Wissen Research analyzed that the global Unmanned Aerial Vehicle (Drones) market was valued at USD 32 billion in 2024 and is projected to reach USD 63.1 billion by 2030, expected to grow at a CAGR of 12% during the forecast period, 2025-2030.

UAV (drones) market is driven by increasing adoption across defense, commercial, and civil sectors, fueled by advancements in autonomous flight, AI integration, and improved battery and sensor technologies. Growing demand for cost-effective aerial surveillance, precision agriculture, infrastructure inspection, and logistics solutions is accelerating market expansion. Supportive government investments, modernization of military capabilities, and evolving regulatory frameworks further boost UAV deployment globally. Additionally, rising interest in urban air mobility and drone delivery services presents new growth avenues.

Opportunities lie in expanding applications such as emergency response, environmental monitoring, and smart city initiatives, alongside innovations in propulsion systems and AI-powered autonomous operations. Emerging markets in Asia-Pacific and Latin America offer significant growth potential due to infrastructure development and regulatory evolution. The convergence of UAVs with 5G and data analytics also enables enhanced real-time decision-making, unlocking further commercial and industrial use cases.

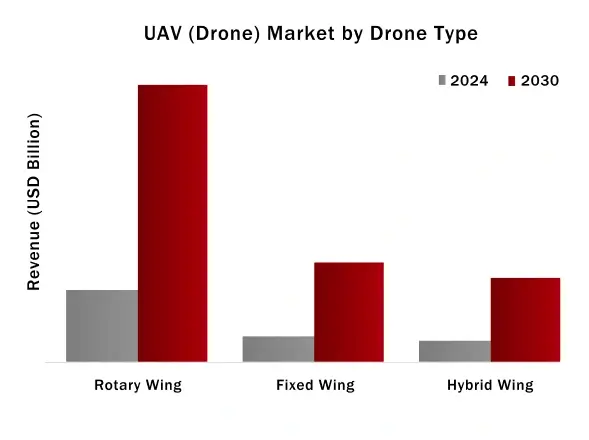

Rotary Wings in type of drone segment has held the largest share in the market since 2022 till current and Hybrid Wing is expected to show the highest growth during the forecast period, with North America dominating the regional market share.

Key players functioning in global UAV (Drones) sector are, SZ DJI Technology Co., Ltd. (China), Northrop Grumman Corporation (US), Israel Aerospace Industries Ltd. (Israel), Teledyne Flir LLC (US), General Atomics Aeronautical Systems (US), Raytheon Technologies Corporation (US), Parrot Drone SAS (France), Yuneec Holding Ltd. (China), Baykar Technologies (Turkey), Ehang Holdings Limited (China), Lockheed Martin (US), The Boeing Company (US), Aerovironment, Inc. (US), Textron Inc. (US), Bae Systems PLC (UK), Thales Group (France), Elbit Systems Ltd. (Israel), Aeronautics Ltd. (Israel), Skydio Inc. (US), Autel Robotics (China), among others.

Furthermore, the US with USD 12.48 billion market in 2024, held a significant share in the global UAV market and is likely to show the highest growth at a CAGR of 12.4% within this market, during the forecast period (2025-2030).

Global UAV market is anticipated to reach USD 63.1 billion by 2030 from USD 32 billion in 2024, growing at an annualized rate of 12% during the period, 2025-2030 | Asia-Pacific, led by China, Japan, and South Korea, has emerged as a global hub for UAV innovation and commercialization. Aggressive national policies, substantial investments in drone manufacturing, and the development of supportive regulatory frameworks are accelerating UAV adoption for both commercial and military applications, positioning the region as the fastest-growing UAV market worldwide | Asia-Pacific In Asia-Pacific, surging demand for efficient aerial solutions in agriculture, construction, and public safety is fueling rapid UAV market growth. National drone strategies, investment in local manufacturing, and the expansion of drone pilot training and support infrastructure are creating a robust ecosystem that supports both innovation and large-scale commercial deployment |

The UAV (drones) market is undergoing rapid transformation as advancements in propulsion systems, miniaturization, and autonomous flight technologies expand drone capabilities across commercial, defense, and civil sectors. This evolution is driving widespread deployment in logistics, precision agriculture, infrastructure inspection, and urban mobility, with particular momentum in regions prioritizing digital infrastructure and automation | Global investment in drone ecosystems—including advanced propulsion, AI-driven analytics, and drone traffic management systems—is expanding UAV use beyond traditional surveillance and mapping into sectors like healthcare delivery, disaster response, and energy infrastructure monitoring. For example, the integration of drones in emergency response and last-mile logistics highlights the technology’s growing role in critical infrastructure and public services. The market’s direction is shaped by evolving regulatory standards, supply chain constraints in high-performance electronics, and the need for harmonization in airspace management and data security. Public-private partnerships and international cooperation are proving essential to overcoming operational barriers and scaling UAV deployments across diverse geographies and industries | |

UAV Market: Strategic Activities

Drivers: Asia-Pacific Defense Modernization and Commercial Innovation Drive UAV Market Growth

Strong defense spending growth, national drone strategies, and public-private partnerships throughout Asia-Pacific are driving UAV adoption to support surveillance, logistics, agriculture, and infrastructure inspection. The intersection of advanced propulsion, AI-enhanced autonomy, and accommodating regulatory environments is facilitating mass deployment of UAVs in both the military and commercial markets, stimulating fast market growth.

Opportunities: Asia-Pacific UAV Ecosystem Opens New Horizons for Advanced Applications

Their aggressive scaling of native drone production, AI and sensor integration, and inter-industry partnerships are creating rich fertile ground for UAV innovation. The leadership in drone technology of the region combined with explosive demand for effective aerial solutions in smart cities, disaster relief, and precision agriculture offers substantial opportunities for both incumbents and new entrants.

Challenges: Adoption High Upfront Costs and Regulatory Complexity Limit UAV Market Penetration

Even with robust policy support, the UAV industry is plagued by ongoing challenges of high up-front investment needs, dispersed regulatory landscapes, and supply chain limitations for essential components. Airspace management, data security, and shortages in skilled workers add further complications to large-scale deployment and commercialization, particularly beyond pilot and demonstration phases.

The worldwide UAV (drones) market, covering fixed-wing, rotary-wing, and hybrid platforms, is experiencing strong growth driven by surging demand for defense, commercial, and civil sectors. The market will be worth about USD 35.6 billion in 2025 and is expected to grow past USD 63 billion by 2030 at a noteworthy CAGR of more than 12%. Main drivers for growth are fast development of autonomous flight, AI-driven analytics, and sensor technologies and growing adoption in use cases like surveillance, precision agriculture, logistics, infrastructure inspection, and emergency response. The market is dominated by Asia-Pacific due to aggressive national drone strategies, large investments in local manufacturing, and mass deployment in China, Japan, and South Korea. North America and Europe continue to be central, as they are hubs for technological innovation, regulatory development, and commercial adoption. Continuing developments in regulatory frameworks, incorporation of drones into urban air mobility, and moving into new emerging sectors are likely to further drive global UAV market expansion in the next few years.

Rotary Wings (Multirotor) segment dominated the UAV Market by Drone Type in 2024

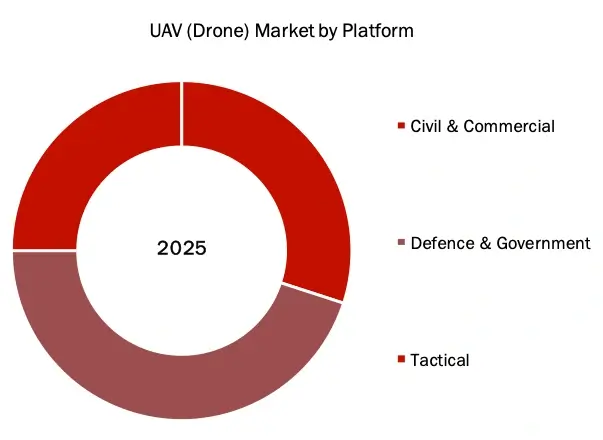

Defense and Government is estimated to hold the largest market share in 2025 in UAV market by Platform

North America held the largest market share in UAV Market in the forecast period (2025-2030)

North America commanded the highest market share in the UAV industry during the period of forecast (2025–2030), supported by high defense expenditure, a well-developed aerospace sector, and high penetration of drones in commercial applications like agriculture, logistics, and infrastructure inspection. For instance, the U.S. Department of Defense continues to be a key buyer of military drones, and regulatory innovation by the Federal Aviation Administration (FAA) has made it possible for expanded commercial drone flight operations, such as beyond visual line of sight (BVLOS) flight.

Major players operating in UAV (Drones) market are:

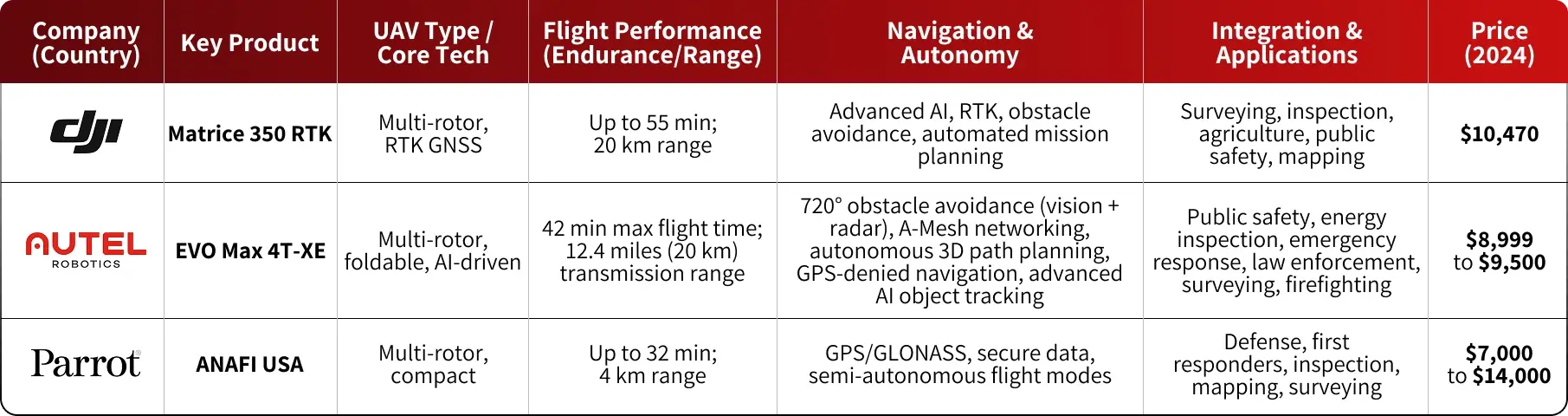

Note: The above pricing has been collected from company websites and third party sellers, latest as of 2024

Sources: Secondary Research

PRIMARY INSIGHTS FROM KEY OPINION LEADERS

“The rapid integration of AI and advanced sensors in UAVs is enabling new applications in precision agriculture, infrastructure inspection, and disaster response.”

CEO – Leading Drone Technology Company (North America)

“Collaborations between drone manufacturers and regulatory authorities are crucial for accelerating safe BVLOS (Beyond Visual Line of Sight) operations and scaling commercial drone services.”

Head of R&D – Major UAV Manufacturer (Europe)

“Asia-Pacific’s strong investment in drone manufacturing and supportive government policies are establishing the region as a global leader in both commercial and defense UAV deployments.”

CEO – Prominent UAV Solutions Provider (Asia-Pacific)

“Continuous improvements in battery technology and lightweight materials are driving longer flight times and expanding the operational range of drones across multiple industries.”

Head of Engineering – Leading Commercial Drone Manufacturer (North America)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

Particulars | Details |

Report | UAV (Drones) Market |

Forecast Period | 2025-2030 |

Base Year | 2024 |

Format | |

Market Size (2024) | USD 32 Billion |

CAGR (2025-2030) | 12% |

Number of Pages | 165 |

Number of Tables | 155 |

Number of Figures | 34 |

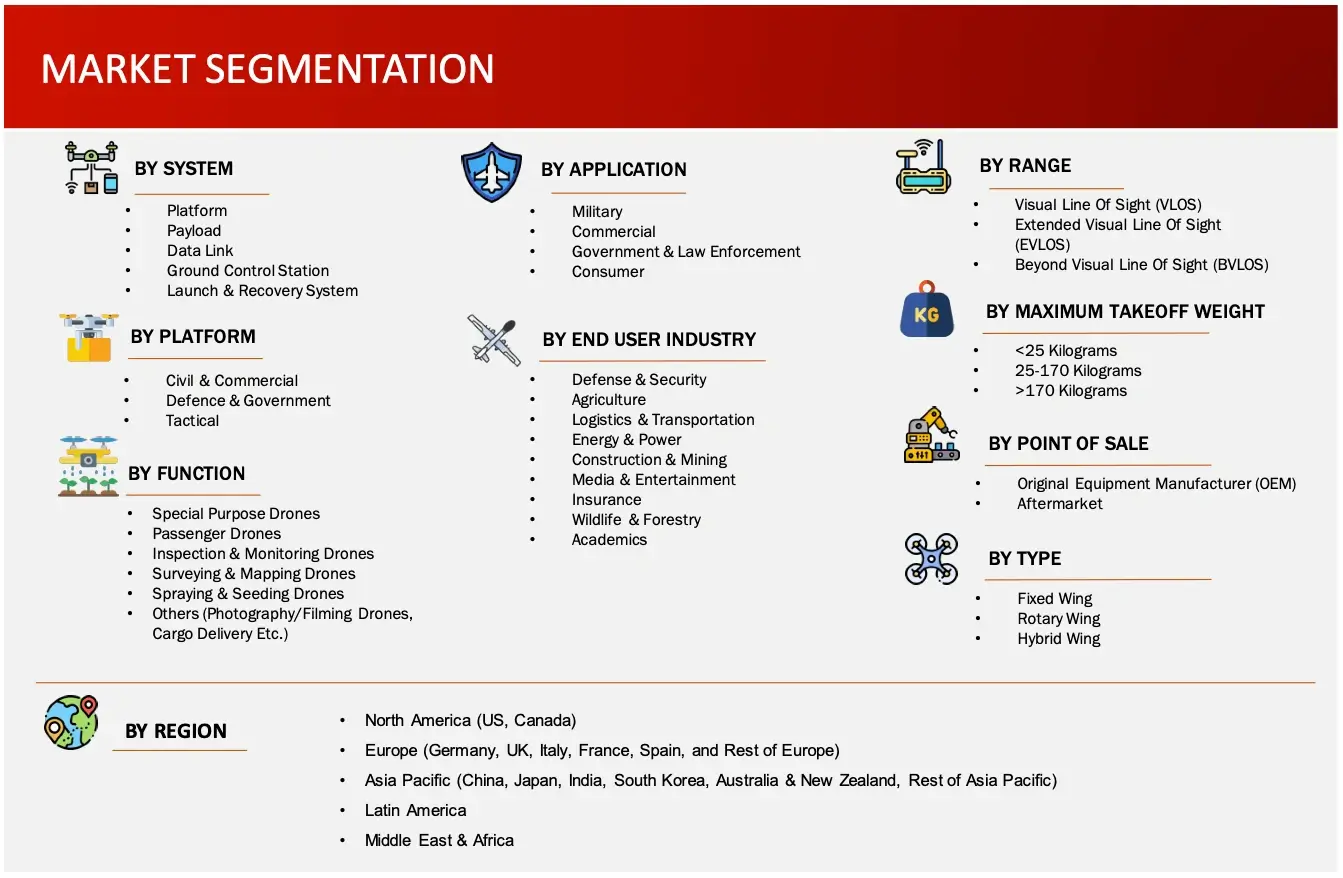

Key Segments | UAV Market Supply Outlook (Platform, Payload, Data Link, Ground Control Station, Launch & Recovery System) UAV Market Platform Outlook (Civil & Commercial, Defence & Government, Tactical) UAV Market Function Outlook (Special Purpose Drones, Passenger Drones, Inspection & Monitoring Drones, Surveying & Mapping Drones, Spraying & Seeding Drones, Others) Others include, Photography/Filming Drones, Cargo Delivery etc. UAV Market Application Outlook (Military, Commercial, Government & Law Enforcement, Consumer) UAV Market End User Industry Outlook (Defence & Security, Agriculture, Logistics & Transportation, Energy & Power, Construction & Mining, Media & Entertainment, Insurance, Wildlife & Forestry, Academics) UAV Market Range Outlook (Visual Line of Sight (VLOS), Extended Visual Line of Sight (EVLOS), Beyond Visual Line of Sight (BVLOS) UAV Market Maximum Take-off Weight Outlook (<25 Kilograms, 25-170 Kilograms, >170 Kilograms) UAV Market Point of Sale Outlook (Original Equipment Manufacturer (OEM), Aftermarket) UAV Market Type Outlook (Fixed Wing, Rotary Wing, Hybrid Wing) |

Regions Covered | § North America: US and Canada § Europe: Germany, UK, France, Italy, Spain, and Rest of the Europe § Asia-Pacific: China, Japan, India, South Korea, Australia and New Zealand, and Rest of the Asia-Pacific § Latin America § Middle East and Africa |

Key Players Covered (Majority Share Holders) | SZ DJI Technology Co., Ltd. (China), Northrop Grumman Corporation (US), Israel Aerospace Industries Ltd. (Israel), Teledyne Flir LLC (US), General Atomics Aeronautical Systems (US), Raytheon Technologies Corporation (US), Parrot Drone SAS (France), Yuneec Holding Ltd. (China), Baykar Technologies (Turkey), Ehang Holdings Limited (China), Lockheed Martin (US), The Boeing Company (US), Aerovironment, Inc. (US), Textron Inc. (US), Bae Systems PLC (UK), Thales Group (France), Elbit Systems Ltd. (Israel), Aeronautics Ltd. (Israel), Skydio Inc. (US), Autel Robotics (China) |

Other Players | Shield AI (US), Delair (France), Volocopter GMBH (Germany), Microdrones (Germany), Turkish Aerospace Industries (Turkey), Autel Robotics (China), Volansi, Inc. (US), Flyability (Switzerland), Wingtra (Switzerland), Garuda Aerospace (India) |

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. UAV (DRONE) MARKET: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. NEED GAP ANALYSIS

4.5. KEY CONFERENCES

4.6. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.7. INDUSTRY TRENDS

4.8. PORTER’S FIVE FORCES ANALYSIS

4.9. REGULATORY LANDSCAPE

4.9.1.NORTH AMERICA

4.9.2.EUROPE

4.9.3.ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. GLOBAL UAV (DRONE) MARKET BY, SYSTEM (2025-2030, USD MILLION)

6.1. PLATFORM

6.1.1.AIRFRAME

6.1.1.1. ALLOYS

6.1.1.2. PLASTICS

6.1.1.3. COMPOSITES

6.1.2.AVIONICS

6.1.2.1. FLIGHT CONTROL

6.1.2.2. NAVIGATION

6.1.2.3. SENSOR

6.1.2.4. COMMUNICATIONS

6.1.2.5. OTHERS

6.1.3.PROPULSION SYSTEMS

6.1.3.1. ENGINE

6.1.3.2. BATTERY

6.1.4.SOFTWARE

6.2. PAYLOAD

6.2.1.CAMERA

6.2.1.1. HIGH-RESOLUTION CAMERA

6.2.1.2. MULTISPECTRAL CAMERA

6.2.1.3. HYPERSPECTRAL CAMERA

6.2.1.4. THERMAL CAMERA

6.2.1.5. ELECTRO-OPTICAL (EO)/INFRARED (IR) CAMERA

6.2.2.INTELLIGENCE PAYLOAD

6.2.2.1. SIGNAL INTELLIGENCE (SIGINT)

6.2.2.2. ELECTRONIC INTELLIGENCE (ELINT)

6.2.2.3. COMMUNICATION INTELLIGENCE (COMINT)

6.2.2.4. TELEMETRY INTELLIGENCE (TELINT)

6.2.3.RADAR

6.2.3.1. SYNTHETIC APERTURE RADAR (SAR)

6.2.3.2. ACTIVE ELECTRONICALLY SCANNED ARRAY (AESA) RADAR

6.2.4.LIDAR

6.2.5.GIMBAL

6.3. DATA LINK

6.4. GROUND CONTROL STATION

6.5. LAUNCH & RECOVERY SYSTEM

7. GLOBAL UAV (DRONE) MARKET BY, PLATFORM (2025-2030, USD MILLION)

7.1. CIVIL & COMMERICIAL

7.1.1.MICRO

7.1.2.SMALL

7.1.3.MEDIUM

7.1.4.LARGE

7.2. DEFENCE & GOVERNMENT

7.3. TACTICAL

7.3.1.CLOSE RANGE

7.3.2.SHORT RANGE

7.3.3.MEDIUM RANGE

7.3.4.LONG RANGE

7.3.5.STRATEGIC

8. GLOBAL UAV (DRONE) MARKET BY, FUNCTION (2025-2030, USD MILLION)

8.1. SPECIAL PURPOSE DRONES

8.1.1.UCAVS

8.1.2.SWARM DRONES

8.1.3.STRATOSPHERIC DRONES

8.1.4.EXO-STRATOSPHERIC DRONES

8.2. PASSENGER DRONES

8.2.1.DRONE TAXIS

8.2.2.AIR SHUTTLES

8.2.3.AIR AMBULANCES

8.2.4.PERSONAL AIR VEHICLES

8.3. INSPECTION & MONITORING DRONES

8.4. SURVEYING & MAPPING DRONES

8.5. SPRAYING & SEEDING DRONES

8.6. OTHERS (PHOTOGRAPHY/FILMING DRONES, CARGO DELIVERY ETC.)

9. GLOBAL UAV (DRONE) MARKET BY, END USERS INDUSTRY (2025-2030, USD MILLION)

9.1. DEFENSE & SECURITY

9.2. AGRICULTURE

9.3. LOGISTICS & TRANSPORTATION

9.3.1.POSTAL & PACKAGE DELIVERY

9.3.2.HEALTHCARE & PHARMACY DELIVERY

9.3.3.RETAIL & FOOD DELIVERY

9.4. ENERGY & POWER

9.4.1.POWER GENERATION

9.4.2.OIL & GAS

9.5. CONSTRUCTION & MINING

9.6. MEDIA & ENTERTAINMENT

9.7. INSURANCE

9.8. WILDLIFE & FORESTRY

9.9. ACADEMICS

10. GLOBAL UAV (DRONE) MARKET BY, APPLICATION (2025-2030, USD MILLION)

10.1. MILITARY

10.1.1. INTELLIGENCE, SURVEILLANCE, AND RECONNAISSANCE (SR)

10.1.2. COMBAT OPERATIONS

10.1.2.1. Lethal

10.1.2.2. Stealth

10.1.2.3. Loitering munition

10.1.2.4. Target

10.1.3. DELIVERY

10.2. COMMERCIAL

10.2.1. REMOTE SENSING

10.2.2. INSPECTION & MONITORING

10.2.3. PRODUCT DELIVERY

10.2.4. SURVEYING & MAPPING

10.2.5. AERIAL IMAGING

10.2.6. INDUSTRIAL WAREHOUSING

10.2.7. PASSENGER & PUBLIC TRANSPORTATION

10.2.8. OTHERS

10.3. GOVERNMENT & LAW ENFORCEMENT

10.3.1. BORDER MANAGEMENT

10.3.2. TRAFFIC MONITORING

10.3.3. FIREFIGHTING & DISASTER MANAGEMENT

10.3.4. SEARCH & RESCUE

10.3.5. POLICE OPERATIONS & INVESTIGATION

10.3.6. MARITIME SECURITY

10.4. CONSUMER

10.4.1. PROSUMERS

10.4.2. HOBBYISTS

11. GLOBAL UAV (DRONE) MARKET BY, RANGE (2025-2030, USD MILLION)

11.1. VISUAL LINE OF SIGHT (VLOS)

11.2. EXTENDED VISUAL LINE OF SIGHT (EVLOS)

11.3. BEYOND VISUAL LINE OF SIGHT (BVLOS)

12. GLOBAL UAV (DRONE) MARKET BY, MAXIMUM TAKEOFF WEIGHT (MTOW) (2025-2030, USD MILLION)

12.1. <25 KILOGRAMS

12.2. 25-170 KILOGRAMS

12.3. >170 KILOGRAMS

13. GLOBAL UAV (DRONE) MARKET BY, POINT OF SALE (2025-2030, USD MILLION)

13.1. ORIGINAL EQUIPMENT MANUFACTURER (OEM)

13.2. AFTERMARKET

14. GLOBAL UAV (DRONE) MARKET BY, TYPE (2025-2030, USD MILLION)

14.1. FIXED WING

14.1.1. CTOL

14.1.2. VTOL

14.2. ROTARY WING

14.2.1. SINGLE ROTOR

14.2.2. MULTI-ROTOR

14.2.3. BICOPTER

14.2.4. TRICOPTER

14.2.5. QUADCOPTER

14.2.6. HEXACOPTER

14.2.7. OCTOCOPTER

14.3. HYBRID WING

15. GLOBAL UAV (DRONE) MARKET BY, REGION (2025-2030, USD MILLION)

15.1. NORTH AMERICA

15.1.1. US

15.1.2. CANADA

15.2. EUROPE

15.2.1. GERMANY

15.2.2. FRANCE

15.2.3. SPAIN

15.2.4. ITALY

15.2.5. UK

15.2.6. REST OF THE EUROPE

15.3. ASIA-PACIFIC

15.3.1. CHINA

15.3.2. JAPAN

15.3.3. INDIA

15.3.4. AUSTRALIA AND NEW ZEALAND

15.3.5. SOUTH KOREA

15.3.6. REST OF THE ASIA-PACIFIC

15.4. MIDDLE EAST AND AFRICA

15.5. LATIN AMERICA

16. COMPETITIVE ANALYSIS

16.1. REVENUE ANALYSIS

16.2. KEY PLAYERS FOOTPRINT ANALYSIS

16.3. MARKET SHARE ANALYSIS (2023/2024)

16.4. REGIONAL SNAPSHOT OF KEY PLAYERS

16.5. R&D EXPENDITURE OF KEY PLAYERS

16.6. BRAND/ PRODUCT COMPARISON

17. COMPANY PROFILES

17.1. SZ DJI TECHNOLOGY CO., LTD.

17.1.1. BUSINESS OVERVIEW

17.1.2. PRODUCT PORTFOLIO

17.1.3. FINANCIAL SNAPSHOT

17.1.4. RECENT DEVELOPMENTS

17.1.4.1. MERGER/ACQUISITIONS

17.1.4.2. PRODUCT APPROVAL/LAUNCHES

17.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

17.1.4.4. EXPANSIONS

17.2. NORTHROP GRUMMAN CORPORATION (US)

17.3. ISRAEL AEROSPACE INDUSTRIES LTD. (ISRAEL)

17.4. TELEDYNE FLIR LLC (US)

17.5. GENERAL ATOMICS AERONAUTICAL SYSTEMS (US)

17.6. RAYTHEON TECHNOLOGIES CORPORATION (US)

17.7. PARROT DRONE SAS (FRANCE)

17.8. YUNEEC HOLDING LTD. (CHINA)

17.9. EHANG HOLDINGS LIMITED (CHINA)

17.10. LOCKHEED MARTIN (US)

17.11. THE BOEING COMPANY (US)

17.12. AEROVIRONMENT, INC. (US)

17.13. TEXTRON INC. (US)

17.14. BAE SYSTEMS PLC (UK)

17.15. THALES GROUP (FRANCE)

17.16. ELBIT SYSTEMS LTD. (ISRAEL)

17.17. AERONAUTICS LTD. (ISRAEL)

17.18. SKYDIO INC. (US)

17.19. BAYKAR TECHNOLOGIES (TURKEY)

17.20. OTHER PLAYERS

17.20.1. SHIELD AI (US)

17.20.2. DELAIR (FRANCE)

17.20.3. VOLOCOPTER GMBH (GERMANY)

17.20.4. MICRODRONES (GERMANY)

17.20.5. TURKISH AEROSPACE INDUSTRIES (TURKEY)

17.20.6. AUTEL ROBOTICS (CHINA)

17.20.7. VOLANSI, INC. (US)

17.20.8. FLYABILITY (SWITZERLAND)

17.20.9. WINGTRA (SWITZERLAND)

17.20.10. GARUDA AEROSPACE (INDIA)

18. APPENDIX

18.1. INDUSTRY SPEAK

18.2. QUESTIONNAIRE/DISCUSSION GUIDE

18.3. AVAILABLE CUSTOM WORK

18.4. ADJACENT STUDIES

18.5. AUTHORS

The UAV (drone) industry involves the design, production, and deployment of unmanned aerial vehicles—airplanes without an onboard human pilot, controlled remotely or autonomously by onboard systems. It involves a broad range of applications across military, commercial, and civil domains. UAVs are mounted with multiple payloads such as cameras, sensors, and delivery units, supporting capabilities such as surveillance, reconnaissance, aerial imaging, infrastructure inspection, precision agriculture, logistics, and disaster relief.

Spurred on by aggressive advances in AI technology, sensor technology, and battery life, UAVs have become more diversified and potent, serving both government and commercial purposes. The market is dominated by constant innovation, widening regulatory environments, and intense investment by both traditional aerospace companies and tech start-ups. With expanding use of UAVs in each industry, the market itself continues to shift, providing greater operating efficiency, automation, and real-time data capabilities.

FIGURE: UAV (DRONE) MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

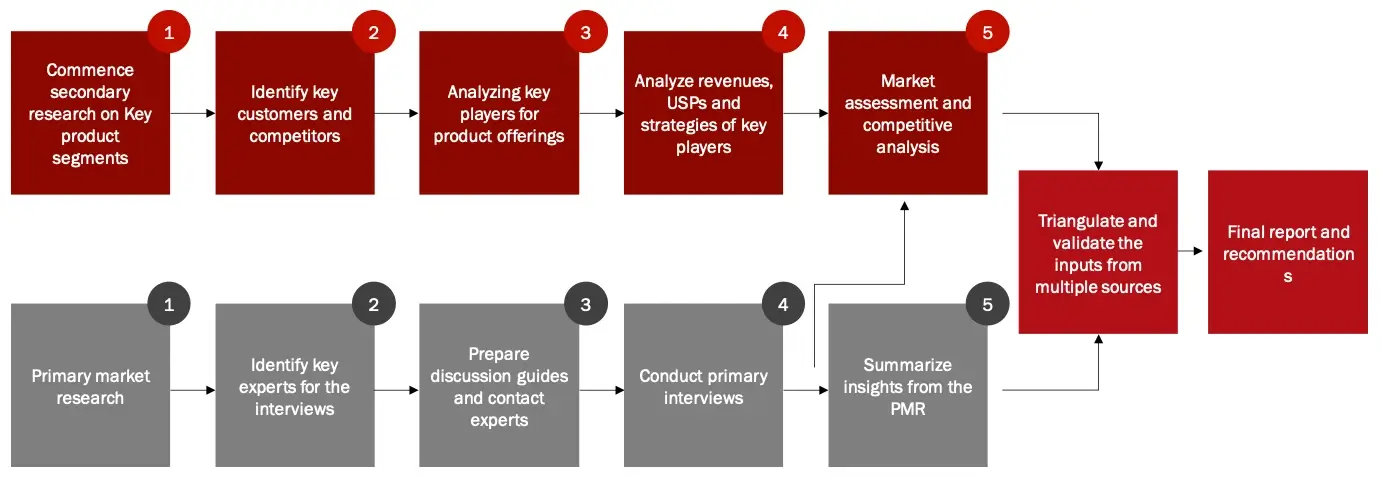

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the UAV market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the UAV technology market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the UAV market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major manufacturers offering various UAV will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of UAV market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the UAV market industry.