Point of Care Diagnostic Market

Global Industry analysis, Size, Share, Growth, Trends, and Forecast 2026-2031

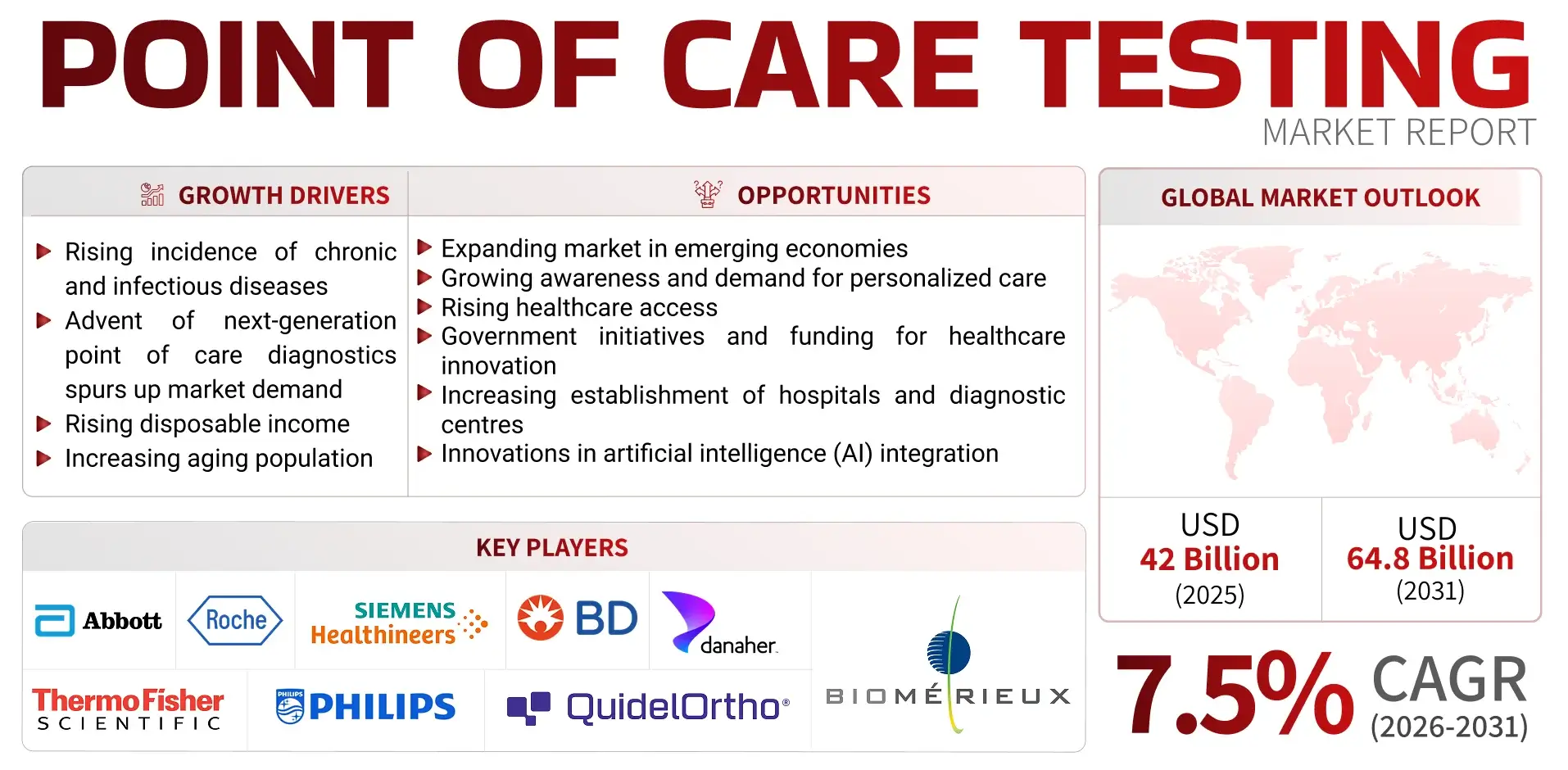

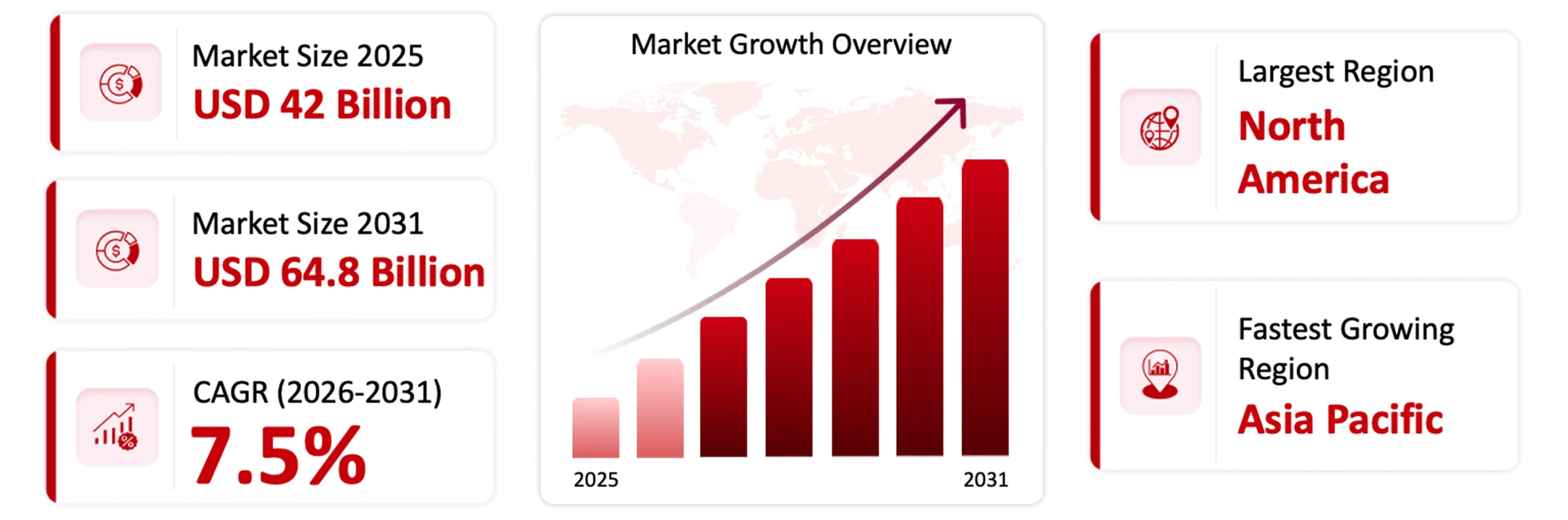

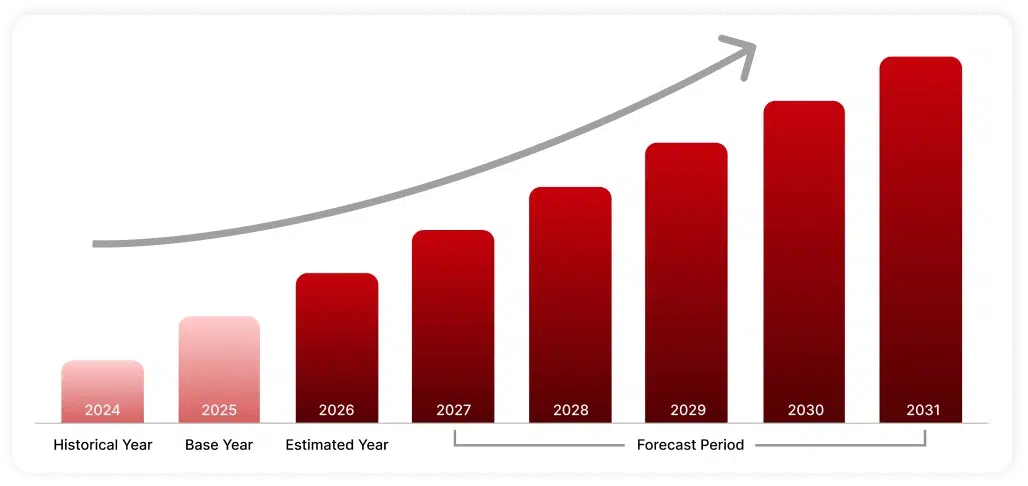

The global point of care diagnostic market is projected to reach USD 64.8 billion by 2031, growing at a CAGR of 7.5% during the forecast period.

| Market Size 2026 | Market Size 2031 | CAGR (2026-2031) | Largest Region | Fastest Growing Region |

|---|---|---|---|---|

| USD 45.1 billion | USD 64.8 billion | 7.5% | North America | Asia Pacific |

Market Overview

The global point-of-care diagnostic (POCD) market is expanding rapidly. This surge is attributed to the growing need for faster and distributed diagnostic approaches, constant improvement in biosensor and microfluidic technologies, increased use of POCD in conjunction with digital healthcare systems and telemedicine solutions, and greater application in clinical diagnostics, infectious disease surveillance and monitoring, chronic disease care, and home-based care. The market is estimated at at USD 45.1 billion in 2026 and is projected to reach USD 64.8 billion by 2031, growing at a CAGR of 7.5% during the forecast period (2026-2031).

Technology Overview

With continued improvements in biosensors, microfluidics and lab-on-chip technology, POCD devices can provide doctors with quick, accurate and immediate test results using very small amounts of sample. The demand for decentralized healthcare along with fast clinical decision-making has led to an increase in the number of single parameter tests to multi-parameter tests integrated into one platform; therefore, POCD products can now be capable of providing information for numerous things (e.g., infected patients, chronic disease patients, patients in an emergency situation). POCD products will be able to increase their ability to communicate with digital health systems as well as smartphones; this means that data can be transferred, monitored and managed from anywhere at any time, allowing for better workflow processes between doctors and patients through seamless integration.

Key Growth Drivers

- One of the most powerful and persistent market drivers since COVID-19 has been the shift away from centralized and towards more decentralized and faster diagnostic testing. The ever-increasing amount of infectious diseases and chronic diseases will be one of the key long-term demand drivers for point-of-care (POCT).

- The continued development of technology around point-of-care diagnostics (such as biosensors, microfluidics and handheld analyzers) will continue to be a key factor in improving the accuracy and usability of tests.

- As digital health continues to develop and telehealth continues to become more prevalent, the relationship between these technologies and the core drivers of demand for point-of-care testing will continue to evolve, although they will take on a smaller role in comparison to the core drivers of demand for testing.

- The growth of home-based and self-testing is currently a major trend in developed markets as well as in many developing markets.

- Government support and regulation from various countries can also be substantive demand drivers for point-of-care diagnostic especially for infectious disease testing.

Point of Care Diagnostic Market Key Highlights

Need deeper insights on this market?

Get full report access with detailed forecasts, competitive analysis, and segmentation.

Point of Care Diagnostic Market Trends

With increased demands for quick diagnostic procedures, decentralized provision of healthcare services, and real-time decision making in the clinical setting, there have been increased investments in the area of point-of-care diagnostics (POCD). The introduction of new trends in the industry will have a positive impact on the POCD market by creating more opportunities in areas such as home testing, digital health platform integration, multiplex and molecular diagnostics, and the use of portable and connected devices. It is therefore anticipated that key players in the POCD market such as Abbott Laboratories, F. Hoffmann-La Roche, Danaher Corporation, and Siemens Healthineers AG will continue developing POCD products such as handheld analyzers, fast antigen, and molecular test kits as well as integrated data platforms.

Point of Care Diagnostic Industry Trends- Miniaturization and Lab-on-a-Chip

Lab-on-a-chip and miniaturization technologies are revolutionizing point-of-care diagnostics. Compact, low-cost and efficient diagnostic devices are now being developed. Microfluidics and integrated biosensors are enabling multiple lab functions, such as preparation, processing, and analysis, to be performed on one lab-on-a-chip, resulting in quicker turnarounds and decreased amount of required sample. While initially only useful for rapid tests, lab-on-a-chip is now being used for more complex testing applications, including molecular diagnostics and multiple tests for multiple markers. Increased demand for portable and home-based testing is also increasing the use of lab-on-a-chip. Leading companies like Abbott, F. Hoffmann-Le Roche and Danaher are working to improve the portability, accuracy and usability of lab-on-a-chip systems through their investment in miniaturized platforms, making lab-on-a-chip systems a key element in developing next-generation point-of-care diagnostics.

Asia Pacific Point of Care Diagnostics Market Trends Insights

Reasons contributing to the increase in demand for the Asia Pacific point of care diagnostics market are improvements to the health infrastructure across the region, growth in the number of people, and the increasing demand for affordable and quick diagnostic services. The leading countries in terms of growth of the Asia Pacific point of care diagnostics market are China, India, Japan and South Korea. These countries are experiencing rapid growth due to the following: increased awareness of the benefits of early detection for disease; high incidence rates of diseases (both chronic and infectious); government initiatives aimed to enhance primary healthcare and the diagnosis of diseases in rural areas. Additionally, increased acceptance of decentralized healthcare systems and home-based diagnosis has provided further growth potential to the point of care diagnostics market. Major companies involved in the point of care diagnostics market include Abbott Laboratories, F. Hoffmann-La Roche, and Sysmex Corporation.

Key Players in the Point of Care Diagnostics Market

Leading companies in the point of care diagnostics market are focusing on innovation, strategic partnerships, and expansion of health-centric features to strengthen their market position.

Strategic Activities within Point of Care Diagnostics Market

QuidelOrtho Corporation completed the acquisition of LEX Diagnostics for cash consideration of approximately $100 million. The LEX VELO System received U.S. Food and Drug Administration (“FDA”) 510(k) clearance and CLIA waiver in February 2026. The LEX VELO System is a breakthrough molecular diagnostics platform that is designed to deliver highly sensitive, multiplex RT-PCR testing for Influenza A, Influenza B and COVID-19 directly from a swab sample in approximately six to ten minutes.

Abbott Laboratories and Flatiron Health, a leading healthtech company advancing point-of-care solutions in oncology, announced the integration of Abbott’s comprehensive Precision Oncology portfolio into OncoEMR®, Flatiron’s cloud-based Electronic Medical Record (EMR) platform.

Royal Philips announced the global launch of the Flash Ultrasound System 5100 POC a breakthrough point-of-care (POC) ultrasound system engineered for the fast-moving needs of anesthesia, critical care, emergency medicine, and musculoskeletal imaging.

Biocare Inc. signed a collaboration agreement with Abbott to bring the Afinion™ 2 Analyzer to more clinicians across the country. This advanced diagnostic platform delivers real-time HbA1c, ACR, CRP, and Lipid panel results that empower healthcare professionals to make swift, data-driven decisions that enhance patient outcomes.

Point of Care Diagnostics Market Insights

Demand for faster clinical decisions and quicker patient diagnoses are propelling growth in the Point-of-Care diagnostics (POCD) marketplace. The growth of healthcare facilities towards being more patient-oriented and outpatient oriented is contributing to the increase of near patient testing as a means to augment traditional laboratory testing. Timeliness of diagnosis, decreased pressure on hospitals and the ability to use test results in an effective manner for timely treatment are reasons why POCD are now an integral part of the modern health system.

Across settings such as infectious disease detection, chronic disease management, and emergency care, point of care diagnostics (POCD) is becoming increasingly common. Many types of POCT (e.g., blood glucose testing, cardiac marker testing, rapid antigen testing) are helping to improve patient outcomes. With the home-based diagnostics growth and self testing solutions for continuous or frequent monitoring of a patient’s condition, POCD is expected to continue to grow.

The rising instances of infections and chronic conditions, along with growing rapid diagnostic testing demand and a shift towards decentralized medicine, will drive the POCD market growth. Owing to technological innovations in sectors like microfluidics, biosensors, and portable analyzers, higher precision and productivity are possible in test protocols. Last but not least, the combination of telemedicine and digital health applications enable instant information exchange and remote medical decision-making, thus providing more adoption prospects via this approach.

POCDs are being driven by trends such as miniaturization, laboratory-on-chip technology, and creation of diagnostic platforms for multiple biomarkers to be detected simultaneously. Advancements in connectivity with mobile phone devices and the health care system will increase access and ease of managing data. Issues that could limit their use are variable test accuracy and complexity with regulation and standardization across the devices.

It is predicted that the Asia Pacific will record the highest growth rate in the point-of-care diagnostics market owing to the growing infrastructure for healthcare, large patient base, and awareness on the benefits of early diagnosis. Countries like China, India, Japan, and South Korea are among the main drivers for the growth in the region, backed by the efforts made by the governments to improve primary healthcare facilities in the rural settings.

Point of Care Diagnostics Market Dynamics

Drivers: Rising demand for rapid diagnostic services is fueling the adoption of POCD systems.

The rising number of patients suffering from infectious diseases coupled with the need for timely treatment is creating a demand for POCD systems. Healthcare providers are shifting towards using POCD systems to make faster diagnoses in emergency care, primary care clinics, and faraway locations. In addition, the increased experience during previous global health emergencies has led to an appreciation of the need for rapid diagnosis, and hence continued investments in rapid antigen, molecular, and multiplex POCD technologies are expected.

Opportunities: Growth opportunities abound within at-home and self-testing diagnostics.

With the increased use of home health services, there are huge opportunities in the POCD market. Consumers are embracing the use of convenient diagnostic tests as part of health screening activities to monitor any chronic conditions as well as detect diseases as early as possible. The development of digital connectivity through smartphones, among other advances, is creating new growth opportunities by making POCD more accessible and easier for consumers to use.

Challenges: Limited Reimbursement Policies in Point of Care Diagnostics Industry

Limited policies regarding reimbursements limit growth in the POCD market in the US. In fact, there is inconsistency in reimbursement rates that differ among insurance plans. Coverage decisions of certain POCDs are made on an individual basis, leaving room for inconsistency. To be considered for reimbursement, a POCD should prove its usefulness and therefore be able to provide a benefit to the patient. Expensive POCDs valued at more than $500 must provide strong evidence in order to gain coverage (Sources: American Medical Association, National Academy of Clinical Biochemistry). The reimbursement process itself is hampered by problems regarding coding. POCDs listed under the CPT Category III code are usually not reviewed automatically and hence subject to long waiting times or even denials (Source: American Medical Association). Less costly POCDs (less than $50) do not usually undergo evaluation by health plans for coverage (Source: Centers for Medicare & Medicaid Services). Community pharmacies encounter obstacles because they have to be certified and enrolled as independent clinical laboratories in order to bill Medicare payments.

Technology and Market Insights

There have been many developments in the global point-of-care diagnostics (POCD) market, as seen through the growth that continues to be experienced. This is due to the increasing demand for POCD devices that are capable of delivering quick, reliable, and decentralized diagnoses. Point-of-care test devices make use of advances made in technology such as biosensors and microfluidic devices to offer rapid test results on-site or even close to the patients. Other drivers that are promoting the growth of this market include the increase in the incidence of both infectious and non-infectious diseases, use of telehealth and home care services, and more efficient molecular diagnostics tests.

Technology Scope and Products

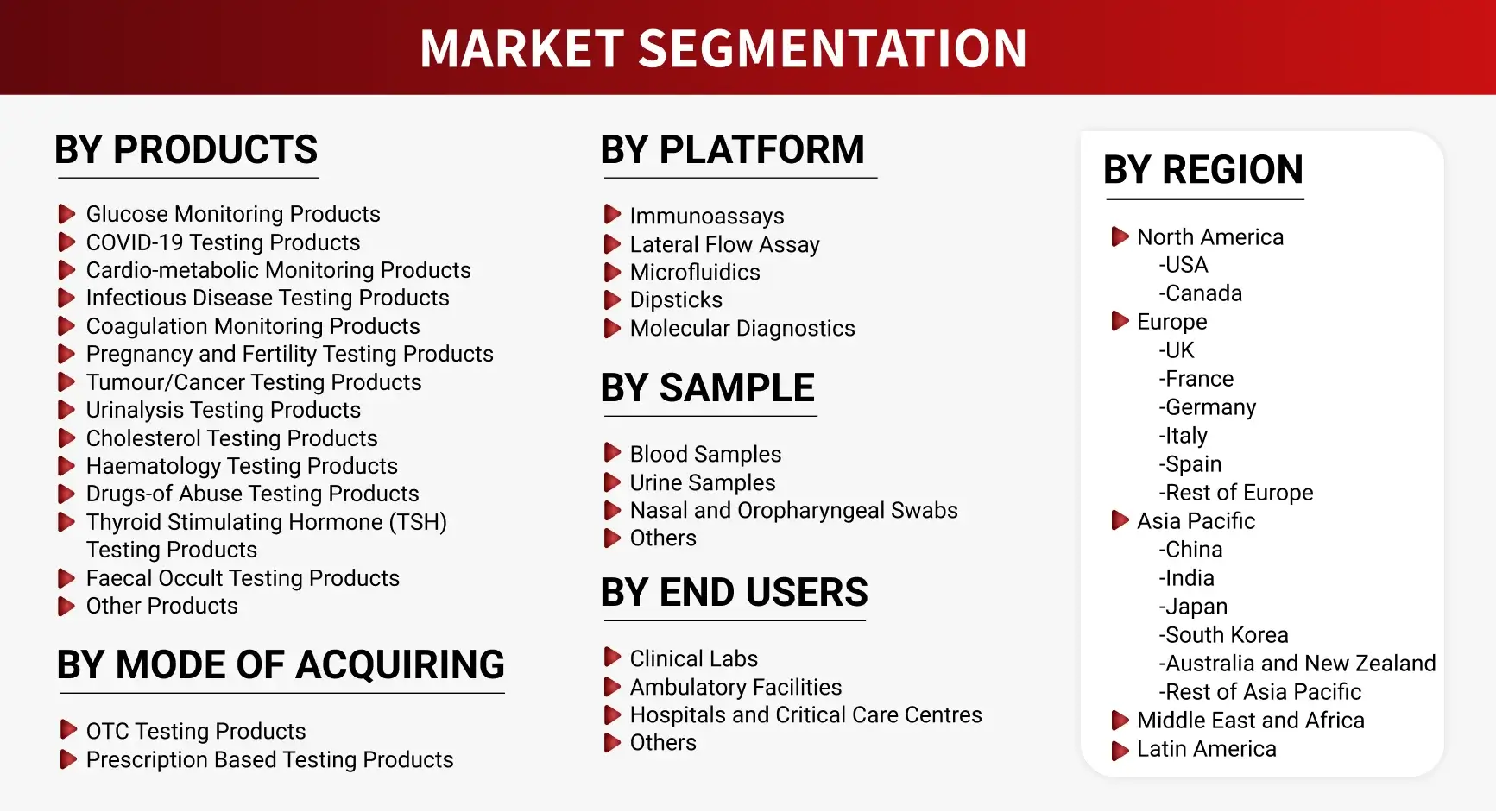

Point of Care Diagnostics detailed Market Segmentation

Want detailed insights from this report?

Industry Developments and Competitive Landscape

The market for point-of-care diagnostics (POCD) technology is experiencing rapid change due to improvements in molecular diagnostics, microfluidics and biosensors. Major manufacturers such as Abbott Laboratories, F. Hoffmann-La Roche, Siemens Healthineers AG, and Danaher Corporation are investing in developing next-generation products such as handheld analyzers, multiplex diagnostic systems and molecular tests. Many are looking to expand their product lines through acquisitions, partnerships, and by entering into new geographic regions, especially in emerging markets. In addition to this increased focus on expanding product lines, the growing integration of digital health technology and connectivity capabilities will support real time data sharing and facilitate clinical decision making by increasing competition and driving ongoing innovation in the POCD market.

The point of care diagnostic market is divided into multiple product categories. In 2025, the Glucose Monitoring segment accounted for the largest share of the global market.

-

Several factors contributed to the segment’s leading position. The continuously rising prevalence of diabetes and prediabetes worldwide has significantly increased demand for rapid and convenient blood glucose monitoring solutions across hospitals, clinics, and home-care settings. Major manufacturers such as Abbott, Dexcom, Medtronic, and Roche have strengthened the market through continuous innovation in glucose monitoring technologies, including connected glucose meters and continuous glucose monitoring (CGM) systems.

-

Technological advancements have further accelerated segment growth. Modern glucose monitoring devices offer improved accuracy, real-time data transmission, smartphone connectivity, cloud-based patient management, and integration with insulin delivery systems. The increasing adoption of CGM devices, particularly among patients with Type 1 and insulin-dependent Type 2 diabetes, has expanded the scope of point-of-care glucose testing beyond traditional finger-prick methods.

-

Additionally, growing awareness of diabetes management, expanding reimbursement coverage for glucose monitoring devices, and increasing healthcare expenditure in emerging economies continue to support market expansion. The shift toward preventive healthcare, remote patient monitoring, and personalized disease management is expected to further strengthen demand for point-of-care glucose monitoring solutions over the coming years.

From 2026 to 2031, the molecular diagnostic segment will be the fastest growing platform in the Point of Care (POC) Diagnostics market because of the high accuracy and sensitivity of molecular diagnosis and the ability to diagnose disease accurately and provide early diagnosis of disease using genomic and other molecular methods.

-

Unlike rapidly developed diagnostic tests that provide rapid turnaround at the point of delivery, molecular and other diagnostic methods such as polymerase chain reaction (PCR) and next-generation sequencing (NGS) enable clinicians to make accurate clinical decisions based on the results of various infectious diseases and oncological biomarkers and provide information on antimicrobial resistance. Increased demand for molecular diagnostics tools is being driven by an increasing shift towards near patient rapid laboratory quality diagnostic testing.

-

Molecular diagnostics is considered to be the fastest growing platform segment in the entire POC testing and diagnostic industry. As well, the increasing number of innovations in genomics and high demand for high accuracy diagnostic tests has certainly contributed to this trend partially through a greater number of people being infected with infectious diseases such as HIV. In 2024, it is estimated that approximately 40.8 million people will be living with HIV worldwide. Technological advancements in portable PCR devices, isothermal amplification techniques, and multiplex technology have substantially contributed to the increased acceptance of molecular POC devices.

Market analysis of point of care diagnostics included the in-depth assessment of five major regions, which include North America, Europe, Asia Pacific, MEA, and Latin America. The assessment of each region was done considering aspects related to health infrastructure, regulations, technology innovations, and market trends. North America emerged as the leader in terms of market shares for the point of care diagnostic market in 2025 due to an advanced health infrastructure, use of innovative imaging technologies, and active participation of market leaders such as Abbott laboratories, Siemens Healthineers, and Thermo-fischer scientific.

The leading position of North America in the POCD market in 2025 is because of advanced health infrastructure and early adoption of innovative POCD devices by companies such as Abbott, Roche, and Becton, Dickinson and Company with their product ranges including i-STAT®, cobas® Liat®, and continuous glucose monitoring system. Europe’s market share is supported by its strong healthcare policy framework and rise in home testing, whereas Asia Pacific’s market share presents huge growth opportunity due to increased investment in POC infrastructure.

What This Report Covers

This report provides a comprehensive analysis of the point of care diagnostics market, offering insights into key trends, growth drivers, challenges, and future opportunities. It is designed to support strategic decision-making through a combination of quantitative data and qualitative analysis.

Specifically, the report covers:

Market Overview & Definition: Overview of the market scope, structure, and key terminology.

Market Size & Forecast: Historical data and future projections across key segments and regions.

Key Market Trends: Insights into emerging trends, technological advancements, and evolving demand patterns.

Drivers, Restraints & Opportunities: Analysis of key factors influencing POCT market growth.

Competitive Landscape: Overview of major players, their strategies, and recent developments.

Detailed Patent Analysis which includes, top assignees, geography focus of top assignees, legal status, technology evolution, key patents and patent trends and innovations

Segmentation Analysis: Breakdown by product, platform, sample, end users, mode of acquiring and region.

Regional Insights: Key regional trends and growth opportunities.

Future Outlook: Strategic insights and future market direction.

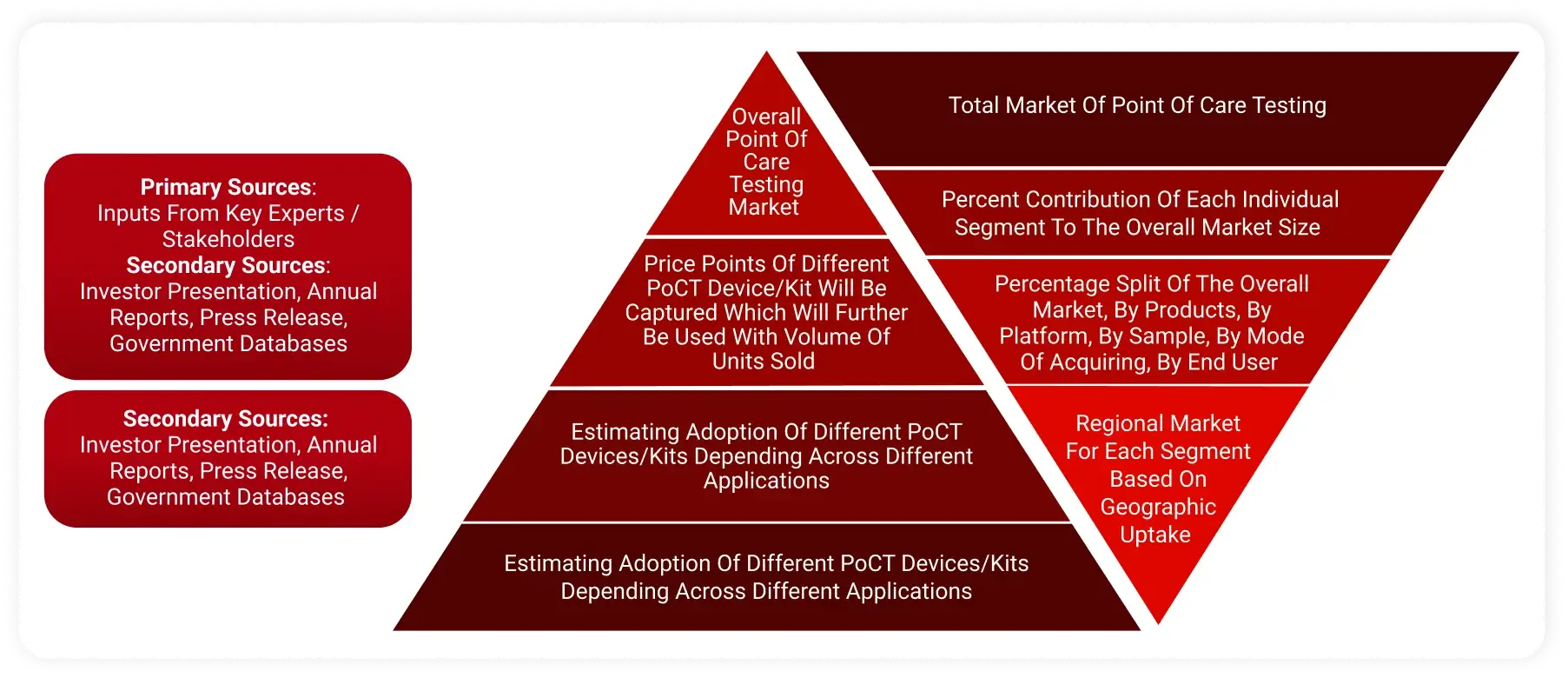

Research Methodology

The study of the point of care diagnostic market is based on a combination of primary and secondary research methodologies, supported by data validation and analytical modeling to ensure accuracy and reliability.

Market Definition: Point of Care diagnostic Market

The POCD marketplace encompasses the design, development, production and sales of quick, real-time diagnostic devices and kits that will provide timely medical results in or on-site to where a patient receives his or her care. Advanced technology such as biosensors, microfluidics, immunoassays and molecular diagnostics, among others, are used in POCD solutions to facilitate the rapid and accurate analysis of biological samples without requiring a centralized laboratory infrastructure. POCD allows for clinical decision making to be performed in real-time due to lower turnaround times from traditional lab testing and increase accessibility to diagnostics across hospitals, clinics, homes and remote areas.

Some of the major POCD products include blood glucose monitoring devices, infectious disease rapid test kits, cardiac markers analyzers, blood gases/electrolytes analyzers and molecular diagnostic platforms. POCD products are utilized for many purposes, including screening for diseases, management of chronic diseases, and emergency diagnostics. POCD enables decentralized, patient-centered delivery of health care, thus improving treatment outcomes, enhancing workflow efficiency, and increasing access to timely diagnostics.

Key Stakeholders

The point of care diagnostic market involves a diverse ecosystem of stakeholders:

- Diagnostic Device Manufacturers (POCT analyzers, test kits, and consumables providers)

- Reagent and Consumable Suppliers (assay developers, cartridges, test strips)

- Component and Technology Providers (biosensors, microfluidics, connectivity modules)

- Healthcare Providers (hospitals, clinics, diagnostic centers, home healthcare providers)

- Pharmaceutical and Biotechnology Companies

- Contract Research Organizations (CROs) and Clinical Laboratories

- Regulatory Authorities (e.g., U.S. Food and Drug Administration, European Medicines Agency)

- Research Institutions and Academic Organizations

- Pharmacies and Distribution Networks (retail pharmacies, online platforms, distributors)

- Digital Health and Telemedicine Providers

- Insurance Providers and Payers (public and private)

- Government and Public Health Agencies

- Investors (venture capital firms, private equity, strategic investors)

Key Objectives of the Study

- To define, describe, analyze, segment, and forecast the point of care diagnostic market by products, by platform, by sample, by end users, and by mode of acquiring.

- To describe and forecast the market for four key regions: North America, Europe, Asia Pacific, and Rest of the World.

- To provide detailed information regarding key drivers, restraints, opportunities, and challenges influencing market growth

- To strategically analyze the micro indicators with respect to individual growth trends, prospects, and contributions to the overall market size

- To analyze opportunities for stakeholders in the point of care diagnostic industry and emphasize on competitive landscape of the market.

- To develop competitive benchmarking of the key market players based on technology specifications and end users.

- To strategically profile key players and comprehensively analyze their product portfolio offerings, and core competencies

- To analyze competitive developments, such as launches and approvals, agreements, mergers and acquisitions, partnerships, joint ventures, investments and expansions, and collaborations, point of care diagnostic domain.

Need deeper insights on this market?

Get full report access with detailed forecasts, competitive analysis, and segmentation.

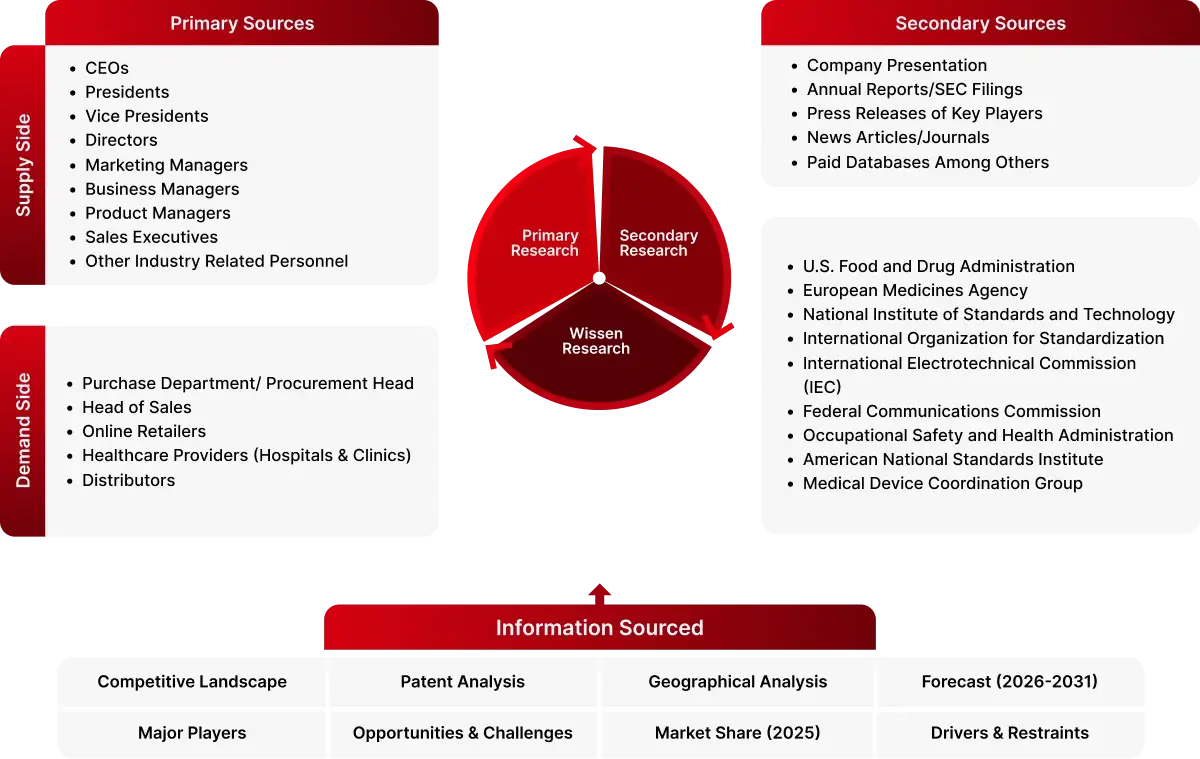

1. Research Approach

This research employs a systematic approach by using primary research along with secondary research to achieve full coverage and accuracy of information about the point of care diagnostic sector. Through this approach, the current market trends in terms of consumer behavior, technological developments, and competitive environment can be analyzed thoroughly.

Secondary Research

Secondary research involves the collection of data from reliable sources such as industry databases, company annual reports, investor presentations, and regulatory filings. This process helps in understanding market trends, identifying key players, and gathering technical and commercial insights.

A comprehensive database of leading companies and market participants is developed through secondary research to support further analysis.

Primary Research

Primary research is conducted to validate findings from secondary research and to gain deeper insights into market dynamics. Interviews are carried out with industry stakeholders across both demand and supply sides, including executives such as CXOs, Vice Presidents, and Directors from business development, marketing, and product teams.

Data is collected through structured questionnaires, email interactions, and telephonic interviews across key regions including North America, Europe, Asia Pacific, and Rest of the World.

Market Size Estimation

Market size estimation is performed using both top-down and bottom-up approaches. Key market players are identified, and their revenues are analyzed to estimate the overall market size.

- Product and service mapping across regions

- Adoption patterns across key application segments

- Insights gathered through primary and secondary research

Data Validation and Research Design

After estimating the overall market size, the data is validated using triangulation methods and market breakdown techniques to ensure accuracy and consistency. Both demand-side and supply-side factors are considered to refine the analysis.

The final data is validated through multiple sources to ensure reliability and to provide accurate insights across all market segments and regions.

2. Assumptions of the Study

The analysis of the point of care diagnostic market is based on the following key assumptions:

- Trends in the industry are drawn from historical data and current information within the sector

- The future outlook is underpinned by constant economic conditions in the absence of shocks to the market

- The rate of adoption for point of care diagnostic will rise steadily in all important regions

- Advancements in AI, connectivity, and lab-on-chip will continue to drive growth in the point-of-care diagnostic market.

- The income statement and market share figures are estimated using available information from the industry and publicly available data

- The exchange rate and price trends will not be greatly affected during the forecast period

Scope and Limitations

Scope of the Study

This report offers an exhaustive overview of the international point of care diagnostic market and includes the following components:

- Summary of market size, growth trends, and projections

- Carefully segmented market based on products, platform, sample, end users, by mode of acquiring and geography

- Discussion of primary factors influencing the market

- Competitor analysis

- Insights into regional and national market performance

Limitations of the Study

Despite the best efforts being made to keep the results accurate, the study does suffer from some limitations:

- It has been done using both primary and secondary data that come with their own constraints

- Rapid developments in technology might affect the future course of market dynamics

- Some figures are only approximations due to lack of public disclosure

- The report is not an insurance against any disruptions in macroeconomics and geopolitics

- Future forecasts are indicative and subject to change due to altered industry dynamics

3. Data Triangulation and Market Breakdown

Data triangulation involved the combination of primary research, secondary research, and the Wissen Research analysis. Once the data points were sourced from the secondary market research, we sanitized the data points to make the market sizing and growth forecast more accurate by developing our own assumptions based on the inputs and insights we gather through the primary interviews with the industry experts. Once the data was thoroughly validated through primary interviews from both, demand and supply side of the market, our team of analyst and other team members involved finalized the market sizing and growth forecast.

Data Triangulation Methodology

Sources: U.S. Food and Drug Administration, European Medicines Agency, National Institute of Standards and Technology, International Organization for Standardization, International Electrotechnical Commission, Federal Communications Commission, Occupational Safety and Health Administration, American National Standards Institute, Device Coordination Group, Company Website, Press Releases, Annual Reports, Paid Data Sources, and Wissen Research Analysis.

4. Years Framework

5. Bottom up approach (Demand Side) and Top down approach (Supply Side)

Bottom-Up Approach (Demand Side Approach):

Determining the market size through the consolidation of demand among end-users, sectors, and geographic areas, which are calculated according to real-world demand conditions.

Top Down Approach (Supply Side Approach):

Calculating the market size through revenue and performance of the industry and its important companies, allocating the market size among various sectors.