Artificial Intelligence (AI) In Healthcare Market

Global Industry analysis, Size, Share, Growth, Trends, and Forecast 2026-2031

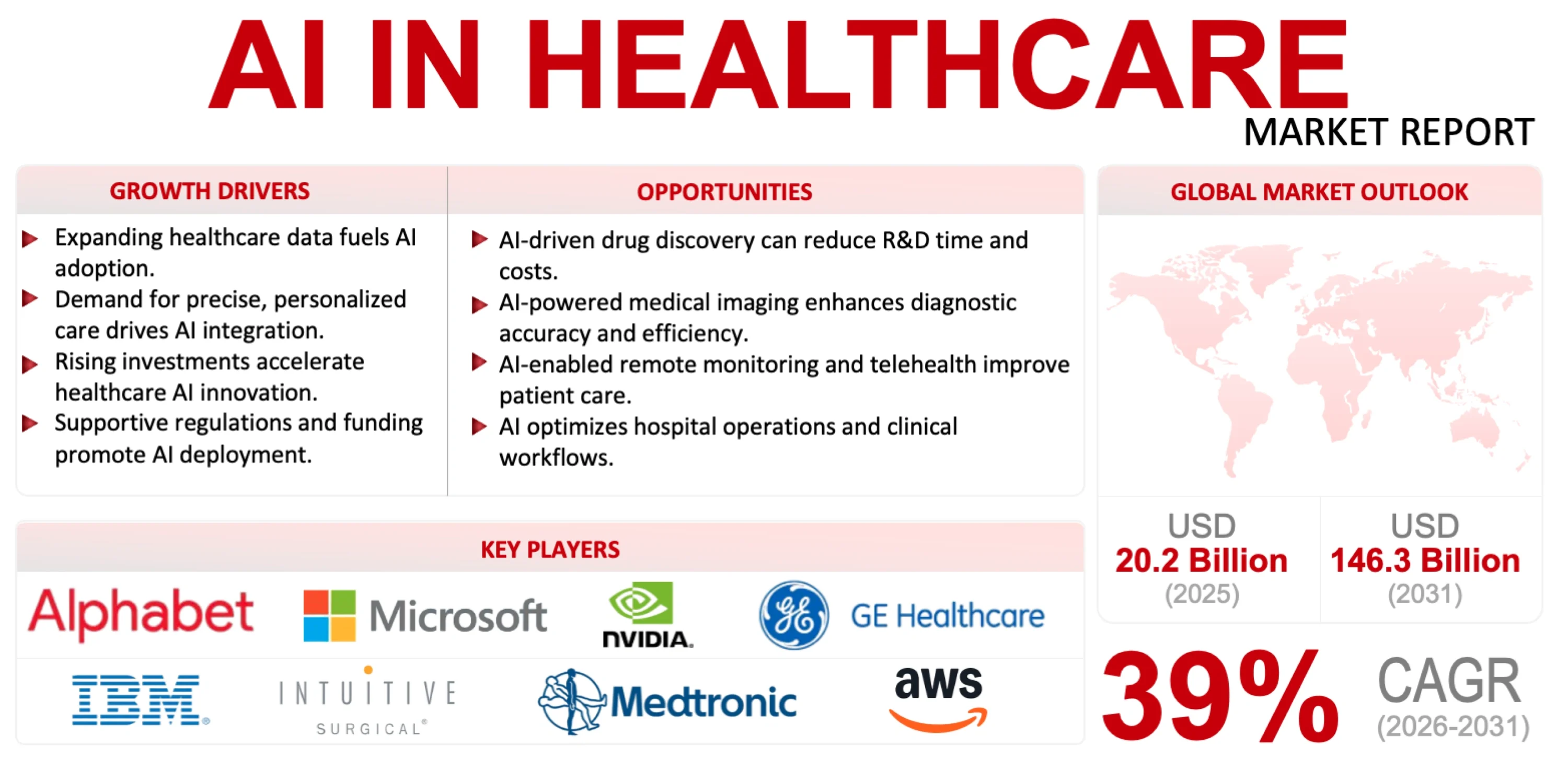

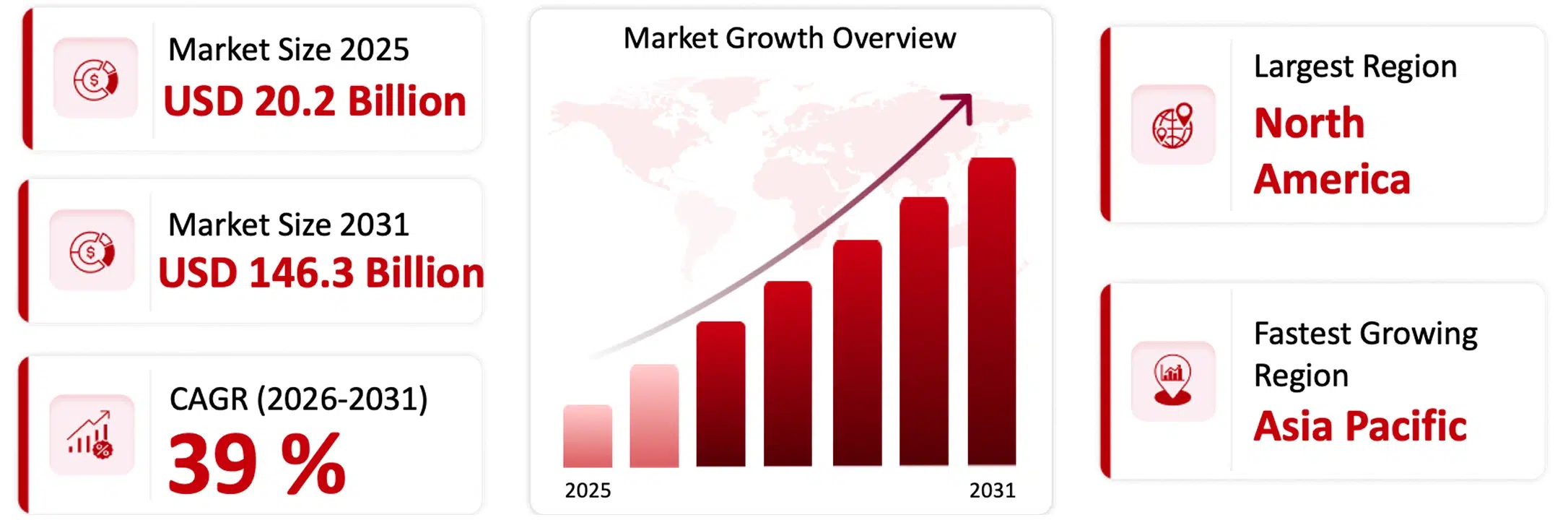

The global AI in Healthcare market is projected to reach USD 146.3 billion by 2031, growing at a CAGR of 39% during the forecast period.

| Market Size 2026 | Market Size 2031 | CAGR (2026-2031) | Largest Region | Fastest Growing Region |

|---|---|---|---|---|

| USD 28.2 Billion | USD 146.3 Billion | 39% | North America | Asia Pacific |

Market Overview

The global AI in Healthcare market‘s growth is occurring largely because hospitals are under major operational pressure due to increased patient volumes, physician burnout, limited staffing, and rising administrative costs; and less due to the hype surrounding AI technologies for use in healthcare. AI technologies have begun to be routinely applied to things like medical imaging, clinical documentation, predictive analysis, hospital workflows and drug discovery. Adoption has increased as electronic health records and cloud-based infrastructure within the healthcare industry are becoming more prevalent. The value of the market in 2026 USD 28.2 billion and projected to be USD 146.3 billion by 2031 with a compound annual growth rate (CAGR) of 39 % from 2026 through to 2031.

Technology Overview

AI is used in health care through the analysis of data from thousands of medical records, lab tests performed on patients, and records of previous patient outcomes. Using machine learning techniques, computers can find patterns within the data and help to predict patients’ diagnoses and risk factors based on their individual information. Deep learning technologies, primarily through neural networks, analyze and process images such as X-rays, CT scans, and MRIs with greater accuracy than any human physician. Also, natural language processing (NLP) converts clinical notes made by the physician during patient visits and other documentation into computer-readable format, enabling easier access and searching through medical documents that would otherwise only be available in paper form. Increasingly, generative AI is being used for documentation to create notes when a patient is seen by a doctor or other provider, for communicating with patients or caregivers about treatment options, and for assisting with the generation of research.

Key Growth Drivers

- The increasing use of AI-based scribe services and workflow automation is greatly reducing the burdens of clinician documentation processes.

- The integration of AI technologies into current EHR systems is speeding up operational integration of AI throughout health systems.

- AI-supportive imaging is improving scan prioritization, report generation speed, and efficiency of the diagnostic work processes.

- AI-based tools being utilized by hospitals is resulting in lowered operational expenses and improved measurable financial results.

- Pharmaceutical companies are utilizing AI technologies to decrease timeframes for clinical trial processes and to speed up drug development.

- Generative AI is improving communications between patients’/healthcare providers as well as summarizing medical records and making clinical data easier to access

AI in Healthcare Market Key Highlights

Need deeper insights on this market?

Get full report access with detailed forecasts, competitive analysis, and segmentation.

AI in Healthcare Market Trends

From experimental pilot projects, AI in healthcare is moving toward integration and deployment based more on workflows and operations. The most significant trend is the rapid use of generative AI for clinical documentation, automation of administrative tasks, and patient interaction, rather than autonomous diagnosis. More hospitals are using ambient AI systems to convert doctor-patient conversations into structured medical records. Another important trend is multimodal AI systems that integrate different modalities for analysis such as medical imaging, clinical notes, lab results and/or patient histories. Healthcare providers are also integrating certain AI solutions into the platforms used for their electronic health records to improve usability and scalability. As adoption moves from pilot platforms into everyday hospital operations, healthcare organizations have defined and embraced “AI Governance, Explain-ability, Cybersecurity and Measurably Successful Return on Investment” to define governance processes for growing as AI adoption expands.

Ambient Clinical Intelligence and AI Documentation Automation

Ambient clinical intelligence systems, which leverage AI technologies for automated clinical documentation of doctor-patient encounters, represent one of the hottest trends in healthcare artificial intelligence (AI). AI tools used in ambient clinical intelligence scrutinize real-time interactions between physicians and patients, producing many of the traditional forms of clinical documentation used in modern medicine (i.e. clinical notes, discharge summaries, billing documentation, and EHR updates). Ambient clinical intelligence systems are gaining traction in part due to increased understanding by healthcare organizations that administrative overload is one of the most significant barriers to operational efficiency in contemporary medicine. Rather than having doctors spend hours creating notes, providers are turning to AI systems to automate repetitive recording tasks, allowing clinicians to maximize their time spent interacting with patients.

Recent published statistics regarding the deployment of healthcare AI highlight that ambient speech and documentation technologies represent the most extensively deployed types of healthcare AI and provide immediate, measurable productivity improvements. Some healthcare systems report thousands of hours of clinician documentation time saved via AI-enabled documentation workflows. The solution is rapidly moving from standalone ambient clinical intelligence-scribes to fully integrated workflow automation platforms that can be utilized across a continuum of care, providing support for coding, referral management, scheduling, and claims management. However, despite the rapid evolution of these technologies, hospitals remain concerned about the need for adequate human oversight and compliance training as well as establishing secure electronic health records (EHR) interfaces prior to experiencing widespread, long-term success with this innovative approach to documenting clinical encounters.

Growth of Multimodal and Agentic AI Systems

Another big trend is the shift from single-function to multi-function AI models that are agent-based. Previous AI-based healthcare solutions typically only examined one source of factual information – either images or structured patient data. The newer multi-function CI-based intelligence examines all relevant sources of medical information based on concepts within a clinical context of the entire patient record. This resulted in more relevant decision-making across complex healthcare delivery systems through AI systems that are contextually aware and being used to improve clinical decision-making accuracy.

While organizations are also pursuing multi-function and agent-based AI systems capable of coordinating complex, multi-step operational processes, as opposed to purely generating language and predictions, many healthcare organizations are interested in using agent-based AI systems to connect, schedule, image, bill for, and create laboratory and EMR records to automate logistical orchestration of work across departments. Based on industry surveys, the predominant view of many in leadership positions in health programs is that the next phase of AI deployment will be to achieve integrative and scalable operations. Analysts agree that the available literature indicates that multi-function AI models have consistently produced stronger outcomes than single-source data models in many clinical applications; however, there remain significant impediments to widespread adoption, such as standardization of data, integration/interoperability with other systems, understanding how AI works and establishing regulatory validation.

Key Players in the AI in Healthcare Market

Leading companies in the AI in healthcare market are focusing on innovation, strategic partnerships, and expansion of health-centric features to strengthen their market position.

Strategic Activities Within the AI in Healthcare Market

IBM (US) and Fujitsu (Japan) announced a partnership to create an independent medical cloud solution to deploy AI throughout hospitals. The two companies collaborated to digitize health information, automate documentation and coding, and improve clinical support and medical research across Japan.

Amazon Web Services (U.S) launched Amazon Connect Health, which provides an agentic AI solution for appointment scheduling, ambient documentation, medical coding, and patient insights. The new platform helps decrease administrative burden, speed up revenue cycles, and connect directly to EHR systems in order to help improve clinician and patient experiences.

Microsoft Corporation (U.S.) launched Copilot Health as a consumer healthcare AI solution that merged electronic health records (EHRs), wearable device information, and lab-routine test results. This tool utilizes advanced logic for providing individualized healthcare data, promoting timely treatments, and simplifying the process of obtaining reliable medical data.

Oracle Corporation (US) enhanced its Oracle Health Clinical AI Agent to automatically create clinical orders through ambient listening and AI inference. Physicians’ administrative workload was minimized, record accuracy was upgraded, and documentation time was saved for approximately 200,000 documentation hours for physicians.

AI in Healthcare Market Insights

The AI in healthcare market is growing rapidly with hospitals moving away from pilot-trying out AI and toward deploying AI at the user level on a large scale. Growth is now translated into money to support actual hospital needs such as implementation of and assisting (or automating) workflow processes, medical documentation, imaging analysis, revenue cycle optimization and other needs, not just research using AI. Ai survey results show hospitals Favor AI projects that have measurable impact on hospital operations and quick returns on investments. Additionally, generative AI is growing health care as an industry because it improves usability when implementing AI at the user level for clinicians and administrators. In addition, hospitals are making larger investments because they have moved to the position of recognizing AI as an infrastructure technology and would be integrating AI into all of their EHR systems, cloud environments and overall operations.

AI is now being used by many health care service providers as an automated way of organising their operations to help with efficiency and assisting their practitioners when making decisions. The most popular ways to apply AI technology in healthcare are medical imaging analysis, clinical documentation, predictive analytics, patient triage, revenue cycle management and drug discovery. Healthcare providers use ambient listening devices to create clinical notes for patients instantaneously, while a patient is being treated, and predictive AI technology can assist healthcare providers to identify patient risks, optimise the use of staff and improve the efficiency of their workflow. Additionally, AI technology will allow pharmaceutical researchers to have an accelerated process for molecular analysis and clinical trial design. Overall, AI technology will give healthcare providers the ability to use a single integrated clinical support system that combines imaging, laboratory data, physician notes, and patient history into one integrated clinical support system.

Growth in the AI industry has created many opportunities in healthcare. Hospitals are looking for scalable automation solutions to help with their workflow, such as scheduling and documentation, coding and billing, and managing patient flow. AI will help to automate these processes.

With the introduction of AI comes an increase in personalized medicine through the use of genomic (or DNA) analysis, imaging and clinical data, allowing for better targeted therapy. Remote monitoring of patients and virtual wellness platforms are becoming more widespread with predictive analytics and ways to engage with patients.

Pharmaceutical companies are also creating many new opportunities in areas like AI driven drug discovery (finding new medicines) and optimizing clinical trials. Emerging global markets are also helping to drive long-term growth in the industry with hospitals updating their IT systems to use modern technologies (the cloud).

A Few primary challenges exist in AI health care market that can hamper AI from being widely used. Health systems have a lot of patient data that is highly sensitive; therefore, there are major concerns about how safe the patients’ private data is and how likely cyber-attackers or hackers will be able to get into the hospital’s network to reach their private data. Hospitals’ IT systems do not easily integrate with each other; therefore, even if a hospital wants to use artificial intelligence (AI) for its operations, it cannot do so until it brings all of its IT systems together so that there is only one provider network. There are additional challenges to installing artificial intelligence (AI) into the health care industry due to regulatory uncertainty. For instance, it is necessary to have clinical validation of AI-based medical devices before AIs can obtain regulatory approval. There are additional challenges to using AI in healthcare, such as the lack of qualified individuals with knowledge of artificial intelligence, the difficulties associated with training clinicians to use AI systems, and the current legal and ethical issues (e.g., bias, transparency, and reliability) that exist concerning AI systems.

The AI healthcare market in Asia Pacific is growing at the fastest rate in global markets due to ongoing digitization of the healthcare system; and continued growth of hospital infrastructure, and continued government support for AI innovations. Countries such as China, India, Japan, South Korea, and Singapore are utilizing AI for various purposes including: diagnoses, hospital management systems and medical education. China has quickly expanded AI utilization in its broad array of tertiary hospitals, particularly in imaging, pathology and clinical decision-making systems. India is beginning to adopt more and more AI through a combination of innovative hospital labs, digital health initiatives and AI-focused medical education programs. The continued growth in this area is being sustained through continuing growth of cloud-based applications and improved technology infrastructure within the healthcare sector, and the ongoing necessity to improve access to quality healthcare within large and varied communities.

AI in Healthcare Market Dynamics

Drivers: Administrative Workflow Automation

Since many hospitals have experienced significant operational inefficiencies, administrative workflow automation has become one of the immediate growth drivers of AI in healthcare. According to research published in the Annals of Internal Medicine, doctors may spend nearly half of their workday interacting with electronic health records and administrative systems instead of with patients. AI-powered ambient documentation tools are helping to alleviate this burden by generating clinical notes and visit summaries automatically when patients are seen for visits. For example, many hospitals in the U.S. have reported that their time spent on documentation has decreased by 20–40% using AI-assisted medical scribes, resulting in increased physician productivity, decreased risk of burnout, and increased patient throughput. As global Labour costs rise, hospitals are using AI automation as an operational requirement instead of waiting to invest in this technology in the future.

Challenges: Data Privacy, Bias, and Clinical Validation

The greatest obstacle facing artificial intelligence (AI) in health care is to be able to provide safe, reliable and clinically validated implementation across diverse patient populations. Healthcare systems have large amounts of sensitive patient data and are under increasing pressure to address cybersecurity issues. Recent reports indicate that the healthcare sector continues to be one of the most frequently attacked by ransomware due to the high value of the medical data in the black market. Furthermore, the results produced by AI models can vary widely depending on whether training data consisted of complete datasets, as well as being specific to certain regions. Example studies have found that some diagnostic AI tools perform differently based on the patients’ ethnicity, imaging equipment used, and the infrastructure available in the hospital. Such variability poses regulatory and legal challenges for hospitals that want to implement AI solutions at scale. Therefore, there is a growing demand for healthcare providers to find AI systems that have explainable use-cases, obtain external validation studies, and to have a well-defined oversight program in place prior to implementing AI solutions on a large scale.

Opportunity: AI-Powered Personalized Medicine and Oncology

One of the greatest long-term potentials for AI in health care, particularly in oncology and genomics, is through personalizing medicine. Hospitals today generate huge amounts of genomic, pathology, imaging, and clinical data that can’t be managed manually. Through the use of AI models, medical professionals can find disease patterns quickly and accurately by triangulating this multi-modal data. For example, AI-assisted genomic analysis allows for fast identification of clinically relevant mutations, going from a work effort that can take days to complete down to mere hours—specifically in some of the workflows related to cancer. Pharmaceutical companies are also leveraging AI to increase the likelihood of identifying potential biomarkers for use in clinical trials and helping recruit appropriate patient populations more quickly by matching individual patient characteristics to the specific trial requirements. As precision oncology becomes more global and sequencing costs decline, it is anticipated that AI-based personalized treatment will be at the center of future cancer treatment and development of targeted therapies.

Technology and Market Insights

AI healthcare market matures from being primarily experimental to now having operationally integrated platforms that can effectively measure improved operational efficiency; hospitals are beginning to use more generative AI, multimodal AI and ambient clinical intelligence (ACI) systems which integrate multiple modalities including medical images, physician notes, laboratory results, and electronic health records (EHRs) into one cohesive workflow through the use of common workflows. The rapid growth of AI based documentation tools are being driven by their ability to significantly decrease the amount of time and effort expended by clinicians on administrative tasks therefore increasing their ability to see more patients in a day through improved efficiency (throughput). From a marketing standpoint, healthcare delivery organizations are now focused on those AI solutions that provide a clear operational ROI versus those that provide an experimental or innovative approach. Continued focus on areas such as administrative automation, imaging workflow optimisation, predictive analytics and AI enabled drug discovery will continue to be priority investment areas going forward. As a complement to the four areas above, the demand for more useable/explainable AI, improved cyber security, enhanced interoperability and new regulatory requirements will become increasingly important to enable broader deployment and commercialization of healthcare AI solutions.

Technology Scope and Products

AI in Healthcare Detailed Market Segmentation

Want detailed insights from this report?

Industry Developments and Competitive Landscape

Technologies such as Generative AI, Ambient Clinical Intelligence, Predictive Analytics, and Multimodal AI Platforms are providing innovation opportunities to develop AI applications for the Healthcare Industry rapidly. AI Solutions, including Document Management, Image Analysis Systems, and Workflow Automation, will allow hospitals to streamline their operations while simultaneously reducing their clinician’s workload. There is increasing competition within Health IT vendors and Cloud Providers, as well as between traditional Tech companies and AI Startups, to provide scalable, explainable, interoperable, and regulatory-compliant AI Solutions for clinical and administrative applications in the Healthcare Industry.

Software Solutions made up the majority of the AI in health market because of the fast implementation of generative AI applications, the popularity of specific regulatory environments, and shorter purchasing times, Hospitals and governments chose a software model by using scalable cloud-based software to submit ambient documentation & clinical support decisions and to automate coding processes (continuous updates and easier to implement than a hardware or service model).

-

A national study released at the end of 2025 indicated that 50% of hospitals in the U.S. were using or planning to use the generative AI software application solutions

-

85% of the money spent on healthcare generative AI was to support software startups to automate workflow and documentation/coding processes

-

The ONC HTI-1 Final Rule of 2025 required EHR certification vendors to upgrade their predictive AI modules for all software, which provided a reason for all companies to resell/license their software products

-

The FDA created the Predetermined Change Control Plan to allow companies to make faster changes to their algorithms, improving their competitiveness and overall advantage in being a Software as a Medical Device business

-

Healthcare IT purchasing cycles decreased from a typical purchase cycle of 8.0 months in 2025 to 6.6 months, which significantly increased the acceptance rate of healthcare providers of cloud-based AI software solutions.

Cloud-based deployment dominated the AI in healthcare market by the year 2025 because of the advantages it provided including scalability, fast implementation time, and ability to handle compute-intensive generative artificial intelligence workloads. As a result, Hospitals and Government Agencies preferred using cloud platforms to support ambient, clinical analytic, and regulatory compliance documentation processes because they offer secure compute capabilities, continuous updates, and lower infrastructure needs compared with traditional on-premise systems.

-

AI models that were advanced required access to high-performance GPU infrastructures which hospitals typically accessed from their Cloud Providers rather than investing funds in expensive local hardware systems.

-

A Study from the JAMA Network revealed that by 2025, Approximately 50% of Acute Care Hospitals across the U.S were prepared either to adopt or plan to adopt generative Artificial Intelligence Tools

-

The OneHHS AI Strategy caused an increase in adoption of Cloud by Agencies such as CMS and CDC that would allow them to efficiently digitally Process Healthcare Databases in volumes

-

The ONC’s HTI-1 Final Rule caused an increase in demand for Cloud-based Monitoring, Transparency, and Continuous updates of Predictive AI Models

-

The length of Time it took for Healthcare Information Technology to Purchase Products dropped from 8.0 Months to 6.6 Months with much of the preference being given towards Software as a Service (SaaS) Platforms that could be setup within days

North America had the largest portion of the market for AI in healthcare because of substantial venture capital investment, quick regulatory approvals, helpful federal policies, and the high cost of healthcare administration. The widespread implementation of ambient documentation, coding automation, and clinical AI solutions are some of the benefits enjoyed by the North American Region. Government and healthcare organizations are fast-tracking the implementation of these solutions within both their operations and care delivery workflows.

-

US Healthcare organizations invested nearly $1.4 billion into AI in 2025, with approximately 75% of total investments being provided by providers and payers based in North America

-

Approximately 85% of the Healthcare AI investments went to AI-natives, allowing for the development of North America’s innovation ecosystem and commercialization capability

-

During 2025, the FDA in the US approved 295 AI/ML-enabled medical devices, enabling faster adoption of software-enabled clinical and diagnostic tools. There was strong interest in reducing the administrative burden and clinician burnout through investments of over $1 billion into ambient documentation and coding automation solutions.

-

In 2025, the US Department of Health and Human Services introduced its OneHHS AI strategy to create acceleration of the use of AI solutions within federal healthcare agencies.

What This Report Covers

This report provides a comprehensive analysis of the AI in healthcare market, offering insights into key trends, growth drivers, challenges, and future opportunities. It is designed to support strategic decision-making through a combination of quantitative data and qualitative analysis.

Specifically, the report covers:

Market Overview & Definition: Overview of the market scope, structure, and key terminology.

Market Size & Forecast: Historical data and future projections across key segments and regions.

Key Market Trends: Insights into emerging trends, technological advancements, and evolving demand patterns.

Drivers, Restraints & Opportunities: Analysis of key factors influencing AI in healthcare market growth.

Competitive Landscape: Overview of major players, their strategies, and recent developments.

Detailed Patent Analysis which includes, top assignees, geography focus of top assignees, legal status, technology evolution, key patents and patent trends and innovations

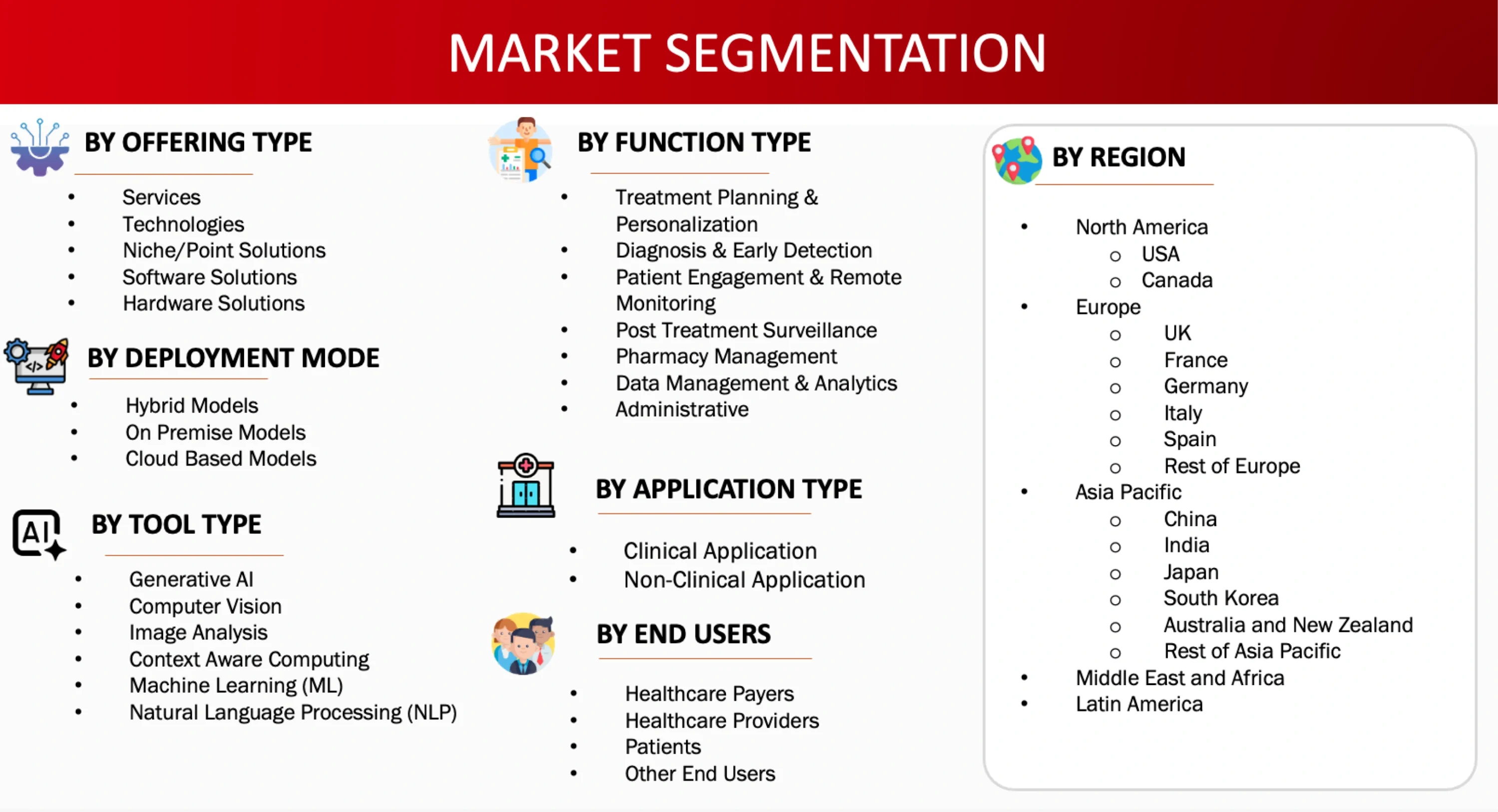

Segmentation Analysis: Breakdown by offering type, deployment type, function type, application, tool type, end user type and region.

Regional Insights: Key regional trends and growth opportunities.

Future Outlook: Strategic insights and future market direction.

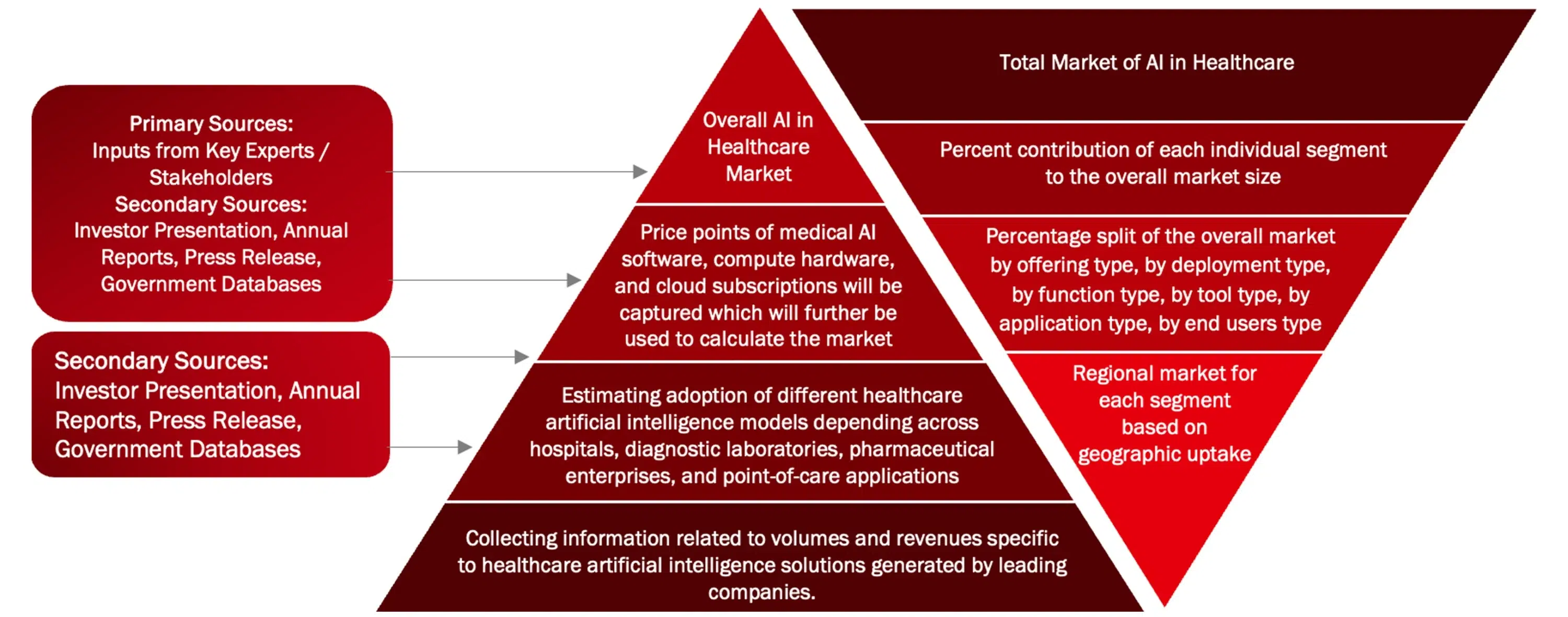

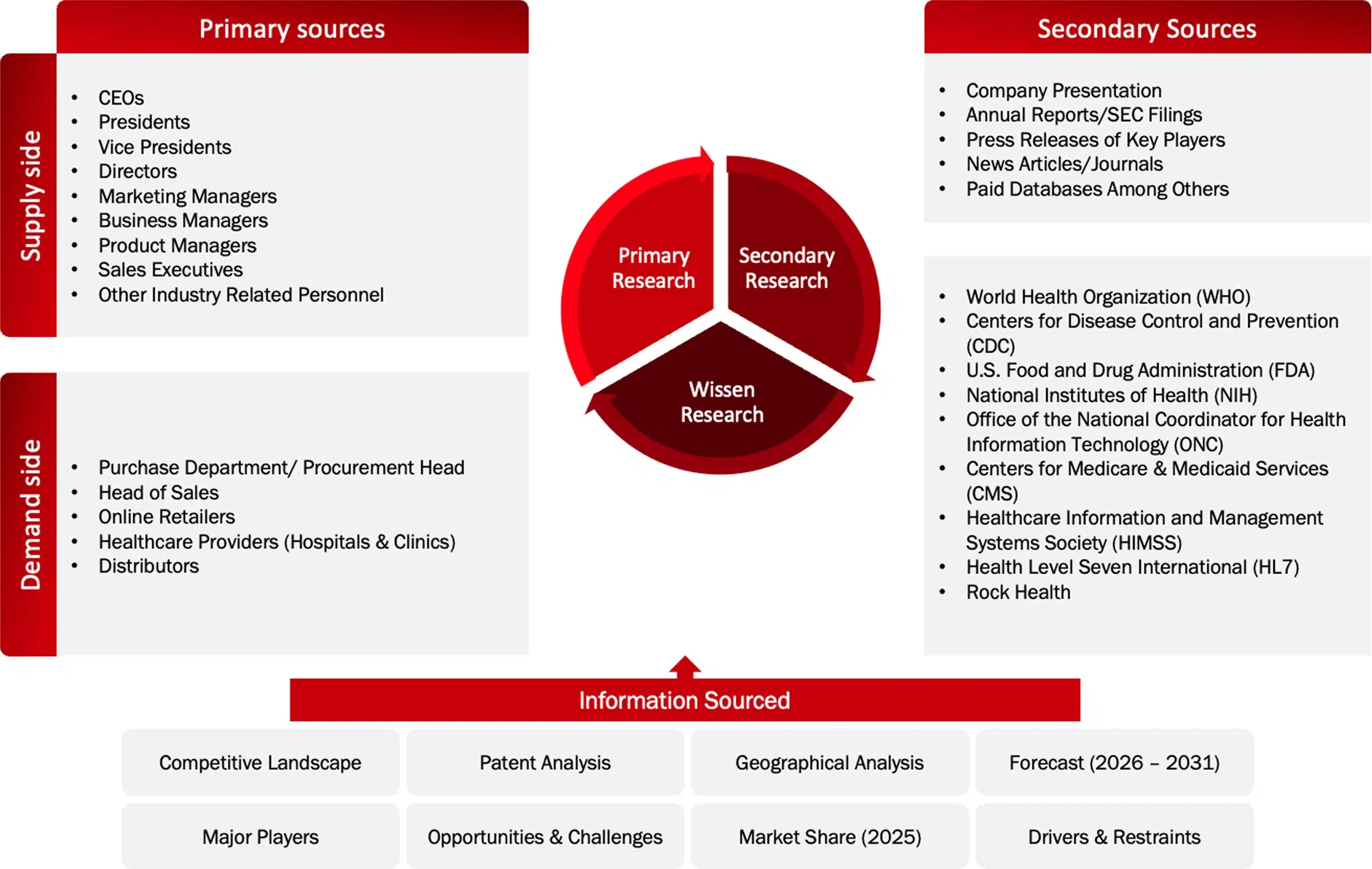

Research Methodology

The study of the AI in healthcare market is based on a combination of primary and secondary research methodologies, supported by data validation and analytical modeling to ensure accuracy and reliability.

Market Definition: AI in Healthcare Market

The AI in Healthcare Market consists of software solutions or platforms, algorithms, and integrated solutions that utilize artificial intelligence (AI) technologies such as machine learning (ML), deep learning (DL), natural language processing (NLP), vision, and generative artificial intelligence (GAI) to evaluate various types of data such as clinical, imaging, genomic, operational, and patient-generated data. These AI in Healthcare applications include but are not limited to:

1) Diagnosing diseases

2) Interpreting images

3) Supporting clinical decisions

4) Developing drugs

5) Creating virtual health assistants

6) Monitoring patients remotely

7) Managing revenue cycles

8) Automating hospital workflows.

The AI in Healthcare market includes both hardware and software, as well as services associated with those technologies, that can be deployed using either cloud-based or on-premise models in hospitals, clinics, pharma/biotech companies, insurance companies, and research facilities.

Key Stakeholders

The AI in healthcare market involves a diverse ecosystem of stakeholders:

- AI Software Providers

- Cloud Infrastructure Providers

- Electronic Health Record (EHR) Vendors

- Medical Device and Diagnostic Companies

- Pharmaceutical and Biotechnology Companies

- Healthcare Providers

- Health Insurance and Payer Organizations

- Contract Research Organizations

- Data and Interoperability Providers

- Regulatory and Standards Organizations

- Research Institutions and Academic Organizations

- Patients and Consumers

Key objectives of the Study

- To define, describe, analyze, segment, and forecast the AI in healthcare by offering type, by application type, by function type, by deployment type, by tool type, by end user.

- To describe and forecast the market for four key regions: North America, Europe, Asia Pacific, and Rest of the World.

- To provide detailed information regarding key drivers, restraints, opportunities, and challenges influencing market growth

- To strategically analyze the micro indicators with respect to individual growth trends, prospects, and contributions to the overall market size

- To analyze opportunities for stakeholders in the ai in healthcare industry and emphasize on competitive landscape of the market.

- To develop competitive benchmarking of the key market players based on technology specifications and end users.

- To strategically profile key players and comprehensively analyze their product portfolio offerings, and core competencies

- To analyze competitive developments, such as launches and approvals, agreements, mergers and acquisitions, partnerships, joint ventures, investments and expansions, and collaborations, ai in healthcare domain.

Need deeper insights on this market?

Get full report access with detailed forecasts, competitive analysis, and segmentation.

1. Research Approach

This research employs a systematic approach by using primary research along with secondary research to achieve full coverage and accuracy of information about the ai in healthcare sector. Through this approach, the current market trends in terms of consumer behavior, technological developments, and competitive environment can be analyzed thoroughly.

Secondary Research

Secondary research involves the collection of data from reliable sources such as industry databases, company annual reports, investor presentations, and regulatory filings. This process helps in understanding market trends, identifying key players, and gathering technical and commercial insights.

A comprehensive database of leading companies and market participants is developed through secondary research to support further analysis.

Primary Research

Primary research is conducted to validate findings from secondary research and to gain deeper insights into market dynamics. Interviews are carried out with industry stakeholders across both demand and supply sides, including executives such as CXOs, Vice Presidents, and Directors from business development, marketing, and product teams.

Data is collected through structured questionnaires, email interactions, and telephonic interviews across key regions including North America, Europe, Asia-Pacific, and Rest of the World.

Market Size Estimation

Market size estimation is performed using both top-down and bottom-up approaches. Key market players are identified, and their revenues are analyzed to estimate the overall market size.

The market is further segmented based on:

- Product and service mapping across regions

- Adoption patterns across key application segments

- Insights gathered through primary and secondary research

Data Validation and Research Design

After estimating the overall market size, the data is validated using triangulation methods and market breakdown techniques to ensure accuracy and consistency. Both demand-side and supply-side factors are considered to refine the analysis.

The final data is validated through multiple sources to ensure reliability and to provide accurate insights across all market segments and regions.

2. Assumptions of the Study

The analysis of the AI in healthcare market is based on the following key assumptions:

- Trends in the industry are drawn from historical data and current information within the sector

- The future outlook is underpinned by constant economic conditions in the absence of shocks to the market

- The rate of adoption for ai in healthcare will rise steadily in all important regions

- Advancements in AI, Automation, etc, will continue to drive growth in the AI in Healthcare market.

- The income statement and market share figures are estimated using available information from the industry and publicly available data

- The exchange rate and price trends will not be greatly affected during the forecast period

Scope and Limitations

Scope of the Study

This report offers an exhaustive overview of the global AI in healthcare market and includes the following components:

- Summary of market size, growth trends, and projections

- Carefully segmented market based on offering type, application type, function type, deployment type, tool type, end user and geography

- Discussion of primary factors influencing the market

- Competitor analysis

- Insights into regional and national market performance

Limitations of the Study

Despite the best efforts being made to keep the results accurate, the study does suffer from some limitations:

- It has been done using both primary and secondary data that come with their own constraints

- Rapid developments in technology might affect the future course of market dynamics

- Some figures are only approximations due to lack of public disclosure

- The report is not an insurance against any disruptions in macroeconomics and geopolitics

- Future forecasts are indicative and subject to change due to altered industry dynamics

3. Data Triangulation and Market Breakdown

Data triangulation involved the combination of primary research, secondary research, and the Wissen Research analysis. Once the data points were sourced from the secondary market research, we sanitized the data points to make the market sizing and growth forecast more accurate by developing our own assumptions based on the inputs and insights we gather through the primary interviews with the industry experts. Once the data was thoroughly validated through primary interviews from both, demand and supply side of the market, our team of analyst and other team members involved finalized the market sizing and growth forecast.

Data Triangulation Methodology

Sources: U.S. Food and Drug Administration, European Medicines Agency, National Institute of Standards and Technology, International Organization for Standardization, International Electrotechnical Commission, Federal Communications Commission, Occupational Safety and Health Administration, American National Standards Institute, Device Coordination Group, Company Website, Press Releases, Annual Reports, Paid Data Sources, and Wissen Research Analysis.

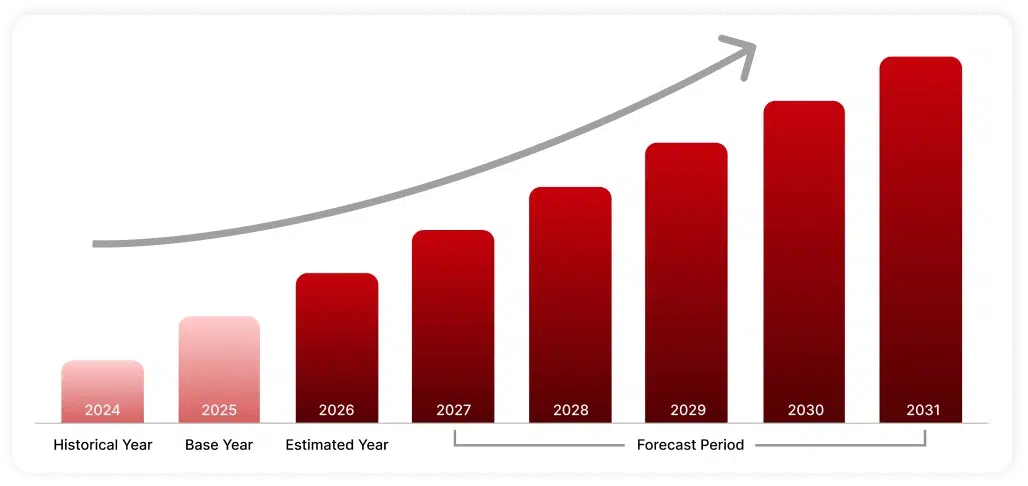

4. Years Framework

5. Bottom up approach (Demand Side) and Top down approach (Supply Side)

Bottom-Up Approach (Demand Side Approach):

Determining the market size through the consolidation of demand among end-users, sectors, and geographic areas, which are calculated according to real-world demand conditions.

Top Down Approach (Supply Side Approach):

Calculating the market size through revenue and performance of the industry and its important companies, allocating the market size among various sectors.