Wissen Research analysed that the global Fuel Cell Technology market was valued at USD 5.5 billion in 2024 and is projected to reach USD 21 billion by 2030, expected to grow at a CAGR of 25% during the forecast period, 2025-2030.

Fuel cell technology market is driven by increasing worldwide focus on clean and sustainable energy solutions, spurred by strict environmental regulations and rising demand for zero-emission transportation and stationary power generation. The development in hydrogen production, storage, and infrastructure is making wider commercialization possible, especially in heavy-duty road transportation and industrial uses. Top automakers and energy firms are heavily investing in fuel cell efficiency improvement, durability, and cost-effectiveness, driving adoption across various sectors

Yet, difficulties like high upfront capital expenses, sparse hydrogen refueling station infrastructure, and supply chain complications continue to restrain swift market growth, needing policy cooperation and technological advancement.

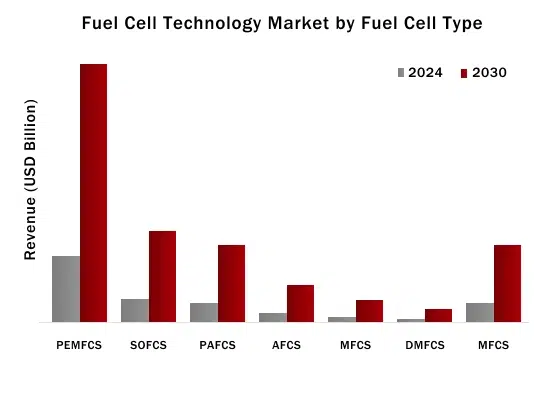

Proton Exchange Membrane Fuel Cell (PEMFC) segment has held the largest share in the market since 2022 till current and Solid Oxide Fuel Cell (SOFCS) is expected to show the highest growth during the forecast period, with Asia-pacific dominating the regional market share.

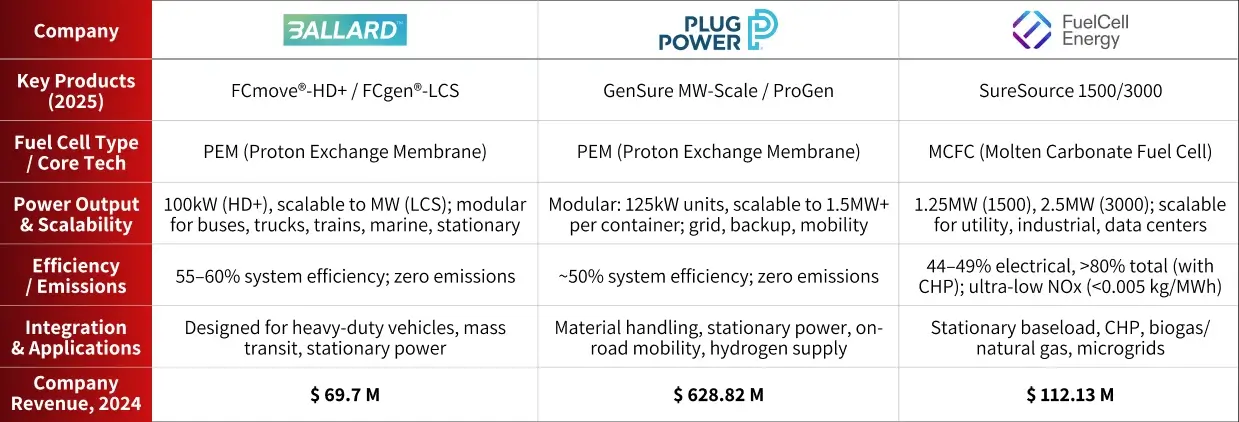

Key players functioning in global Fuel Cell technology sector are, Fuelcell Energy, Inc., Mitsubishi Heavy Industries, Ballard Power Systems, Hydrogenics Corporation, Plug Power, Inc., Doosan Fuel Cell America, Inc., Ceres Power Holdings PLC, Nuvera Fuel Cells LLC, Nedstack Fuel Cell Technology B.V., Kyocera Corporation, SFC Energy AG, Fuji Electric Co. Ltd., Cummins Inc., Toshiba Corporation, Aisin Corporation, Toyota Motor Corporation, among others.

Global Fuel Cell Technology market is anticipated to reach USD 21 billion by 2030 from USD 5.5 billion in 2024, growing at an annualized rate of 25% during the period 2025-2030. | The Asia-Pacific countries, dominated by Japan, South Korea, and China, are becoming the world center for fuel cell innovation and commercialization. Aggressive government campaigns, national hydrogen plans, and investment in fueling infrastructure are driving the deployment of fuel cell electric vehicles and stationary power applications, positioning Asia-Pacific as the fastest-growing fuel cell technology market globally. |

Asia-Pacific In Asia-Pacific, surging demand for clean mobility and resilient energy solutions is fueling rapid innovation in the fuel cell technology market. Aggressive national hydrogen strategies in countries like Japan, South Korea, and China are driving large-scale investments in hydrogen production, fueling infrastructure, and localized supply chains. |

The market for fuel cell technology is facing considerable change as technologies in hydrogen manufacturing and storage, as well as stack efficiency and longevity, improve to make wider use possible in heavy-duty transportation, distributed power, and industrial energy. Large-scale fuel cell truck, bus, and backup power systems deployment are being driven by this change, especially in countries with strong policy alignment with decarbonization. | Global investment in hydrogen ecosystems including electrolyser manufacturing, green hydrogen production, and refuelling networks is catalysing the expansion of fuel cell applications beyond transportation, into marine, rail, and off-grid power. For example, Hyundai’s deployment of fuel cell trucks in Switzerland and Japan’s hydrogen-powered residential microgrids highlight the technology’s expanding role in both mobility and stationary energy markets. The direction of the market is determined by changing regulatory landscapes, supply chain disruptions in key materials such as platinum and rare earths, and the demand for standardization in hydrogen quality and safety. In the meantime, public-private collaboration and transnational cooperation are proving critical to pushing through infrastructure hurdles and scaling up fuel cell use across different geographies and sectors. |

Drivers: Hydrogen Initiatives and Industrial Take-Up Drive Market Growth

Strong policy support, national hydrogen plans, and public-private collaboration in Asia-Pacific are driving fast growth of fuel cell technology, especially in transport, industry, and home applications. The intersection of strict emissions standards, high investments in hydrogen infrastructure, and operational requirements for clean, efficient power is propelling mass use of fuel cell cars, stationary power solutions, and backup power products.

Opportunities: Asia-Pacific Hydrogen Ecosystem Opens New Frontiers for Fuel Cell Innovation

Rapid rollouts of hydrogen refueling infrastructure, scaling up green hydrogen production, and increased cooperation between automakers, utilities, and technology companies are creating fertile ground for innovation. The region’s leadership in PEMFC and SOFC technologies, coupled with booming demand for clean energy in urban mobility, logistics, and heavy industry, presents considerable growth opportunities for both incumbents and new startups.

Challenges: High Initial Investment Needs and Infrastructural Gaps Restrict Mass Adoption

In spite of robust policy backing, the fuel cell technology market continues to be thwarted by ongoing issues of high up-front investment needs, bounded hydrogen refueling infrastructure, and supply chain complications for key materials. Regulatory ambiguities, technology standardization challenges, and skilled labor needs add to the risk and complexity for market players, especially in scaling up deployments past pilot and demonstration levels.

The worldwide fuel cell technology market, including proton exchange membrane, solid oxide, and others, is experiencing strong growth driven by the imperative for green energy solutions, strict emission policies, and rapidly growing adoption in transportation, industrial, and stationary power applications. Worth about USD 6.9 billion in 2025, the market is expected to reach close to USD 21 billion by 2030, posting an astounding CAGR of more than 25%. Principal growth promoters are growing government incentives, high growth in hydrogen infrastructure, and constant innovation in the efficiency and longevity of fuel cells. Asia Pacific dominates the market, driven by ambitious national hydrogen strategies and bulk deployment in China, Japan, and South Korea, supported by North America and Europe as key hubs for research, commercialization, and policy support. Transition to zero-emission vehicles, distributed power generation, and resilient off-grid applications is likely to drive further growth in the global market in the next decade

Proton exchange membrane fuel cell (PEMFC) segment dominated the Fuel Cell Technology Market by Fuel Cell Type in 2024

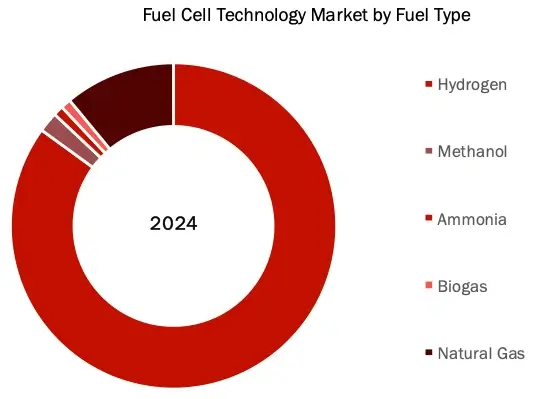

Hydrogen Fuel Segment held the largest market share in 2024, accounting for a significant share in Fuel Cell Technology market by Fuel Type

Asia-Pacific held the largest market share in Fuel Cell Technology Market in the forecast period (2025-2030)

Asia-Pacific held the largest market share in the fuel cell technology market during the forecast period (2025–2030), propelled by robust government policies, large-scale investments in hydrogen infrastructure, and strong demand for clean transportation solutions. Countries such as Japan, South Korea, and China are leading this growth through aggressive national hydrogen strategies, generous subsidies for fuel cell vehicles, and rapid expansion of hydrogen refueling networks. For example, in 2024, Toyota and Hyundai-Kia accelerated the rollout of fuel cell electric vehicles and buses across the region, while China expanded its fleet of hydrogen-powered commercial vehicles and invested heavily in hydrogen corridors for long-distance logistics. These initiatives, combined with a focus on green hydrogen production and public-private partnerships, are positioning Asia-Pacific as the global hub for fuel cell innovation and large-scale deployment.

Major players operating in Fuel Cell Technology market are:

Note: The aforementioned revenues are annual company revenues collected from company reports and sec filings

Sources: Secondary Research

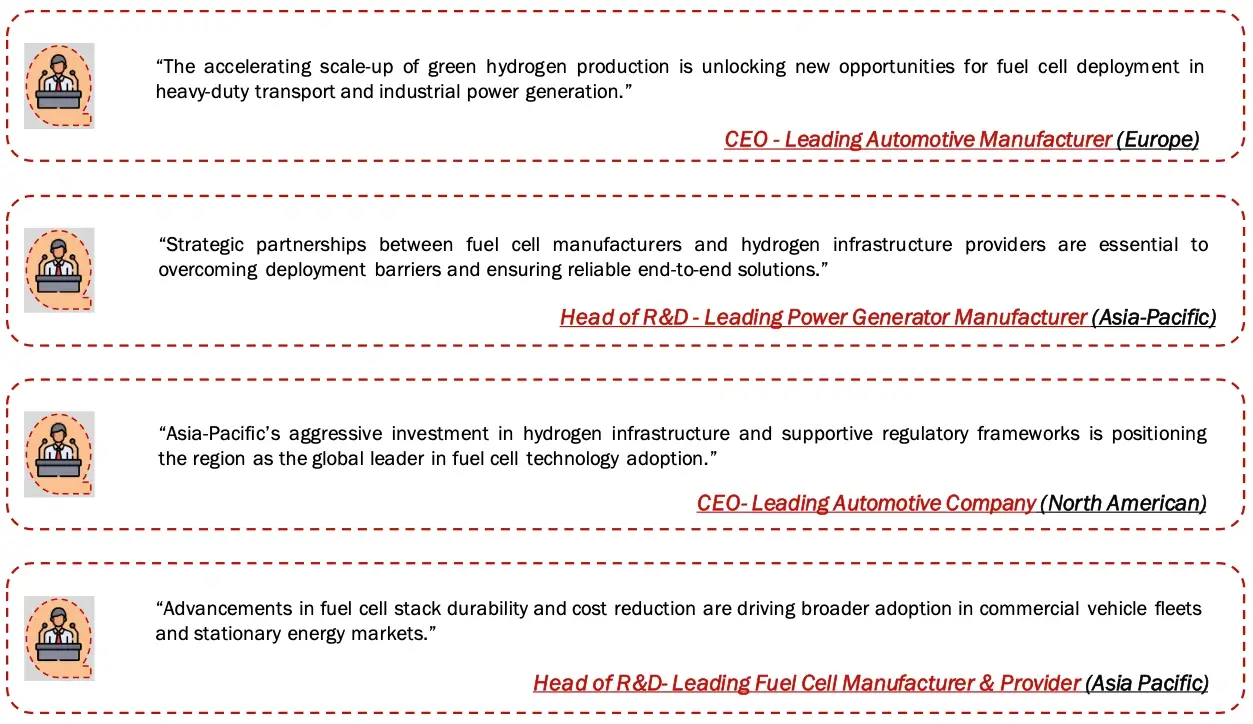

PRIMARY INSIGHTS FROM KEY OPINION LEADERS

Particulars | Details |

| Report | Fuel Cell Technology Market |

| Forecast Period | 2025-2030 |

| Base Year | 2024 |

| Format | |

| Market Size (2024) | USD 5.5 Billion |

| CAGR (2025-2030) | 25% |

| Number of Pages | 165 |

| Number of Tables | 155 |

| Number of Figures | 34 |

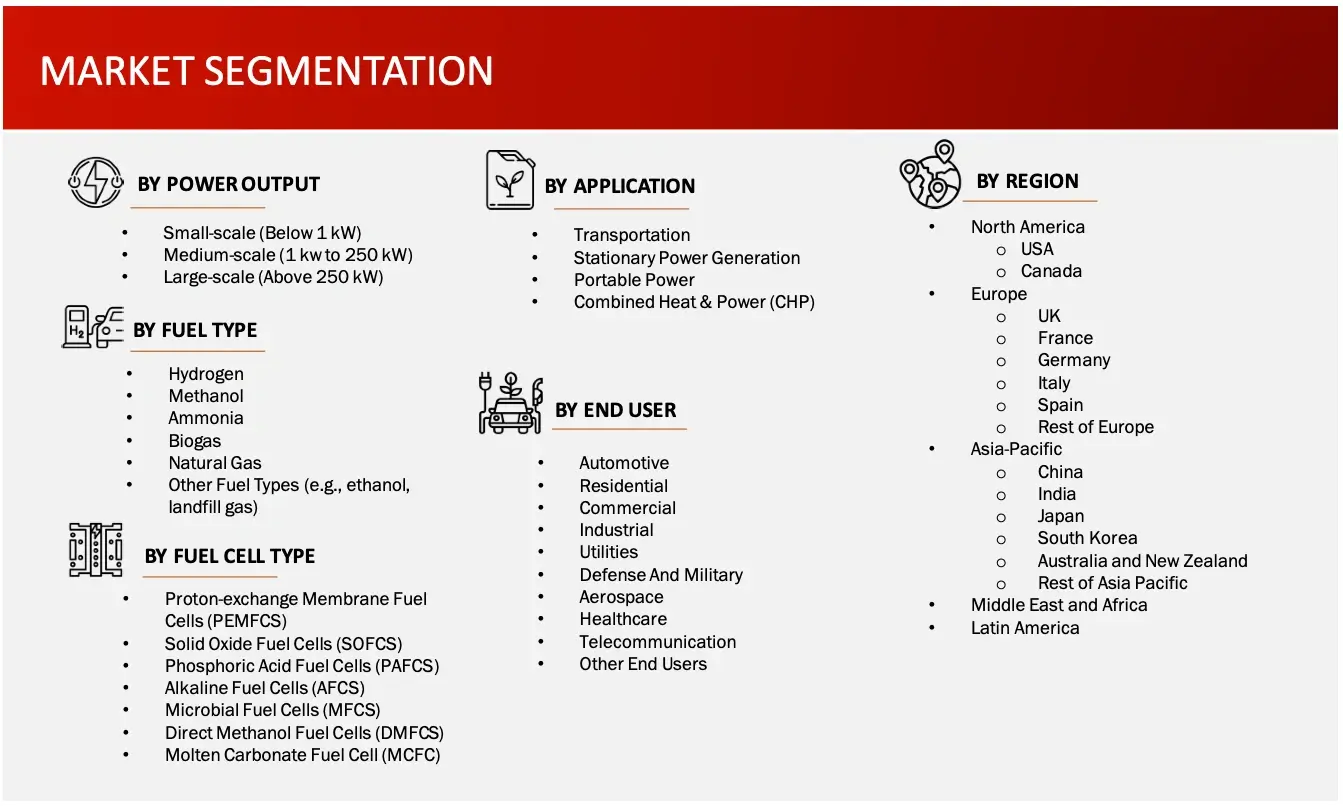

| Key Segments | Fuel Cell Technology Market Power Output Outlook (Small-scale (Below 1 kW), Medium-scale (1 kw to 250 kW), Large-scale (Above 250 kW)) Fuel Cell Technology Market Fuel Type Outlook (Hydrogen, Methanol, Ammonia, Biogas,Natural Gas, Other Fuel Types) Other Fuel types include ethanol, landfill gas, etc. Fuel Cell Technology Market Fuel Cell Type Outlook (Proton-exchange Membrane Fuel Cells (PEMFCS), Solid Oxide Fuel Cells (SOFCS), Phosphoric Acid Fuel Cells (PAFCS), Fuel Cell Technology Market Application Outlook (Transportation, Stationary Power Generation, Portable Power, Combined Heat & Power (CHP)) Fuel Cell Technology Market End User Industry Outlook (Automotive, Residential, Commercial, Industrial, Utilities, Defence and Military, Aerospace, Healthcare, Telecommunication) |

| Regions Covered | § North America: US and Canada § Europe: Germany, UK, France, Italy, Spain, and Rest of the Europe §Asia-Pacific: China, Japan, India, South Korea, Australia and New Zealand, and Rest of the Asia-Pacific § Latin America § Middle East and Africa |

| Key Players Covered (Majority Share Holders) | Fuelcell Energy, Inc. (US), Mitsubishi Heavy Industries (Japan), Ballard Power Systems (Canada), Plug Power, Inc. (US), Doosan Fuel Cell America, Inc. (US), Ceres Power Holdings PLC (UK), Nuvera Fuel Cells LLC (US), Nedstack Fuel Cell Technology B.V. (Netherlands), Kyocera Corporation (Japan), SFC Energy AG (Germany), Fuji Electric Co. Ltd. (Japan), Cummins Inc. (US), Toshiba Corporation (Japan), Aisin Corporation (Japan), Toyota Motor Corporation (Japan) |

| Other Players | Ten Intelligent Energy Limited (UK), Horizon Fuel Cell Technologies PTE LTD (Singapore), Nuvera Fuel Cells, LLC (US), Solidpower S.P.A. (Italy), Altergy (US), Adaptive Energy (US), Adelan (UK), Special Power Sources (US), Ztek Corporation, Inc. (US), Microrganic Technologies (US), Avl List GMBH (Austria), Watt Fuel Cell Corporation (US), Proton Motor Fuel Cell GMBH (Germany) |

Introduction

Market Definition

The market for fuel cell technology consists of equipment and systems that produce electricity by means of electrochemical processes, mainly hydrogen or other fuels, to provide clean, efficient, and dependable power with low environmental impact. The market involves various types of fuel cells—proton exchange membrane fuel cells (PEMFC), solid oxide fuel cells (SOFC), and alkaline fuel cells—deployed in transportation (fuel cell vehicles), stationary power generation, and portable power uses. Spurred by worldwide demand for clean energy, tough emissions regulations, and enormous investments in hydrogen infrastructure, fuel cell technology is gaining increasing acceptance in commercial, industrial, and public applications to lower greenhouse gas emissions and enable transition to low-carbon energy systems.

Sources: Company Websites and Wissen Research Analysis

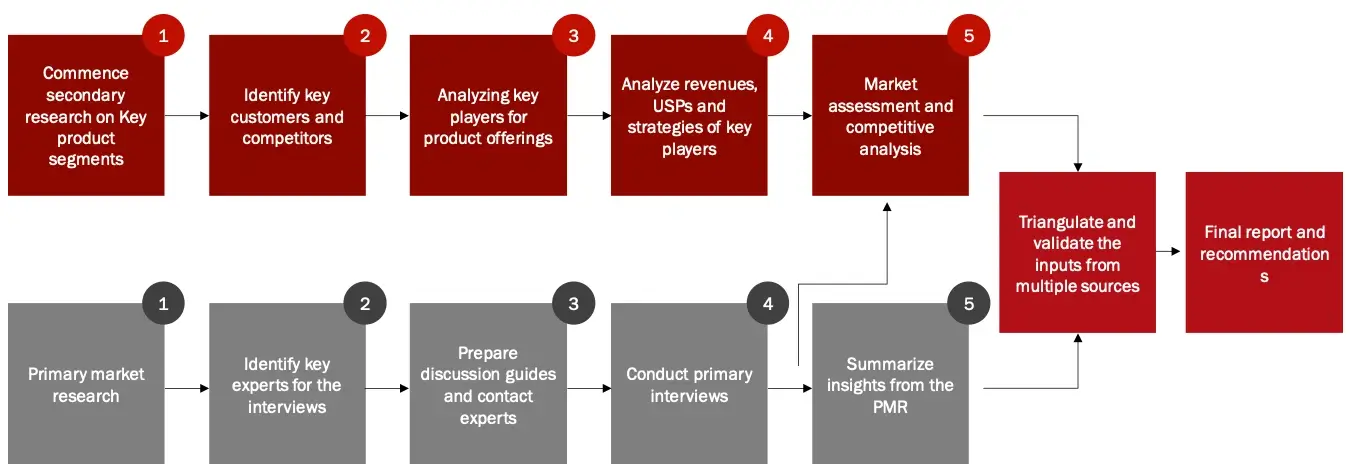

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the fuel cell technology market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub-segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the fuel cell technology market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the fuel cell technology market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major manufacturers offering various fuel cell technology will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of fuel cell technology market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub-segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the fuel cell technology market.

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. FUEL CELL TECHNOLOGY: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. NEED GAP ANALYSIS

4.5. KEY CONFERENCES

4.6. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.7. INDUSTRY TRENDS

4.8. PORTER’S FIVE FORCES ANALYSIS

4.9. REGULATORY LANDSCAPE

4.9.1.NORTH AMERICA

4.9.2.EUROPE

4.9.3.ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. GLOBAL FUEL CELL TECHNOLOGY MARKET BY, POWER OUTPUT (2025-2030, USD MILLION)

6.1. SMALL-SCALE (BELOW 1 kW)

6.2. MEDIUM-SCALE (1KW TO 250 kW)

6.3. LARGE- SCALE (ABOVE 250 kW)

7. GLOBAL FUEL CELL TECHNOLOGY MARKET BY, FUEL TYPE (2025-2030, USD MILLION)

7.1. HYDROGEN

7.2. METHANOL

7.3. AMMONIA

7.4. BIOGAS

7.5. NATURAL GAS

7.6. OTHER FUEL TYPES (e.g., ethanol, landfill gas)

8. GLOBAL FUEL CELL TECHNOLOGY MARKET BY, FUEL CELL TYPE (2025-2030, USD MILLION)

8.1. PROTON-EXCHANGE MEMBRANE FUEL CELLS (PEMFCS)

8.2. SOLID OXIDE FUEL CELLS (SOFCS)

8.3. PHOSPHORIC ACID FUEL CELLS (PAFCS)

8.4. ALKALINE FUEL CELLS (AFCS)

8.5. MICROBIAL FUEL CELLS (MFCS)

8.6. DIRECT METHANOL FUEL CELLS (DMFCS)

8.7. MOLTEN CARBONATE FUEL CELL (MCFC)

8.8. OTHER TYPES

9. GLOBAL FUEL CELL TECHNOLOGY MARKET BY, APPLICATION (2025-2030, USD MILLION)

9.1. TRANSPORTATION

9.2. STATIONARY POWER GENERATION

9.3. PORTABLE POWER

9.4. COMBINED HEAT & POWER (CHP)

10. GLOBAL FUEL CELL TECHNOLOGY MARKET BY, END USERS (2025-2030, USD MILLION)

10.1. AUTOMOTIVE

10.2. RESIDENTIAL

10.3. COMMERCIAL

10.4. INDUSTRIAL

10.5. UTILITIES

10.6. DEFENSE AND MILITARY

10.7. AEROSPACE

10.8. HEALTHCARE

10.9. TELECOMMUNICATION

10.10. OTHER END USERS

11. GLOBAL FUEL CELL TECHNOLOGY MARKET BY, REGION (2025-2030, USD MILLION)

11.1. NORTH AMERICA

11.1.1. US

11.1.2. CANADA

11.2. EUROPE

11.2.1. GERMANY

11.2.2. FRANCE

11.2.3. SPAIN

11.2.4. ITALY

11.2.5. UK

11.2.6. REST OF THE EUROPE

11.3. ASIA-PACIFIC

11.3.1. CHINA

11.3.2. JAPAN

11.3.3. INDIA

11.3.4. AUSTRALIA AND NEW ZEALAND

11.3.5. SOUTH KOREA

11.3.6. REST OF THE ASIA-PACIFIC

11.4. MIDDLE EAST AND AFRICA

11.5. LATIN AMERICA

12. COMPETITIVE ANALYSIS

12.1. REVENUE ANALYSIS

12.2. KEY PLAYERS FOOTPRINT ANALYSIS

12.3. MARKET SHARE ANALYSIS (2023/2024)

12.4. REGIONAL SNAPSHOT OF KEY PLAYERS

12.5. R&D EXPENDITURE OF KEY PLAYERS

12.6. BRAND/ PRODUCT COMPARISON

13. COMPANY PROFILES

13.1. FUELCELL ENERGY, INC.

13.1.1. BUSINESS OVERVIEW

13.1.2. PRODUCT PORTFOLIO

13.1.3. FINANCIAL SNAPSHOT

13.1.4. RECENT DEVELOPMENTS

13.1.4.1. MERGER/ACQUISITIONS

13.1.4.2. PRODUCT APPROVAL/LAUNCHES

13.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

13.1.4.4. EXPANSIONS

13.2. MITSUBISHI HEAVY INDUSTRIES

13.3. BALLARD POWER SYSTEMS

13.4. HYDROGENICS CORPORATION

13.5. PLUG POWER, INC.

13.6. DOOSAN FUEL CELL AMERICA, INC.

13.7. CERES POWER HOLDINGS PLC

13.8. NUVERA FUEL CELLS LLC

13.9. NEDSTACK FUEL CELL TECHNOLOGY B.V.

13.10. KYOCERA CORPORATION

13.11. SFC ENERGY AG

13.12. FUJI ELECTRIC CO. LTD.

13.13. CUMMINS INC.

13.14. TOSHIBA CORPORATION

13.15. AISIN CORPORATION

13.16. TOYOTA MOTOR CORPORATION

13.17. OTHER PLAYERS

13.17.1. ΤΕΝ INTELLIGENT ENERGY LIMITED

13.17.2. HORIZON FUEL CELL TECHNOLOGIES PTE LTD

13.17.3. NUVERA FUEL CELLS, LLC

13.17.4. SOLIDPOWER S.P.A.

13.17.5. ALTERGY

13.17.6. ADAPTIVE ENERGY

13.17.7. ADELAN

13.17.8. SPECIAL POWER SOURCES

13.17.9. ZTEK CORPORATION, INC.

13.17.10. MICRORGANIC TECHNOLGIES

13.17.11. AVL LIST GMBH

13.17.12. WATT FUEL CELL CORPORATION

13.17.13. PROTON MOTOR FUEL CELL GMBH

14. APPENDIX

14.1. INDUSTRY SPEAK

14.2. QUESTIONNAIRE/DISCUSSION GUIDE

14.3. AVAILABLE CUSTOM WORK

14.4. ADJACENT STUDIES

14.5. AUTHORS

15. REFERENCES