Wissen Research analysed that the global aluminum extrusion market reached USD 120 billion in 2025 and will grow to USD 170 billion by 2030, growing at a CAGR of 7.2% during the forecast period from 2026 to 2030.

Aluminum Extrusion Market: Market Size, Trend, by Alloy Grade (6XXX, 1XXX, 5XXX), by Products (Solid Profiles, Semi-hollow Profiles, Hollow Profiles), by Surface Finish, by End Users, Region, Major Players – Global Forecast to 2030

Wissen Research analysed that the global aluminum extrusion market reached USD 120 billion in 2025 and will grow to USD 170 billion by 2030, growing at a CAGR of 7.2% during the forecast period from 2026 to 2030.

Global Market

Global aluminum extrusion market is anticipated to reach USD 170 billion by 2030 from USD 120 billion in 2025, growing at an annualized rate of 7.2% during the period, 2026-2030

Primary Application Area

The construction and automotive sectors remain key demand drivers, with rising infrastructure development and increasing adoption of lightweight materials in electric vehicles accelerating extrusion demand. Aluminum extrusions are widely used in window frames, curtain walls, structural components, and automotive body structures due to their durability and ease of fabrication. The growing shift toward electric mobility is further boosting demand, as lightweight extruded components contribute to improved vehicle efficiency and battery range.

Drivers

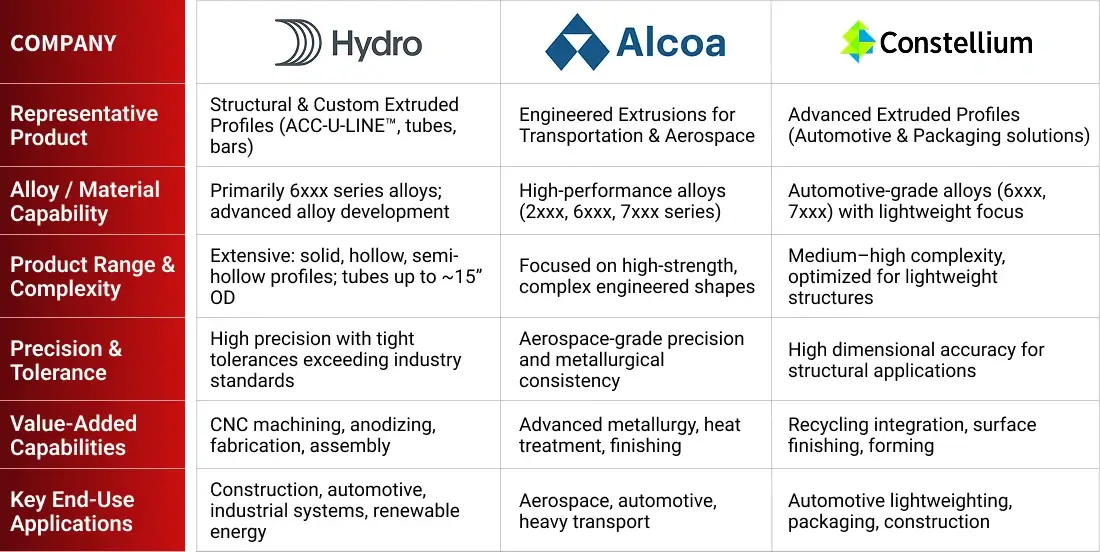

The aluminum extrusion market is experiencing steady growth driven by increasing demand for lightweight, durable, and corrosion-resistant materials across industries such as construction, automotive, electrical, and industrial manufacturing. Aluminum extrusions offer a high strength-to-weight ratio, design flexibility, and recyclability, making them a preferred material for structural and functional applications. Leading companies such as Norsk Hydro ASA, Alcoa Corporation, and Constellium are investing in advanced extrusion technologies, alloy development, and downstream fabrication capabilities to meet evolving industry requirements.

Innovations and Trends

Technological advancements and sustainability trends are reshaping the market, with a strong focus on recycled aluminum and low-carbon production processes. Manufacturers are increasingly adopting closed-loop recycling systems and energy-efficient extrusion technologies to reduce carbon emissions and production costs. In addition, advancements in precision extrusion, surface finishing, and alloy optimization are enabling the production of complex, high-performance profiles for specialized industrial applications.

Despite positive growth prospects, the market faces challenges such as volatility in aluminum prices, high energy consumption in primary aluminum production, and supply chain fluctuations. In response, companies are focusing on vertical integration, recycling, and long-term raw material sourcing strategies to ensure cost stability and supply security while maintaining product quality and competitiveness.

Asia-Pacific

Asia-Pacific dominates the aluminum extrusion market, supported by strong manufacturing ecosystems, high aluminum production capacity, and robust demand from construction, automotive, and consumer goods sectors. Countries such as China and India lead regional consumption, driven by rapid urbanization, infrastructure investments, and expanding industrial activity, positioning the region as the primary growth engine for the global aluminum extrusion market.

Strategic Activities Within the Aluminum Extrusion Market

Drivers: Rising Demand for Lightweight and High-Strength Materials in Automotive and Construction

One of the primary drivers of the aluminum extrusion market is the increasing demand for lightweight and durable materials across automotive and construction industries. Aluminum extrusions provide an excellent strength-to-weight ratio, corrosion resistance, and design flexibility, making them ideal for structural and architectural applications. In the automotive sector, lightweight extruded components help improve fuel efficiency and extend the driving range of electric vehicles by reducing overall vehicle weight. Similarly, the construction industry widely uses aluminum extrusions in window frames, curtain walls, and structural systems due to their durability and ease of fabrication. Major industry players such as Norsk Hydro ASA, Alcoa Corporation, and Hindalco Industries Ltd. are expanding their extrusion and alloy development capabilities to support growing demand from these sectors

Opportunities: Expansion of Sustainable and Recycled Aluminum Solutions

A major opportunity in the aluminum extrusion market lies in the growing adoption of recycled aluminum and low-carbon production processes. Aluminum is highly recyclable, and recycled aluminum requires up to 95% less energy compared to primary aluminum production, making it an attractive solution for industries seeking to reduce carbon footprints. Increasing environmental regulations and corporate sustainability commitments are encouraging manufacturers to incorporate higher recycled content in extruded products. Companies such as Constellium and Norsk Hydro ASA are investing in closed-loop recycling systems and low-carbon aluminum production to meet growing demand for sustainable materials across automotive, construction, and packaging industries.

Challenges: Volatility in Aluminum Prices and Energy-Intensive Production

One of the key challenges facing the aluminum extrusion market is the volatility in aluminum prices and the high energy consumption associated with primary aluminum production. Aluminum prices are strongly influenced by fluctuations in energy costs, raw material availability, and global supply-demand dynamics. Since energy accounts for a significant portion of aluminum production costs, rising electricity prices can significantly impact manufacturing margins for extrusion companies. In addition, geopolitical factors and supply chain disruptions can affect the availability of primary aluminum and billets, creating pricing uncertainty. As a result, extrusion manufacturers are increasingly focusing on recycling, long-term supply agreements, and operational efficiency to manage cost pressures and maintain competitiveness.

The global aluminum extrusion market is witnessing steady growth as industries increasingly demand lightweight, durable, and high-performance materials across construction, automotive, electrical, and industrial applications. Aluminum extrusions offer excellent strength-to-weight ratio, corrosion resistance, and design flexibility, making them a preferred choice for structural and functional components. The market is driven by rising infrastructure development, growing adoption of electric vehicles, and increasing emphasis on energy efficiency and sustainable materials.

Aluminum extrusion products include a wide range of profiles such as rods, bars, tubes, and complex custom shapes used in diverse end-use industries. Continuous advancements in alloy development, precision extrusion, and surface finishing technologies are enabling manufacturers to produce high-quality, application-specific profiles at scale. Leading companies such as Norsk Hydro ASA, Alcoa Corporation, and Hindalco Industries Ltd. are investing in capacity expansion, downstream integration, and sustainable production to meet growing global demand.

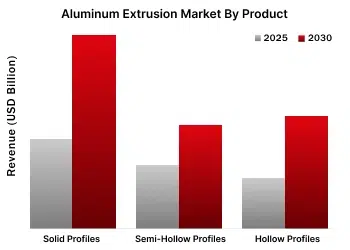

Solid Profiles segment dominated aluminum extrusion market by products in 2025

The solid profiles segment dominated the aluminum extrusion market by product in 2025, accounting for ~53% of total market share in 2024, indicating its continued leadership due to strong demand across core industries. Solid profiles such as rods, bars, beams, and channels are widely used in construction, infrastructure, and industrial applications because they offer higher structural strength (no internal cavities) and superior load-bearing capacity. Additionally, they are manufactured using simpler solid dies, making production faster and more cost-efficient compared to hollow and semi-hollow profiles. Their extensive use in high-volume applications like building frameworks, transportation components, and machinery, combined with lower manufacturing complexity, has solidified their position as the largest product segment in the aluminum extrusion market.

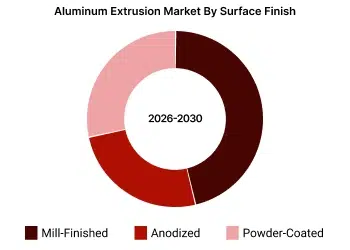

Mill-finished segment is expected to register the highest CAGR in the aluminum extrusion market by surface finish in the forecast period (2026-2030)

The mill-finished segment is expected to register the highest CAGR in the aluminum extrusion market during 2026–2030, driven by its cost efficiency and widespread industrial applicability. The segment is projected to grow at ~7.3–7.8% CAGR, supported by increasing demand from construction, industrial machinery, and solar mounting systems . Unlike anodized or powder-coated products, mill-finished extrusions eliminate additional surface treatment costs, reducing processing expenses and enabling shorter lead times and faster deployment in high-volume applications. Additionally, over 48% of end users prefer mill-finished profiles for their flexibility in downstream customization and fabrication. This combination of low cost, scalability, and versatility across industries is driving its position as the fastest-growing surface finish segment.

Asia-pacific is estimated to register the highest CAGR in the aluminum extrusion market during the forecast period (2026–2030)

Asia-Pacific is estimated to register the highest CAGR in the aluminum extrusion market during the forecast period (2026–2030) due to its strong industrial base, rapid urbanization, and large-scale infrastructure investments. The region already dominates the global market, accounting for over 70–75% of total revenue share in 2024–2025, supported by extensive construction and manufacturing activities across China, India, Japan, and Southeast Asia . Growth momentum remains significantly higher than the global average. Driven by infrastructure expansion, EV adoption, and industrial manufacturing growth . Countries such as China and India are investing heavily in transport, smart cities, and renewable energy projects, while the region’s cost-competitive manufacturing ecosystem and availability of raw materials further accelerate demand for aluminum extrusions. This combination of high base demand and faster-than-global growth rates firmly positions Asia-Pacific as the fastest-growing regional market.

Sources: Secondary Research

“Automotive manufacturers are increasingly adopting aluminum extrusions to reduce vehicle weight and improve fuel efficiency, particularly in electric vehicles where lightweight structures directly enhance battery range.”

Vice President, Lightweight Materials Procurement, Automotive OEM (Europe)

“Construction and infrastructure projects are driving strong demand for customized aluminum profiles due to their durability, corrosion resistance, and ease of installation in modern building designs.”

Director, Project Materials Sourcing, International Construction Firm (Europe)

“Recycled aluminum is becoming a key focus area as customers demand lower carbon footprint materials, pushing extrusion companies to invest in closed-loop recycling and secondary aluminum sourcing.”

Head of Sustainability, Aluminum Extrusion Manufacturer (Asia-Pacific)

“Precision extrusion and advanced finishing capabilities are increasingly critical as industrial and electronics customers require tighter tolerances and high-performance surface treatments.”

Chief Technology Officer, Industrial Aluminum Solutions Provider (Europe)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

| Particulars |

Details |

| Particulars Report |

Aluminium Extrusion Market |

| Forecast Period |

2026-2030 |

| Format |

|

| Market Size (2025) |

USD 120 Billion |

| CAGR (2026-2030) |

7.2% |

| Number of Pages |

165 |

| Number of Tables |

153 |

| Number of Figures |

38 |

| Key Segments |

Aluminium Extrusion Market by Alloy Grade (6XXX, 1XXX, 5XXX, Other Grade) Aluminium Extrusion Market by Product (Solid Profiles, Semi-hollow Profiles, Hollow Profiles) Aluminium Extrusion Market by Surface Finish (Mill-finished, Anodized, Powder-coated) Aluminium Extrusion Market by End Users (Construction & Infrastructure, Automotive & Mass Transport, Electrical & Electronics, Machinery & Equipment, Other End Users) |

| Regions Covered |

|

| Key Players Covered (Majority Share Holders) |

Hindalco Industries Ltd. (India), Alcoa Corporation (US), Aluminium Corporation of China Limited (China), Rusal (Russia), Kaiser Aluminum (US), Century Aluminum Company (US), Constellium (France), Norsk Hydro ASA (Norway), Jindal Aluminum Limited (India), Hammerer Aluminum Industries (Austria), Alom Group (India), Banco Aluminum Private Limited (India), Maan Aluminium Limited (India), Shenzhen Oriental Turdo Ironwares Co., Ltd (China), ETEM (Greece). |

| Other Players |

Guangdong Zhenhan Special Light Alloy Co., Ltd (China), Albras (Brazil), YK Aluminium (China), Eleanor Industries Pvt. Ltd (India), Alupco (Saudi Arabia), Zahit Aluminyum (Turkey), Arconic (US), Hulamin (South Africa), Gulf Extrusion (United Arab Emirates), Benkam Alu Extrusions (Uzbekistan). |

The global market for aluminum extrusion market was valued at USD 120 billion in 2025.

The global aluminum extrusion market is anticipated to grow at an annual growth rate of 7.2% from 2026 to 2030 to reach USD 170 billion, by 2030.

Leading players within the aluminum extrusion market are Hindalco Industries Ltd. (India), Alcoa Corporation (US), Aluminium Corporation of China Limited (China), Rusal (Russia), Kaiser Aluminum (US) and Century Aluminum Company (US).

The aluminum extrusion market is moderately fragmented to moderately consolidated, with a mix of large global producers and numerous regional and local extrusion companies serving diverse end-use industries. Leading players such as Norsk Hydro ASA, Alcoa Corporation, Constellium, and Hindalco Industries Ltd. hold strong market positions due to their integrated operations, global manufacturing footprint, and advanced value-added product offerings.

At the same time, the market remains highly competitive at the regional level, with a large number of small and mid-sized extruders catering to construction, automotive, and industrial applications through customized profiles and cost-competitive production. Companies are increasingly focusing on capacity expansions, downstream integration, and acquisitions to strengthen their market presence and move toward higher-margin, value-added segments such as automotive lightweighting and precision industrial components.