Sustainable Pharmaceutical Packaging Market

Global Industry analysis, Size, Share, Growth, Trends, and Forecast 2026-2031

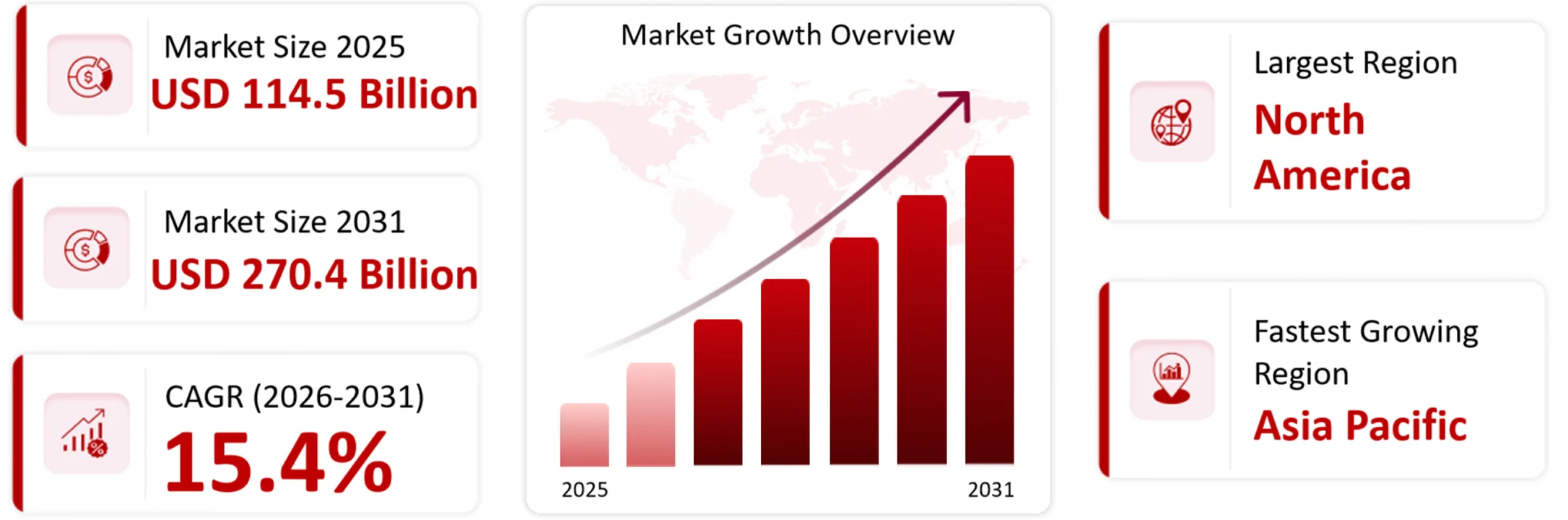

The global sustainable pharmaceutical packaging market is projected to reach USD 270.4 billion by 2031, growing at a CAGR of 15.4% during the forecast period.

| Market Size 2025 | Market Size 2031 | CAGR (2026-2031) | Largest Region | Fastest Growing Region |

|---|---|---|---|---|

| USD 114.5 Billion | USD 270.4 Billion | 15.4% | North America | Asia Pacific |

Market Overview

The global sustainable pharmaceutical packaging market is growing largely due to increased focus on sustainability by pharmaceutical companies as well as increased focus on long-term sustainability goals and regulatory compliance. This is largely driven by regulatory changes that have become more stringent on the pharmaceutical manufacturers, the concern for pharmaceutical waste has become a topic of concern, the corporate ESG commitments have had an increasing focus, and the continued rise in demand for sustainable healthcare supply chains has driven the trend toward sustainable packaging solutions. The value of the market in 2025 USD 114.5 billion and projected to be USD 270.4 billion by 2031 with a compound annual growth rate (CAGR) of 15.4% from 2026 through to 2031.

Technology Overview

The primary goal for sustainable pharmaceutical packaging is to develop an environmental responsible manner of packaging products as well as ensuring that the effectiveness, safety and stability of the pharmaceutical product is maintained over the entire duration of its life cycle. Many organizations are using alternate forms of materials which are recyclable (for example, biobased polymers), environmentally friendly (biodegradable), and low-weight packaging’s. These alternate forms help to reduce the amount of material consumed during the manufacturing process and to decrease the volume of packaging debris produced after the use of a particular product. Due to advances in the science of materials, many companies have access to new types of packaging that demonstrate improved environmental performance while providing the types of barrier properties (moisture, oxygen, contamination) that are required for pharmaceutical products. Furthermore, several companies are utilizing digital technologies (digital print) and lifecycle assessment tools to determine the effectiveness of their materials (cost), carbon footprint and overall sustainability of their packaging processes.

Key Growth Drivers

- Pharmaceutical manufacturers are implementing low-carbon reusable packaging solutions across their supply chains due to stronger enforcement of Scope 3 GHG emissions reductions which drive the sustainable pharmaceutical packaging market.

- Increase in the regulation of recyclable packaging (e.g., PPWR regulations), which is causing many manufacturers to move away from the traditional multi-material formats toward compliant, alternative packaging formats.

- The development of mono-material barrier packaging technology enables pharmaceutical companies to manufacture recyclable products while maintaining product stability and/or protection.

- Extended Producer Responsibility Regulations are creating extra cost impacts on pharmaceutical companies for producing difficult-to-recycle packaging waste.

- Growth in the adoption of green tender framework and sustainability-based procurement by hospitals strengthening the demand of environmentally friendly packaging.

Sustainable Pharmaceutical Packaging Market Key Highlights

Need deeper insights on this market?

Get full report access with detailed forecasts, competitive analysis, and segmentation.

Sustainable Pharmaceutical Packaging Market Trends

There are some key developments in the sustainable pharmaceutical packaging, such as: the trend toward more recyclable mono-materials; increasing use of post-consumer recycled plastic (PCR) materials; more paper-based secondary packaging; expansion of lightweight (GLP) pharmaceutical glass products; the adoption of smart and traceable packaging technologies and the increasing investment in bio-based polymer materials. Companies within the pharmaceutical field will focus on reducing their packaging waste, reducing their carbon footprint, increasing their recyclability and complying with the growing number of sustainability regulations that apply to their global supply chains in the pharmaceutical industry.

Transition from Conventional Multi-Material Pharmaceutical Packaging Toward Recyclable Mono-Material Structures

A major trend in this particular industry/sector is the movement away from traditional multi-material pharmaceutical packaging toward mono-material recyclable structures. The traditional blister packs and flexible types of pharmaceutical packaging on the market today are usually comprised of several layers of plastics & aluminum material which are very difficult (if not impossible) to recycle by normal means or through the existing landfill system. There are currently various types of mono-material barrier solutions made of polypropylene and polyethylene that have been developed by packaging manufacturers for use in pharmaceutical applications. These mono-materials can provide moisture protection, oxygen barriers, and drug stability as has historically been provided by conventional multi-material packs while still remaining 100% mechanically recyclable. These mono-material barriers are becoming widely used by pharmaceutical manufacturers as they strive to meet their emerging recyclability goals or comply with circular economy targets.

Increasing Integration of Post-Consumer Recycled Materials and Lightweight Packaging Formats

Another emerging trend, to coincide both with an increase of post-consumer recycled materials and a rise in lightweight formats of packaging in the pharmaceutical sector, is the integration of these into production of pharmaceutical packaging. Pharmaceutical companies have begun to substitute part of their use of virgin plastics with PCR resin in bottles, closures and secondary packaging. Additionally, many companies are investing in the development of lighter weight glass containers (lightweight) and downgauged flexible products for their packaging, to reduce both transportation greenhouse gas emissions and material usage. This trend is being further accelerated due to corporations having established ESG goals and corporate commitments to reducing carbon emissions as well as by regulations mandating improvements in sustainability of packaging while still meeting all the necessary requirements of pharmaceutical safety, sterility and regulatory compliance.

Key Players in the Sustainable Pharmaceutical Packaging Market

Leading companies in the Sustainable Pharmaceutical Packaging market are focusing on innovation, strategic partnerships, and expansion of health-centric features to strengthen their market position.

Strategic Activities Within the Sustainable Pharmaceutical Packaging Market

Amcor plc (Switzerland) and Berry Global Group Inc (US) merged together to provide improved global healthcare packaging, enhanced recyclable packaging technology, greater integration of post-consumer recycled materials into products across the pharmaceutical and consumer packaging industries as well as capabilities related to the sustainable development of all their respective products.

Becton, Dickinson and Company (United States) and Envetec Sustainable Technologies (Ireland) completed a feasibility study in January 2026 demonstrating closed-loop recycling of healthcare plastics, including Petri dishes, syringes, PET tubes, and medical packaging materials, supporting circular economy adoption and reducing virgin plastic dependency across healthcare and pharmaceutical supply chains.

SCHOTT Pharma (Germany) expanded its EVERIC® portfolio with EVERIC® lyo & amber, an advanced amber glass vial designed for highly light-sensitive biologics and ADC therapies. The solution combined FIOLAX® amber pharma glass with hydrophobic coating technology to improve lyophilization efficiency, reduce product loss, and enhance primary-container light protection for high-value oncology drugs.

Key Players in the Sustainable Pharmaceutical Packaging Market

The market for sustainable pharmaceutical packaging is seeing continued expansion as pharmaceutical firms increasingly turn away from traditional types of packaging material, in favor of scalable, environmentally responsible forms of packaging that can be integrated into their entire commercial drug supply chains. With continued market expansion comes increased support for genuine investment in recyclable material, lightweight packaging forms, post-consumer recycled content and low-carbon manufacturing processes, instead of limited pilot studies for sustainable packaging solutions. Pharmaceutical manufacturers are making sustainable packaging solutions a priority due to their ability to reduce wasted materials, enhance recyclability, decrease transportation-related emissions and meet compliance goals and provide product safety and sterility. Along with an increased focus on ESG (Environmental, Social and Governance) initiatives and a greater emphasis on meeting global targets for reducing carbon emissions; pharmaceutical companies are increasingly implementing sustainable packaging practices directly into the way they purchase packaging items, the way they manufacture drug products and overall supply chain strategies.

Sustainable packaging solutions are being adopted by numerous pharmacy & health care product businesses mainly for eco-friendly purposes, or to decrease overall harm to the planet, for increased product performance through greater use of materials, and also as a response to political pressures from increased health care regulation changes related to packaging use in supply chain. Key application areas for sustainable pharmaceutical or health care products include: recyclable blister packs; sustainable pharmacy bottles; light weight glass vials; paper based secondary packaging; recyclable flexible packaging’s; and eco-friendly closures or caps. Pharmaceutical manufacturers are also beginning to produce more recyclable used mono-material polymer packages compared to previous years by utilizing ex-consumer recycled plastic in order to obtain improved recyclability standards while still adhering to all existing packaging barriers, as well as the stability requirements for drugs. As part of sustainable packaged product designs, additional technological advances being integrated into the design of sustainable packaging include smart packaging technologies, such as, QR code systems, RFID tracking systems, and connected labelling systems, which will provide improved traceability, authentication through inventory monitoring and improved engagement of patient and pharmacist.

There are many ways that the sustainable pharmaceutical packaging industry is offering new possibilities for manufacturers of packaging materials, suppliers of materials to the pharmaceutical industry, and those producing environmentally friendly solutions to health care. Pharmaceutical companies want more recyclable and renewable options, as well as lower carbon packaging choices, that meet their sustainability goals and their regulatory obligations. As a result, the industry as a whole will begin to see more inventive and differentiated products by establishing additional means to produce and use materials in packaging. In addition, the growth of biologics, injectables, and temperature-sensitive pharmaceuticals is increasing the demand for advanced, innovative, and sustainable barrier packaging technologies. Emerging and developing markets within pharmaceutical manufacturing will create opportunities for long-term growth as capacity increases and healthcare infrastructure develops in those regions. Additionally, an increase in investment directed at new circular economy programs, improved recovery of packaging, and improved sustainable manufacturing methods should help to speed up the introduction of new products and also create additional demand for established manufacturers and their products throughout the liquid and solid drug packaging supply chain.

There are a number of major challenges within the sustainable pharmaceutical market that may slow down the adoption of these products to a wider market. Due to the need to provide a high level of protection for pharmaceutical products against moisture, oxygen, contamination, and temperature fluctuations, sustainable materials must provide the same performance as traditional packaging materials without decreasing the safety of the product or affecting the shelf life of a product. Manufacturers are especially concerned about the higher cost of buying bio-based, recyclable, and biodegradable materials when competing against lower cost traditional packaging in cost-sensitive markets. The limited ability to recycle pharmaceutical packaging adds to the difficulty of collecting, sorting and recovering pharmaceutical products after they have been utilized.

The adoption of sustainable packaging is growing rapidly in China due to stricter enforcement of environmental policies, increased exports of prescribed medicine from China to other countries, and increased investment into initiatives that will support the circular economy. The high demand for environmentally friendly packaging is also being driven by increased production of generic pharmaceuticals in India, new regulations in India regarding plastic waste, and an increased commitment of pharmaceutical companies in India to operate in a more sustainable manner. In addition, there are a number of other factors contributing to the continued increase in sustainable packaging adoption throughout the region: the increasing accessibility of healthcare across the region; the increasing volume of production of pharmaceuticals in the Asia-Pacific Region; the increasing number of recycling businesses throughout the Asia-Pacific Region; as well as the increasing number of government and industry initiatives designed to promote sustainable industrial development and environmentally friendly packaging solutions.

Sustainable Pharmaceutical Packaging Market Dynamics

Drivers: Regulatory Pressure and Sustainable Procurement Initiatives

Sustainable packaging has become a key driver for growth in the pharmaceutical packaging sector as pharmaceutical manufacturers continue to encounter mounting regulatory requirements regarding the environment and carbon minimizing obligations. Sustainability studies conducted by major pharmaceutical corporations indicate that packaging-related emissions and waste represent a large proportion of the environmental impact generated by pharmaceutical supply chains. At the same time that government agencies and regulatory organizations are imposing mandates regulating the recyclability of packaging, reduction requirements for plastic use, EPR laws, and requirements for the disclosure of carbon emissions which have a direct impact on packaging processes associated with the pharmaceutical industry collectively. As hospitals, a healthcare system or a pharmacy organization chooses suppliers based on their sustainability practices, pharmaceutical manufacturers are moving faster to invest in recyclable blister packages, mono-material packaging, lightweight packaging and post-consumer recycled materials to meet environmental regulations, improve their ESG scores, reduce waste disposal costs, and improve their long-term competitive position in the global healthcare supply chain.

Challenges: Material Performance, Regulatory Compliance, and Recycling Infrastructure

Maintaining the safety and regulatory compliance of medicines while developing ways to improve the environmental performance of drug packaging presents the biggest challenge to creating sustainably packaged medicines. Examples of this include requiring pharmaceutical packaging to provide a strong barrier against moisture; an oxygen barrier; the ability to avoid contamination; and the ability to maintain the stability of the product for a specified period of time. Bio-based and recyclable materials are not able to provide the same performance levels that multi-layer plastic and aluminium packaging can provide at this time. It is also necessary for sustainable packaging to undergo extensive regulatory testing and approval prior to commercialization. Additionally, there are limitations to the recycling infrastructure for pharmaceuticals; complex segregation requirements concerning waste; and inconsistency in recycling by region that limit the large-scale adoption of sustainable packaging solutions.

Opportunity: Mono-Material Packaging and Circular Economy Integration

The market offers large opportunities for growth due to recyclable mono-material pharmaceutical packaging systems. Traditional blister packs often use a combination of plastics and aluminium, which makes recycling difficult in conventional waste management systems. By utilizing advances in polymer engineering, mono-material solutions made from polypropylene (PP) and polyethylene (PE) can furnish barriers to moisture and oxygen while being designed for recyclable purposes. Manufacturers are now putting their efforts into lightweight packaging, closed-loop partnerships for recycling and integrating post-consumer recycled material in an attempt to reduce the use of virgin plastics as well as lower CO2 emissions across the globe in the life sciences supply chains.

Technology and Market Insights

The sustainable pharmaceutical packaging industry is moving away from conventional recyclable packages to more sophisticated, sustainable packaging systems that emphasize carbon offsetting materials, and a closed-loop economy in addition to being a highly efficient form of packaging. As a result, packaging manufacturers have an increasing selection of options available for creating sustainable packaging solutions such as the use of mono-material barrier technologies, lightweight glass bottles, plastics made of post-consumer recycled sources, paper-based packaging, and bio-based polymers. The demand for recyclable pharmaceutical blister packaging and sustainable flexible packaging is growing rapidly because of stricter regulations concerning the environment and the corporate commitment to expanded ESG programs in an effort to create a more sustainable global manufacturing solution. Pharmaceutical manufacturers are seeking solutions in their packaging systems that provide a reduction in the excess waste that is created, increasing the recyclability of the packaging, decreasing the amount of CO2 emitted during transportation, while maintaining the strictest standards for safety and sterility of the product being delivered to the customer.

Technology Scope and Products

Sustainable Pharmaceutical Packaging Detailed Market Segmentation

Want detailed insights from this report?

Industry Developments and Competitive Landscape

The growth of the sustainable pharmaceutical packaging market has been spurred by innovations surrounding recyclable materials and circular economy solutions along with improvements made in barrier technology. As a result, manufacturers are concentrating their efforts on creating either mono-material structures or lightweight glass containers to enhance recyclability and reduce carbon footprint as well as develop options made from post-consumer recycled materials; these can assist with both enhancing recyclability while also reducing carbon emissions. Manufacturers have also made significant advancements in polymer engineering, sustainable coating technology to allow for moisture protection and oxygen barriers as well as maintaining the stability of the drug while also reducing the complexity of the material used in their products. Furthermore, through the integration of smart packaging technologies, such as QR codes, RFID tracking, and digital serialization systems, more emphasis has been placed on improving traceability, regulatory compliance, and supply chain efficiency.

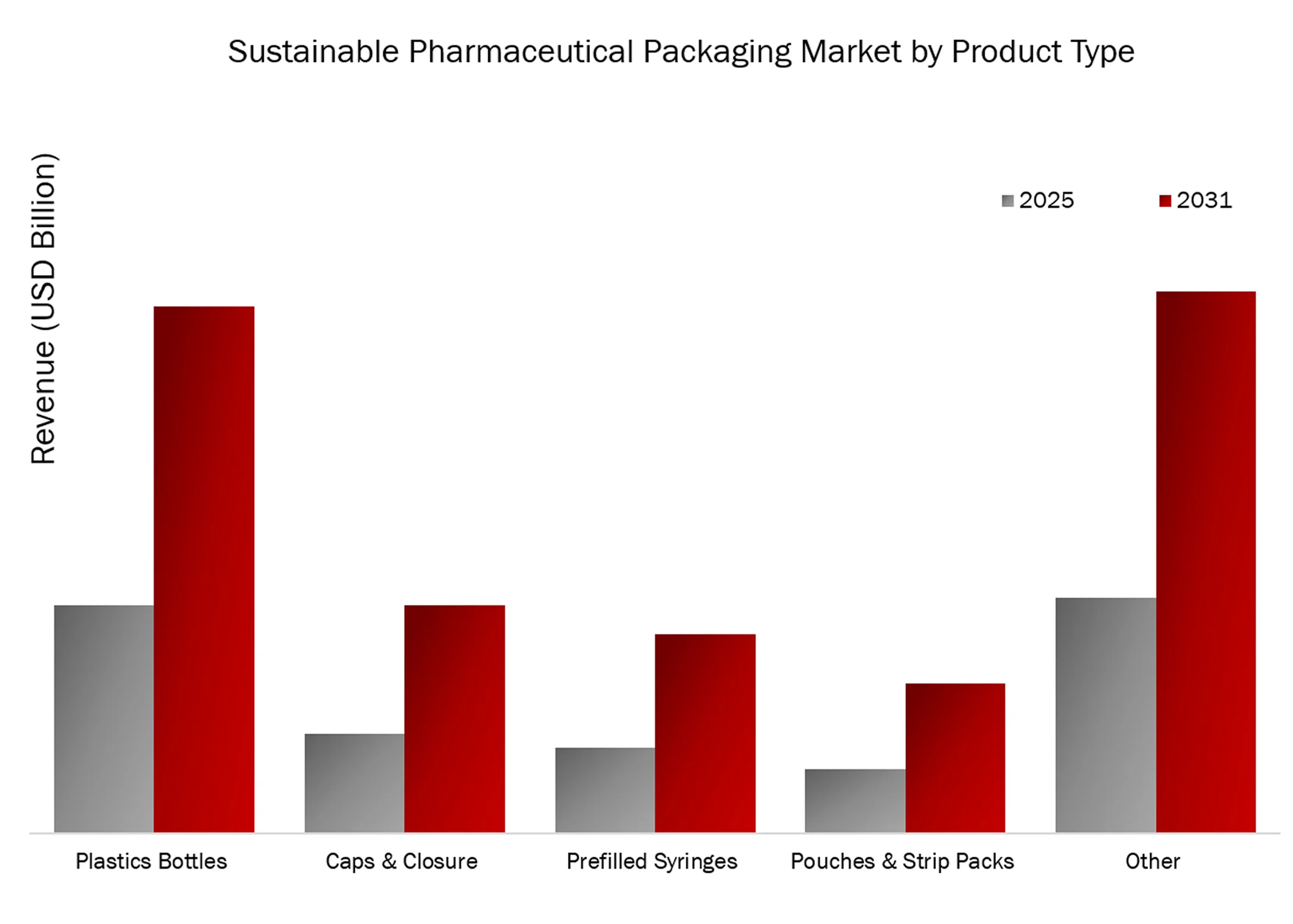

The largest chunk of the market share in sustainable pharmaceutical packaging held by the plastic bottle by product type. The fact that most pharmaceutical companies will use plastic bottles made from one material (HDPE or PET) allows for an easier recycling process and less money to change over these types of bottles in the global marketplace in the year 2025.

-

To facilitate the transition to sustainable packaging, various FDA certified pathways for the manufacture and commercialization of recycled HDPE and PET containers have led to an increase in the use of sustainable plastic bottle packaging across North America.

-

The vast majority of municipal recycling programs currently in existence were already set up to allow for advanced collection methods of PET and HDPE plastic bottles, thereby providing for better recycling capability in the case of simple recycling processes versus more complex multi-material types of pharmaceutical packaging.

-

The majority of volume of all sales of pharmaceutical products will continue to increase, therefore impacting the growth in rigid plastic packaging products across the supply chain in healthcare.

-

Pharmaceutical companies have placed a high priority on using plastic bottles made from recycled content because they provide companies with a low-risk way of reducing their use of virgin plastics and assist their attempt to meet their ESG goals and/or reduce their carbon footprints.

-

Several of the largest packaging companies Amcor plc. (Switzerland) and Berry Global Group, Inc. (United States) have made major investments into recyclability of traditional rigid plastic packaging; therefore, maintaining the leadership of plastic bottle volume in sustainable packaging.

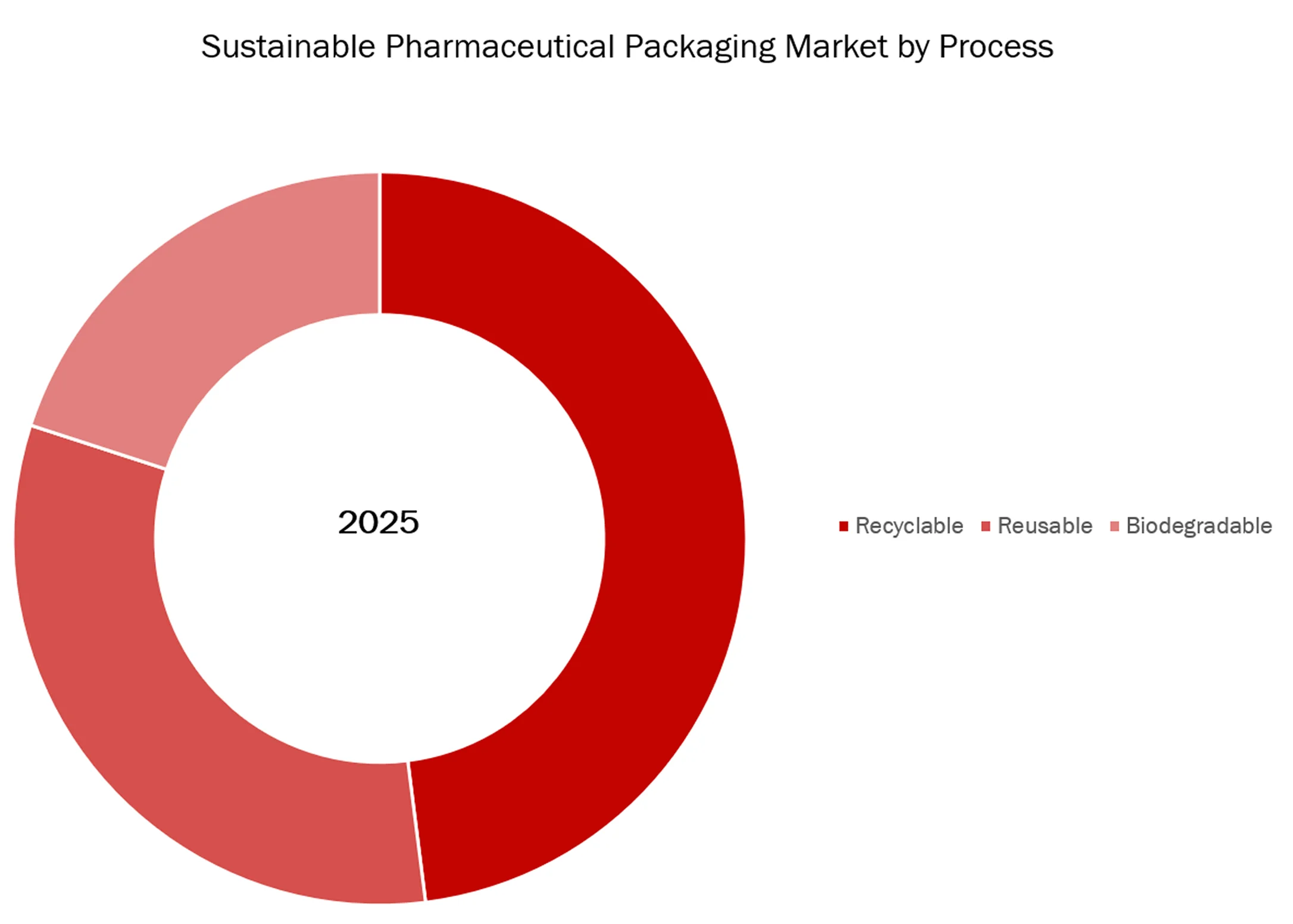

Recyclable packaging commanded the highest proportion of the sustainable pharmaceutical packaging market in 2025 because they seamlessly fit into the current municipal waste and recycling systems around the globe.

-

Due to the existence of established recycling ecosystems for PET, HDPE, polypropylene and aluminum, pharmaceutical companies were able to implement recyclable packaging at an accelerated rate compared to biodegradable or reusable packaging options throughout their entire commercial supply chain.

-

Stringent requirements imposed by the FDA with respect to sterility and contamination control also provided support for the adoption of recyclable pharmaceutical packaging since the recycling process removes contaminants and still allows the end product to meet the required standards for safety and performance as a pharmaceutical-grade material.

-

In addition, recyclable materials provide better, long term moisture, oxygen and stability protection compared to biodegradable materials resulting in recyclable packaging being better suited for products that will be stored in sensitive pharmaceutical environments or that will require longer shelf lives.

-

Pharmaceutical companies have prioritized recyclable packaging because converting an existing production line from a reusable packaging infrastructure system to a mono-material recyclable format will require much lower capital investment than continuing with an existing reusable packaging infrastructure system.

-

Leading packaging manufacturers such as Amcor plc (Switzerland) are focusing investments on developing sustainable packaging technologies based on recyclable packaging materials; this has led to accelerated large scale adoption of recyclable packaging technologies throughout commercial pharmaceutical distribution networks and enhanced the recyclable packaging sector’s overall market leadership position.

North America accounted for 40-45 percent of the worldwide revenue for pharmaceuticals with a manufacturing market share. As a result, North America is the leading sustainable pharmaceutical packaging market by far.

-

The high level of pharmaceuticals produced in North America means significantly more dollars were spent than Europe on sustainable packaging such as bottles, cartons, blister packs, labels, and logistics packaging materials

-

With healthcare spending in the United States being over $4.5 trillion, it allowed pharmaceutical companies to pass on the extra costs associated with recyclable and medically certified sustainable packaging materials.

-

Higher profit margins in North America have led to a faster adoption of modern and advanced technologies in sustainable packaging, while Europe’s price control systems created less incentive for voluntary investment on a large scale.

-

Major packaging manufacturers have placed their sustainable packaging infrastructure investments strategically in the U.S. near the largest pharmaceutical manufacturing hubs, leading to a significant increase in the available production capacity for recycled pharmaceutical packaging.

-

North America retains the lead in sustainable packaging by having a streamlined approval process (Letter of No Objection) necessary for faster commercialization of the use of recycled pharmaceutical grade plastics, resulting in higher levels of sustainable packaging used in North America.

What This Report Covers

This report provides a comprehensive analysis of the sustainable pharmaceutical packaging market, offering insights into key trends, growth drivers, challenges, and future opportunities. It is designed to support strategic decision-making through a combination of quantitative data and qualitative analysis.

Specifically, the report covers:

Market Overview & Definition: Overview of the market scope, structure, and key terminology.

Market Size & Forecast: Historical data and future projections across key segments and regions.

Key Market Trends: Insights into emerging trends, technological advancements, and evolving demand patterns.

Drivers, Restraints & Opportunities: Analysis of key factors influencing market growth.

Competitive Landscape: Overview of major players, their strategies, and recent developments.

Detailed Patent Analysis which includes, top assignees, geography focus of top assignees, legal status, technology evolution, key patents and patent trends and innovations

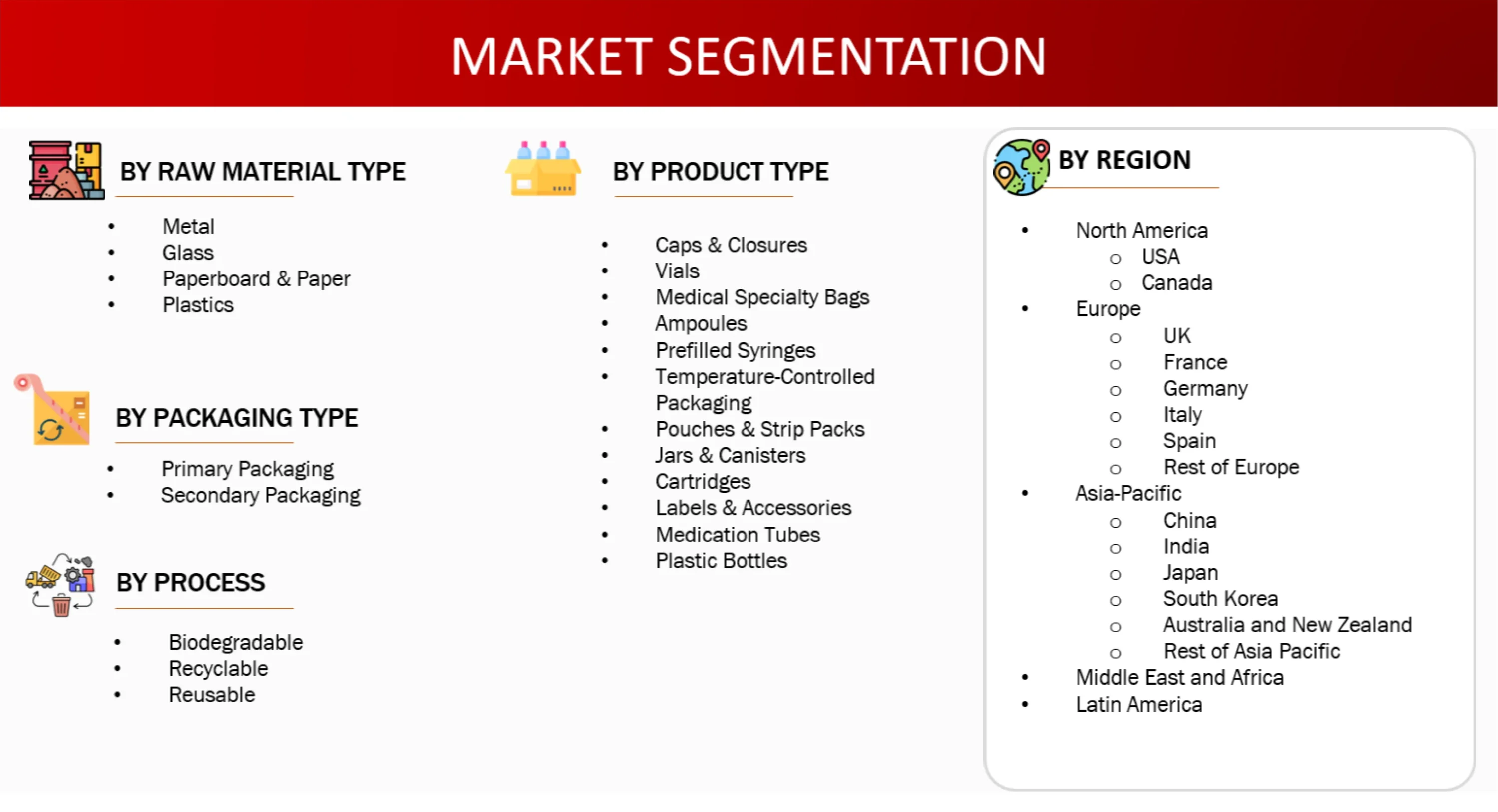

Segmentation Analysis: Breakdown by product, raw material, process, packaging & region.

Segmentation Analysis: Breakdown by product, raw material, process, packaging & region.

Future Outlook: Strategic insights and future market direction.

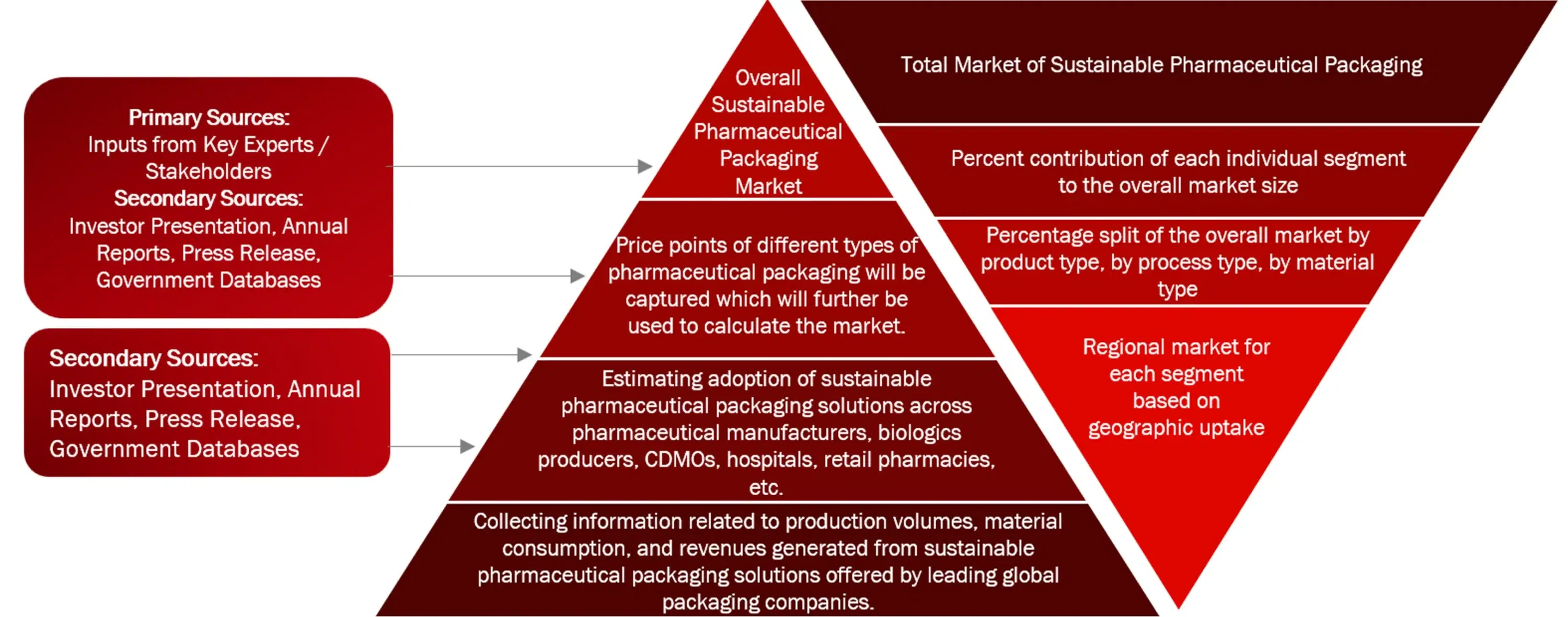

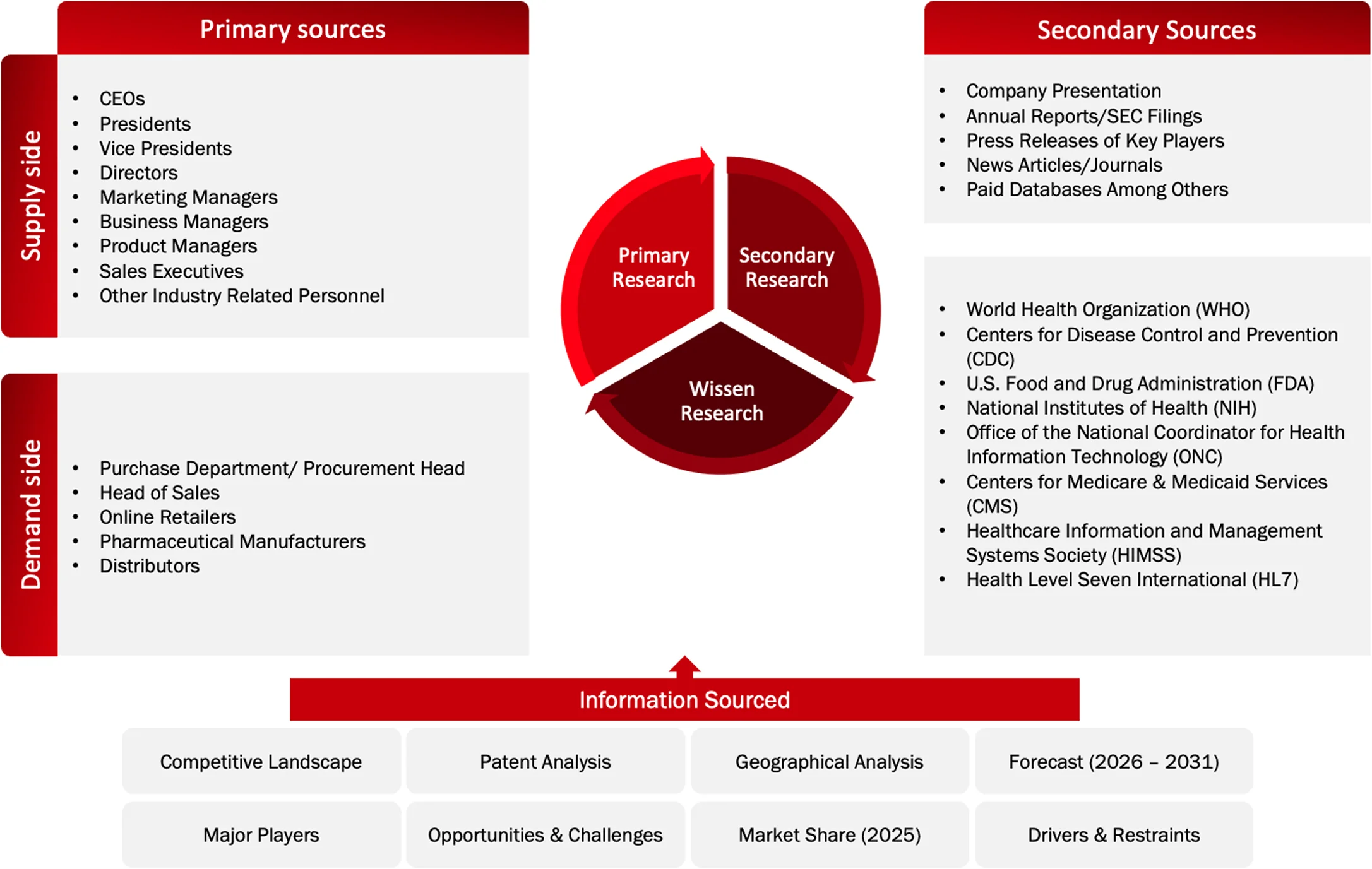

Research Methodology

The study of the sustainable pharmaceutical packaging market is based on a combination of primary and secondary research methodologies, supported by data validation and analytical modeling to ensure accuracy and reliability.

Market Definition: Sustainable Pharmaceutical Packaging Market

Sustainable pharmaceutical packaging comprises three types of pharma packaging’s: primary, secondary and tertiary packaging – all crafted from environmentally-friendly materials. They aim to limit environmental impacts while maintaining the same level of safety for pharmaceutical products. The range of sustainable pharmaceutical packaging products includes recyclable mono-material packaging; post-consumer recycled plastics; bio-based polymers; lightweight glass containers; paper-based packaging; flexible sustainable packaging; and various advanced barrier technology packaging. Sustainable pharmaceutical packaging applications include but are not limited to:

1) Bottle

2) Blister pack

3) Vial and ampoule

4) Syringe and injectable product

5) Carton or label

6) Cold chain

7) Packaging for medical devices

8) Logistic and transport packaging for pharmaceuticals

There are many companies involved in providing sustainable pharmaceutical packaging; packaging manufacturers, contract development and manufacturing organizations (CDMOs), biologics manufacturers, hospital systems, retail pharmacy chains, and healthcare distribution organizations.

Key Stakeholders

The sustainable pharmaceutical packaging market involves a diverse ecosystem of stakeholders:

- Pharmaceutical Manufacturers (drug producers adopting recyclable, low-carbon, and regulatory-compliant packaging solutions across primary and secondary packaging applications)

- Packaging Material Suppliers (providers of recyclable polymers, bio-based plastics, pharmaceutical glass, paperboard, coatings, and post-consumer recycled materials)

- Pharmaceutical Packaging Companies (manufacturers of bottles, blister packs, vials, syringes, closures, cartons, labels, and sustainable flexible packaging solutions)

- Healthcare Providers and Hospitals (health systems promoting sustainable procurement standards and environmentally responsible pharmaceutical supply-chain practices)

- Contract Packaging Organizations (CPOs) (outsourced pharmaceutical packaging service providers supporting sustainable packaging conversion and manufacturing operations)

- Pharmaceutical Distributors and Logistics Companies (supply-chain operators utilizing lightweight, recyclable, and low-emission transport packaging systems)

- Recycling and Waste Management Companies (organizations managing pharmaceutical packaging collection, sorting, recovery, and circular economy recycling processes)

- Consumers and Patients (end users increasingly supporting recyclable, environmentally responsible, and low-waste pharmaceutical packaging products)

Key Objectives of the Study

- To define, describe, analyze, segment, and forecast the sustainable pharmaceutical packaging by product type, by process type, by material type, and by packaging type.

- To describe and forecast the market for four key regions: North America, Europe, Asia Pacific, and Rest of the World.

- To provide detailed information regarding key drivers, restraints, opportunities, and challenges influencing market growth

- To strategically analyze the micro indicators with respect to individual growth trends, prospects, and contributions to the overall market size

- To analyze opportunities for stakeholders in the sustainable pharmaceutical packaging industry and emphasize on competitive landscape of the market.

- To develop competitive benchmarking of the key market players based on technology specifications and end users.

- To strategically profile key players and comprehensively analyze their product portfolio offerings, and core competencies

- To analyze competitive developments, such as launches and approvals, agreements, mergers and acquisitions, partnerships, joint ventures, investments and expansions, and collaborations, sustainable pharmaceutical packaging domain.

Need deeper insights on this market?

Get full report access with detailed forecasts, competitive analysis, and segmentation.

1. Research Approach

This research employs a systematic approach by using primary research along with secondary research to achieve full coverage and accuracy of information about the sustainable pharmaceutical packaging sector. Through this approach, the current market trends in terms of consumer behavior, technological developments, and competitive environment can be analyzed thoroughly.

Secondary Research

Secondary research involves the collection of data from reliable sources such as industry databases, company annual reports, investor presentations, and regulatory filings. This process helps in understanding market trends, identifying key players, and gathering technical and commercial insights.

A comprehensive database of leading companies and market participants is developed through secondary research to support further analysis.

Primary Research

Primary research is conducted to validate findings from secondary research and to gain deeper insights into market dynamics. Interviews are carried out with industry stakeholders across both demand and supply sides, including executives such as CXOs, Vice Presidents, and Directors from business development, marketing, and product teams.

Data is collected through structured questionnaires, email interactions, and telephonic interviews across key regions including North America, Europe, Asia-Pacific, and Rest of the World.

Market Size Estimation

Market size estimation is performed using both top-down and bottom-up approaches. Key market players are identified, and their revenues are analyzed to estimate the overall market size.

The market is further segmented based on:

- Product and service mapping across regions

- Adoption patterns across key application segments

- Insights gathered through primary and secondary research

Data Validation and Research Design

After estimating the overall market size, the data is validated using triangulation methods and market breakdown techniques to ensure accuracy and consistency. Both demand-side and supply-side factors are considered to refine the analysis.

The final data is validated through multiple sources to ensure reliability and to provide accurate insights across all market segments and regions.

2. Assumptions of the Study

The analysis of the sustainable pharmaceutical packaging market is based on the following key assumptions:

- • Trends in the industry are drawn from historical data and current information within the sector

- • The future outlook is underpinned by constant economic conditions in the absence of shocks to the market

- • The rate of adoption for sustainable pharmaceutical packaging will rise steadily in all important regions

- • Advancements in AI, connectivity, and lab-on-chip will continue to drive growth in the point-of-care testing market.

- • The income statement and market share figures are estimated using available information from the industry and publicly available data

- • The exchange rate and price trends will not be greatly affected during the forecast period

Scope and Limitations

Scope of the Study

This report offers an exhaustive overview of the international sustainable pharmaceutical packaging market and includes the following components:

- Summary of market size, growth trends, and projections

- Carefully segmented market based on products, platform, sample, end users, by mode of acquiring and geography

- Discussion of primary factors influencing the market

- Competitor analysis

- Insights into regional and national market performance

Limitations of the Study

Despite the best efforts being made to keep the results accurate, the study does suffer from some limitations:

- It has been done using both primary and secondary data that come with their own constraints

- Rapid developments in technology might affect the future course of market dynamics

- Some figures are only approximations due to lack of public disclosure

- The report is not an insurance against any disruptions in macroeconomics and geopolitics

- Future forecasts are indicative and subject to change due to altered industry dynamics

3. Data Triangulation and Market Breakdown

Data triangulation involved the combination of primary research, secondary research, and the Wissen Research analysis. Once the data points were sourced from the secondary market research, we sanitized the data points to make the market sizing and growth forecast more accurate by developing our own assumptions based on the inputs and insights we gather through the primary interviews with the industry experts. Once the data was thoroughly validated through primary interviews from both, demand and supply side of the market, our team of analyst and other team members involved finalized the market sizing and growth forecast.

Data Triangulation Methodology

Sources: U.S. Food and Drug Administration, European Medicines Agency, National Institute of Standards and Technology, International Organization for Standardization, International Electrotechnical Commission, Federal Communications Commission, Occupational Safety and Health Administration, American National Standards Institute, Company Website, Press Releases, Annual Reports, Paid Data Sources, and Wissen Research Analysis.

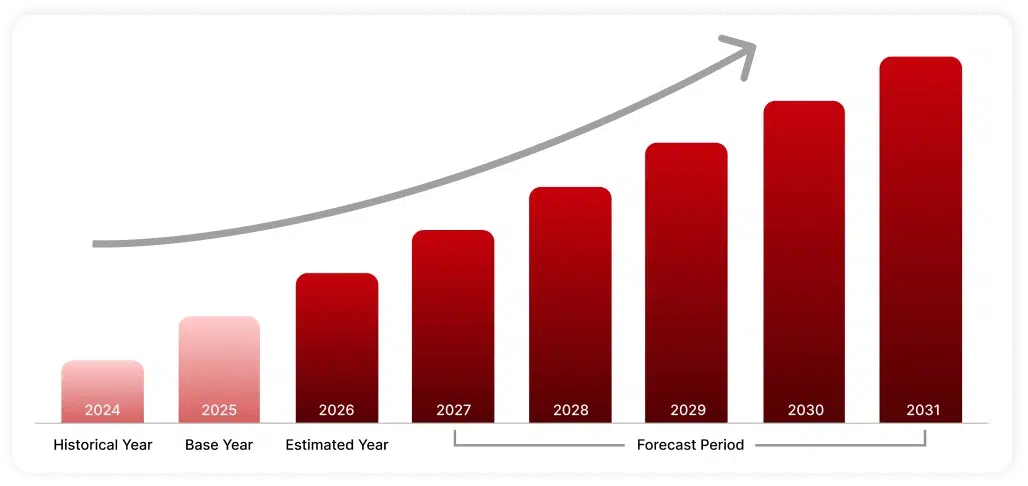

4. Years Framework

5. Bottom up approach (Demand Side) and Top down approach (Supply Side)

Bottom-Up Approach (Demand-Side Approach):

Determining the market size through the consolidation of demand among end-users, sectors, and geographic areas, which are calculated according to real-world demand conditions.

Top-Down Approach (Supply-Side Approach):

Calculating the market size through revenue and performance of the industry and its important companies, allocating the market size among various sectors.