain maintenance is relatively high especially in rural and developing nations. In addition, high costs of research and development, as well as varying strains of diseases, pose difficulties for vaccine developers.

Technology and Market Insights

The global veterinary vaccines market is witnessing significant technological advancements driven by the increasing need for effective animal disease prevention, livestock productivity enhancement, and zoonotic disease control. Veterinary vaccines are increasingly incorporating advanced technologies such as recombinant DNA platforms, vector-based systems, and adjuvant innovations to improve immune response, vaccine safety, and disease-specific targeting. Rising awareness regarding preventive animal healthcare, expansion of commercial livestock farming, and increasing pet ownership are further supporting market growth worldwide. In addition, growing investments in precision livestock farming, veterinary diagnostics, and disease surveillance systems are strengthening vaccination strategies across the animal healthcare industry.

Technology Scope and Products

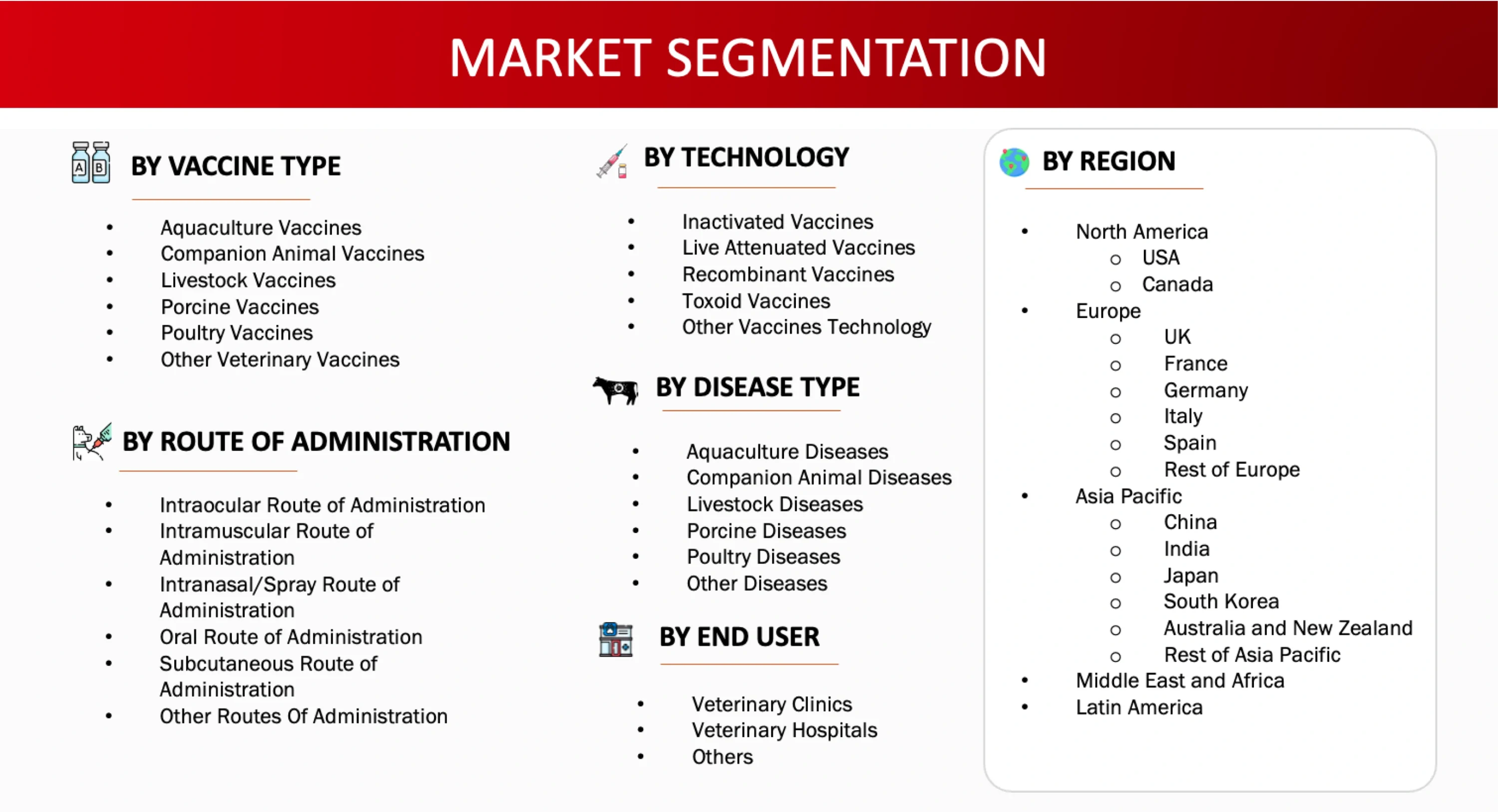

Veterinary Vaccines Detailed Market Segmentation

Want detailed insights from this report?

Industry Developments and Competitive Landscape

The market for veterinary vaccines is undergoing radical changes due to the innovations in the development of recombinant vaccines, vector-based delivery methods, and the use of better adjuvant systems. The increased attention paid to the prevention of diseases in animals, managing livestock diseases, and controlling zoonotic diseases is stimulating innovative approaches in vaccine development and delivery. Market players are widening their product lines through partnerships for research and development, increasing manufacturing capacities, and penetrating into new markets, especially emerging economies with rising numbers of livestock and companion animals. Also, the application of digital livestock monitoring systems and precision farming can aid in successful vaccination campaigns.

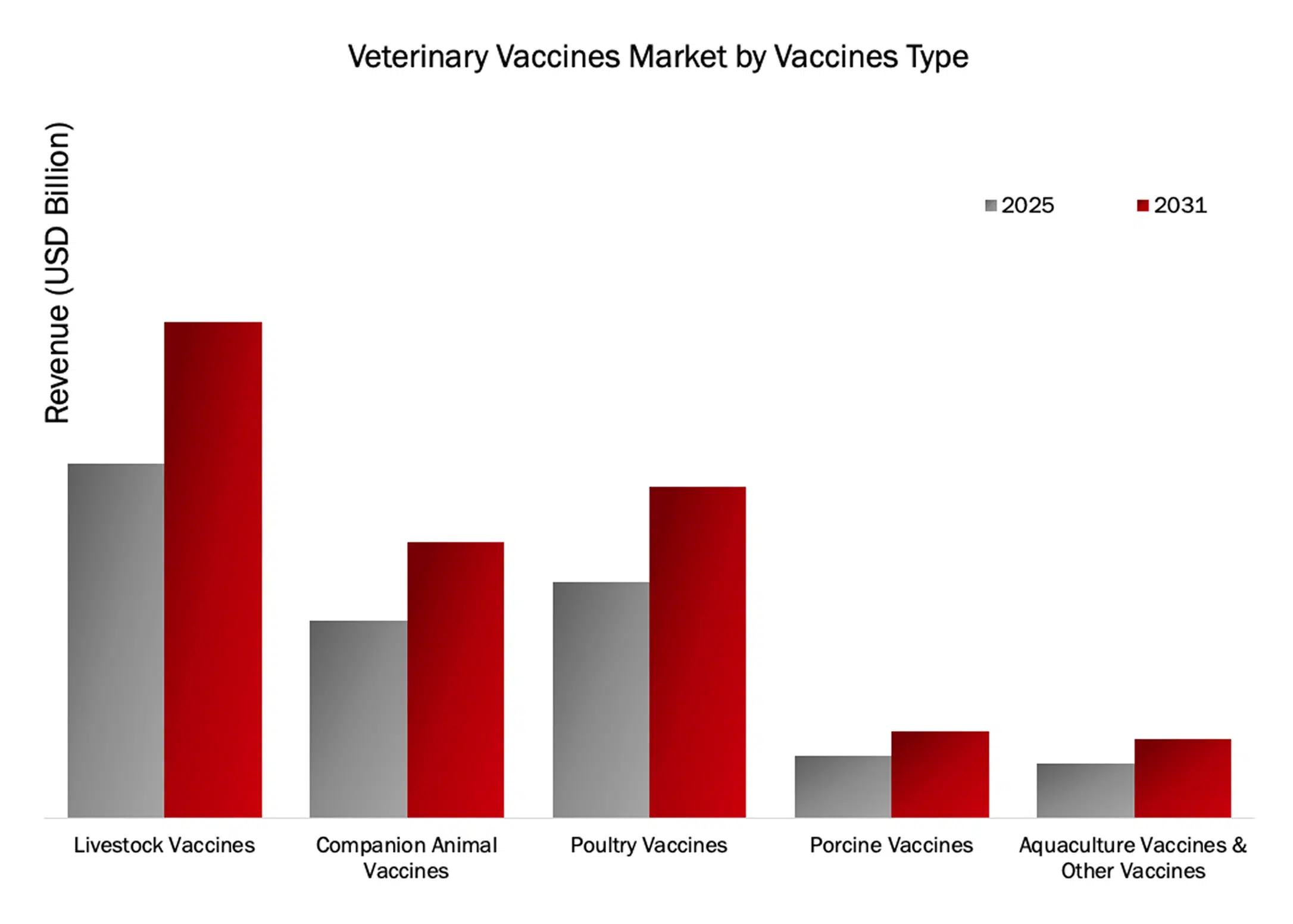

The livestock vaccines category emerged as the leader in the veterinary vaccines market in 2025 owing to the growing worldwide requirement for animal protein, the rising prevalence of transboundary livestock diseases, and the expanding number of animal immunization initiatives backed by governments.

-

According to statistics from the Food and Agriculture Organization (FAO), meat production in the world exceeded 360 million metric tonnes on an annual basis, leading to an increased demand for vaccinations that can prevent the occurrence of any diseases among cattle, poultry, swine, and aquaculture stocks.

-

The poultry industry is a key source of growth in the livestock vaccines segment. According to the FAO, the number of chickens, turkeys, guinea fowls, ducks, geese, and other poultry raised annually was more than 28 billion. Furthermore, there is a continuous effort by governments and international bodies like the World Organisation for Animal Health (WOAH) to conduct massive livestock vaccination drives to minimize zoonotic diseases and enhance food security. The rising investment in commercial farms, especially in the Asia Pacific and Latin American regions, is fueling the adoption of preventive vaccinations in livestock operations.

A large part of the worldwide veterinary vaccine market was attributed to the live attenuated vaccine segment by 2025 since they elicited a strong and long-lasting immune response, are relatively inexpensive and have become popular in both livestock and pet use.

-

Used for immuno-prophy-lactic purposes for preventing outbreaks of various types of infectious animal diseases, including Newcastle disease, infectious bronchitis, canine distemper virus, bovine viral diarrhoea and classical swine fever, these vaccines are preferred for participation in large-scale vaccination programs because they stimulate both antibody (humoral) and cell-mediated (cellular) immunity in animals with very few doses.

-

The poultry industry has been one of the main consumers of live attenuated veterinary vaccines, owing both to the tremendous number of chickens produced (over 28 billion live birds produced globally each year) and the potential for experiencing an outbreak of avian influenza. The livestock sector has also been a major market segment for live attenuated vaccines primarily due to their rapid induction of immunity in animals, and the ease with which they can be administered among extremely large numbers of livestock using sprayers, oral administration, or drinking-water delivery systems.

-

In 2025, North America was the leader in the veterinary vaccines market due to its advanced infrastructure for animal healthcare, a large volume of livestock produced, and high levels of companion animal ownership. The U.S. is among the top producers of beef, chicken, and dairy products with USDA statistics stating that there are more than 85 million cattle and over 9 billion broiler chickens produced per year. Demand for routine vaccination programs to prevent diseases like bovine respiratory disease, avian influenza, and swine infections will continue to be significant because of the size of the commercial livestock industry.

-

This region has many households with pets; according to the American Pet Products Association (APPA) about 66% of all households in America have pets. An increase in spending on preventative care for pets such as routine vaccinations for dogs and cats will help create demand for vaccines for this segment of the market. Regulatory oversight, large numbers of veterinary facilities across North America, and increasing technological advancements related to vaccine development such as the use of recombinant and vector based vaccines will all contribute to North America’s continued growth as a leader in the veterinary vaccines market.

What This Report Covers

This report provides a comprehensive analysis of the veterinary vaccines market, offering insights into key trends, growth drivers, challenges, and future opportunities. It is designed to support strategic decision-making through a combination of quantitative data and qualitative analysis.

Specifically, the report covers:

Market Overview & Definition: Overview of the market scope, structure, and key terminology.

Market Size & Forecast: Historical data and future projections across key segments and regions.

Key Market Trends: Insights into emerging trends, technological advancements, and evolving demand patterns.

Drivers, Restraints & Opportunities: Analysis of key factors influencing veterinary vaccines market growth.

Competitive Landscape: Overview of major players, their strategies, and recent developments.

Detailed Patent Analysis which includes, top assignees, geography focus of top assignees, legal status, technology evolution, key patents and patent trends and innovations

Segmentation Analysis: Breakdown by product, platform, sample, end users, mode of acquiring and region.

Regional Insights: Key regional trends and growth opportunities.

Future Outlook: Strategic insights and future market direction.

Research Methodology

The study of the veterinary vaccine market is based on a combination of primary and secondary research methodologies, supported by data validation and analytical modeling to ensure accuracy and reliability.

Market Definition: Veterinary Vaccine Market

The veterinary vaccine market consists of the development of vaccines to help prevent infectious diseases in livestock, pet animals and also include poultry and aquaculture animals. The role of the veterinary vaccines market is to stimulate animal immune systems so they become resistant to bacteria, viruses and parasites, thus resulting in potentially less transmission of disease from animals to people.

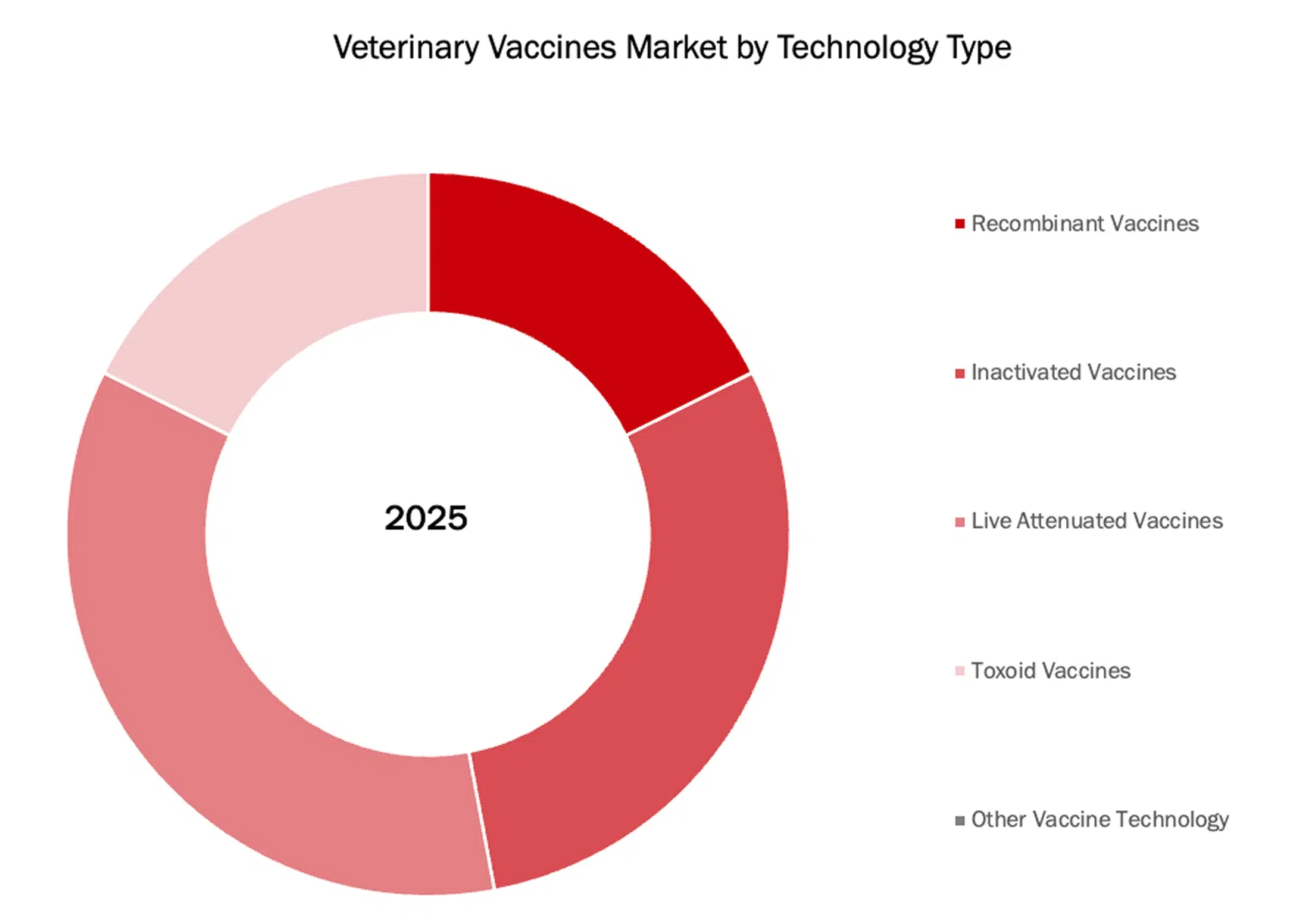

There are many different veterinary vaccine technologies available, such as live attenuated, inactivated, recombinant, vector-based, DNA and multivalent formulations. Vaccines can be given to animals in many ways, including by injection (annual vaccinations), orally (dissolving tablets or capsules), by intranasal spray (nasal rabies vaccine) and also as a food additive (poultry) with delivery occurring at commercial farms and veterinary clinics or hospitals.

Veterinary vaccines are commonly used for the control of diseases such as foot-and-mouth disease, avian influenza (Bird Flu), Newcastle disease, rabies, Bovine Respiratory Disease and Swine Fever. The veterinary vaccines market has an important impact on the prevention of disease outbreaks due to the economic loss they inflict, the decreased need for antibiotics used to treat sick animals, the improvement of herd management practices and the support of the worldwide control of zoonotic disease.

Key Stakeholders

The veterinary vaccine market involves a diverse ecosystem of stakeholders:

- Veterinary Vaccine Manufacturers

- Animal Health Pharmaceutical Companies

- Livestock Producers and Commercial Farms

- Poultry Integrators and Hatcheries

- Companion Animal Clinics and Veterinary Hospitals

- Aquaculture and Fish Farming Companies

- Contract Research Organizations (CROs) and Clinical Testing Laboratories

- Veterinary Research Institutes and Academic Organizations

- Vaccine Adjuvant, Antigen, and Biologics Suppliers

- Cold Chain, Packaging, and Logistics Providers

- Veterinary Distributors and Animal Health Retail Networks

- Government Veterinary and Animal Health Departments

- Regulatory Authorities (e.g., USDA Center for Veterinary Biologics, European Medicines Agency)

- International Animal Health Organizations (e.g., WOAH, FAO)

- Pet Care and Animal Welfare Organizations

- Biotechnology and Recombinant Vaccine Technology Providers

- Feedlot Operators and Dairy Producers

- Investors and Strategic Industry Partners

Key objectives of the Study

- To define, describe, analyze, segment, and forecast the veterinary vaccines market by vaccine type, by route of administration, by technology, by disease type and by end users.

- To describe and forecast the market for four key regions: North America, Europe, Asia Pacific, and Rest of the World.

- To provide detailed information regarding key drivers, restraints, opportunities, and challenges influencing market growth

- To strategically analyze the micro indicators with respect to individual growth trends, prospects, and contributions to the overall market size

- To analyze opportunities for stakeholders in the veterinary vaccines industry and emphasize on competitive landscape of the market.

- To develop competitive benchmarking of the key market players based on technology specifications and end users.

- To strategically profile key players and comprehensively analyze their product portfolio offerings, and core competencies

- To analyze competitive developments, such as launches and approvals, agreements, mergers and acquisitions, partnerships, joint ventures, investments and expansions, and collaborations, veterinary vaccines domain.

Need deeper insights on this market?

Get full report access with detailed forecasts, competitive analysis, and segmentation.

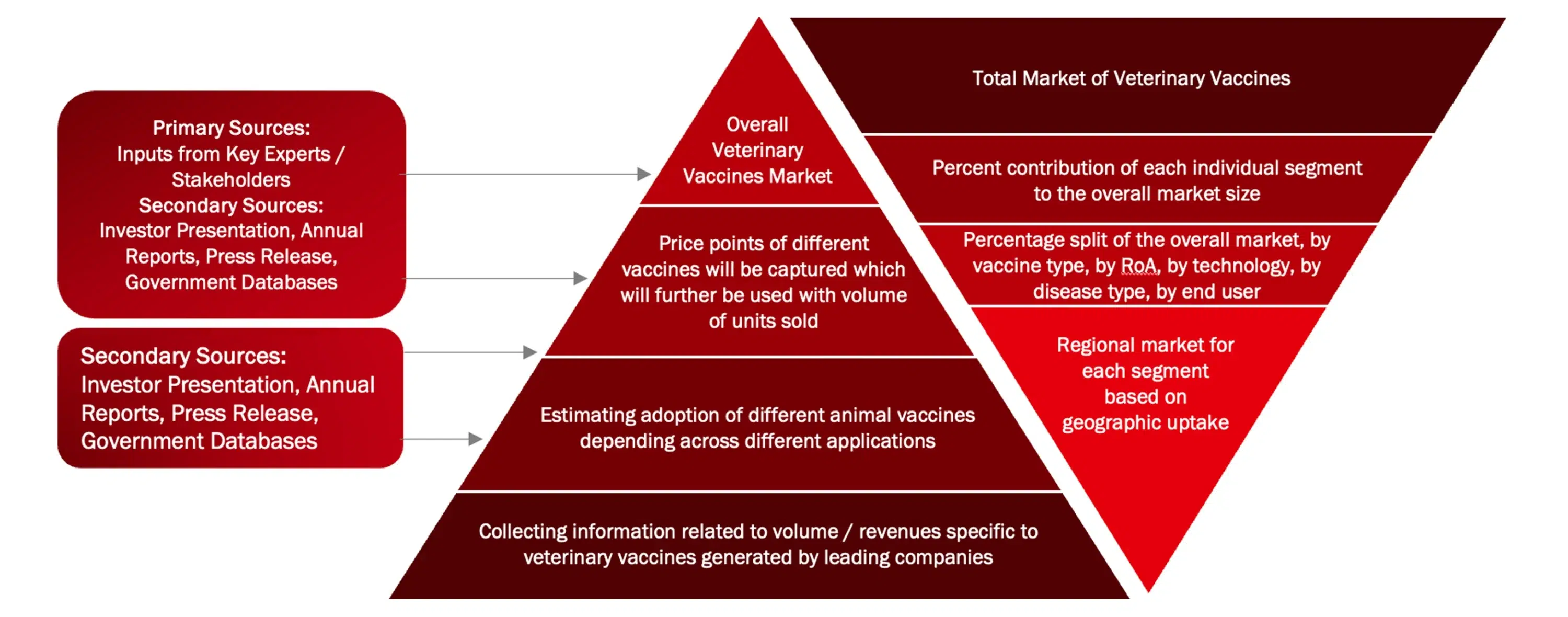

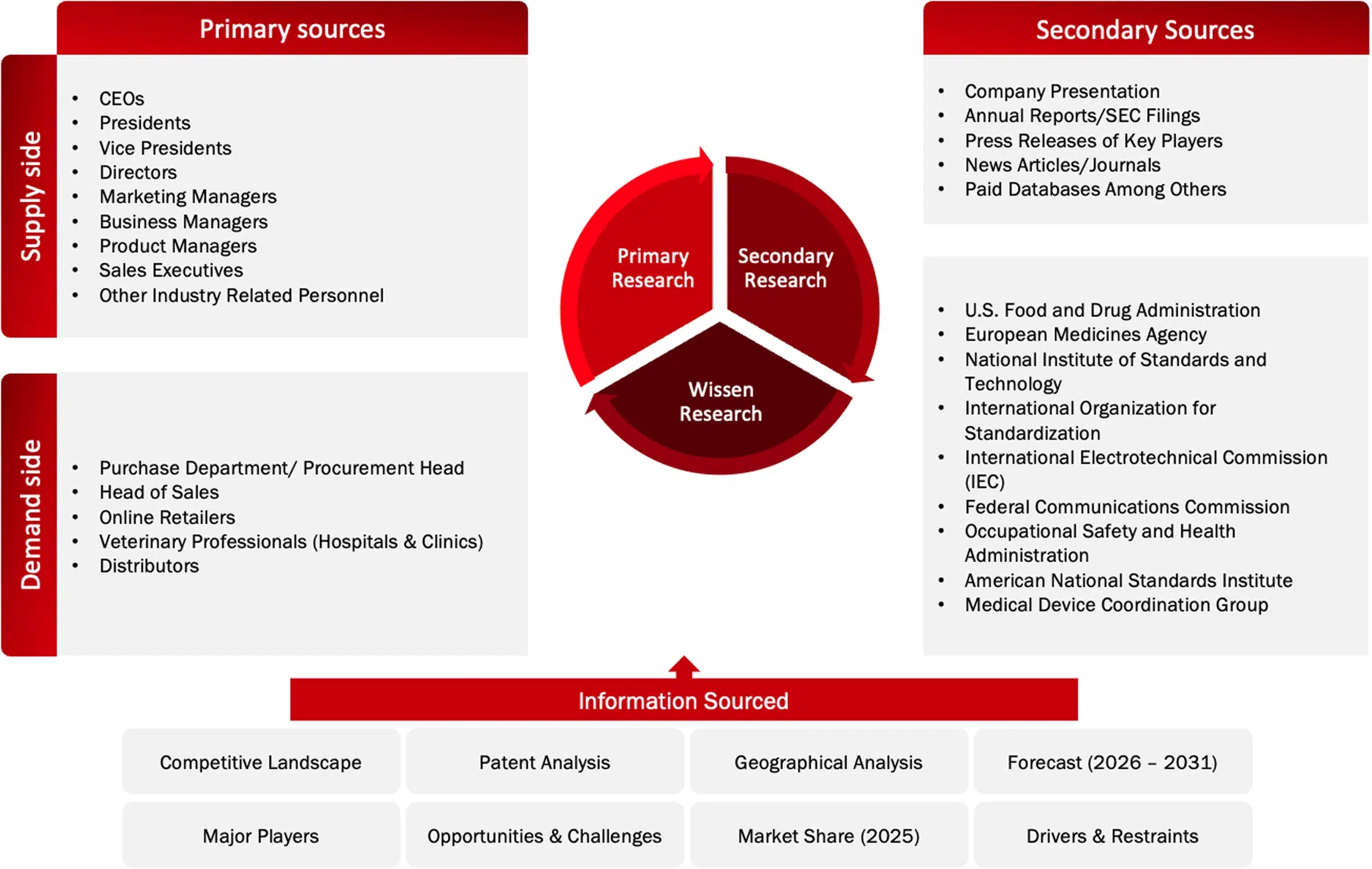

1. Research Approach

This research employs a systematic approach by using primary research along with secondary research to achieve full coverage and accuracy of information about the veterinary vaccines sector. Through this approach, the current market trends in terms of consumer behavior, technological developments, and competitive environment can be analyzed thoroughly.

Secondary Research

Secondary research involves the collection of data from reliable sources such as industry databases, company annual reports, investor presentations, and regulatory filings. This process helps in understanding market trends, identifying key players, and gathering technical and commercial insights.

A comprehensive database of leading companies and market participants is developed through secondary research to support further analysis.

Primary Research

Primary research is conducted to validate findings from secondary research and to gain deeper insights into market dynamics. Interviews are carried out with industry stakeholders across both demand and supply sides, including executives such as CXOs, Vice Presidents, and Directors from business development, marketing, and product teams.

Data is collected through structured questionnaires, email interactions, and telephonic interviews across key regions including North America, Europe, Asia Pacific, and Rest of the World.

Market Size Estimation

Market size estimation is performed using both top-down and bottom-up approaches. Key market players are identified, and their revenues are analyzed to estimate the overall market size.

The market is further segmented based on:

- Product and service mapping across regions

- Adoption patterns across key application segments

- Insights gathered through primary and secondary research

Data Validation and Research Design

After estimating the overall market size, the data is validated using triangulation methods and market breakdown techniques to ensure accuracy and consistency. Both demand-side and supply-side factors are considered to refine the analysis.

The final data is validated through multiple sources to ensure reliability and to provide accurate insights across all market segments and regions.

2. Assumptions of the Study

The analysis of the veterinary vaccines market is based on the following key assumptions:

- Trends in the industry are drawn from historical data and current information within the sector

- The future outlook is underpinned by constant economic conditions in the absence of shocks to the market

- The rate of adoption for veterinary vaccines will rise steadily in all important regions

- Advancements in next-generation vaccine technologies such as recombinant vaccines, mRNA vaccines, and intranasal vaccines will continue to drive growth in the veterinary vaccines market.

- The income statement and market share figures are estimated using available information from the industry and publicly available data

- The exchange rate and price trends will not be greatly affected during the forecast period

Scope and Limitations

Scope of the Study

This report offers an exhaustive overview of the international veterinary vaccines market and includes the following components:

- Summary of market size, growth trends, and projections

- Carefully segmented market based on vaccines type, technology, disease type, end users, by route of administration and geography

- Discussion of primary factors influencing the market

- Competitor analysis

- Insights into regional and national market performance

Limitations of the Study

Despite the best efforts being made to keep the results accurate, the study does suffer from some limitations:

- It has been done using both primary and secondary data that come with their own constraints

- Rapid developments in technology might affect the future course of market dynamics

- Some figures are only approximations due to lack of public disclosure

- The report is not an insurance against any disruptions in macroeconomics and geopolitics

- Future forecasts are indicative and subject to change due to altered industry dynamics

3. Data Triangulation and Market Breakdown

Data triangulation involved the combination of primary research, secondary research, and the Wissen Research analysis. Once the data points were sourced from the secondary market research, we sanitized the data points to make the market sizing and growth forecast more accurate by developing our own assumptions based on the inputs and insights we gather through the primary interviews with the industry experts. Once the data was thoroughly validated through primary interviews from both, demand and supply side of the market, our team of analyst and other team members involved finalized the market sizing and growth forecast.

Data Triangulation Methodology

Sources: U.S. Food and Drug Administration, European Medicines Agency, National Institute of Standards and Technology, International Organization for Standardization, International Electrotechnical Commission, Federal Communications Commission, Occupational Safety and Health Administration, American National Standards Institute, Device Coordination Group, Company Website, Press Releases, Annual Reports, Paid Data Sources, and Wissen Research Analysis.

Years Framework

5. Bottom up approach (Demand Side) and Top down approach (Supply Side)

Bottom-Up Approach (Demand Side Approach):

Determining the market size through the consolidation of demand among end-users, sectors, and geographic areas, which are calculated according to real-world demand conditions.

Top Down Approach (Supply Side Approach):

Calculating the market size through revenue and performance of the industry and its important companies, allocating the market size among various sectors.