Wissen Research analysed that the global Conversational Artificial Intelligence (AI) market was valued at USD 15 billion in 2024 and is projected to reach USD 44.8 billion by 2030, expected to grow at a CAGR of 20% during the forecast period, 2025-2030.

The major growth drivers of the conversational AI market are speedy developments in natural language processing and machine learning, increasing need for effective and personalized customer interactions, prevalent use of AI-driven chatbots and virtual assistants across all industries, and conversational AI integration with digital channels and business applications.

Challenges in this area involve data privacy and security issues, exorbitant implementation and maintenance expenses, regulatory ambiguities, and the complexity of creating context-sensitive, multilingual, and emotionally intelligent systems

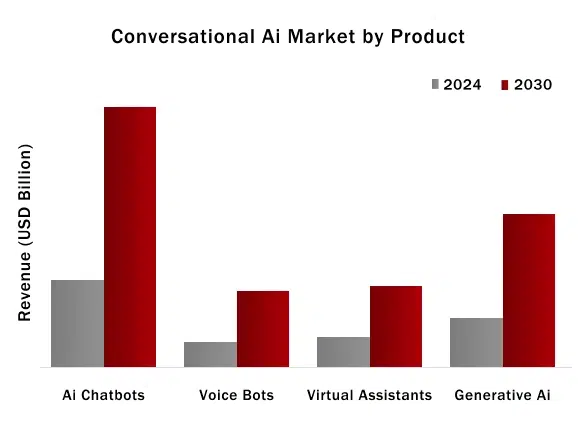

AI Chatbot segment have held the largest share in the market since 2022 and during the forecast period, with North America dominating the regional market share.

Global Conversational AI market is anticipated to reach USD 44.8 billion by 2030 from USD 15 billion in 2024, growing at an annualized rate of 20% during the period, 2025-2030 | The Asia Pacific region, spearheaded by China and India, is proving to be the most rapidly expanding conversational AI market, driven by enormous internet user bases, government-sponsored digitalization efforts, and a boom in local AI start-ups building solutions specific to regional languages and cultural environments. | Trans-Atlantic In North America and Europe, demand for AI-driven customer service and adoption of explainable and ethical AI platforms are fueling innovation, whereas in Latin America, the Middle East, and Africa, increasing digital adoption and AI investment are creating new growth horizons for providers of conversational AI solutions |

The market for conversational AI is rapidly evolving as generative AI and next-generation natural language processing models allow for more contextual, emotionally responsive, and multilingual conversations. This is giving rise to the adoption of intelligent chatbots and virtual agents across industries like banking, health, and retail, where they mechanize complicated processes and provide hyper-personalized customer experiences. | Increased worldwide investment in AI infrastructure and cloud platforms is speeding the adoption of conversational AI as part of omnichannel strategies, enabling businesses to provide continuous, always-on support across messaging, voice, and social channels. For instance, Walmart’s integration of generative AI-based search and customer service capabilities showcases how conversational AI is being applied to personalize shopping and optimize operations at scale. The market is also being influenced by macroeconomic and regulatory changes, including technology import tariffs and changing data privacy regulations, that are affecting the cost structure, deployment models, and cross-border collaboration of conversational AI providers. |

Drivers: Omnichannel Conversational AI Integration Fuels Seamless Enterprise Engagement

Omnichannel deployment and convergence of conversational AI on messaging, voice, and social platforms are driving enterprise adoption, allowing companies to provide seamless, always-on customer interactions and automate sophisticated workflows at scale.

Opportunities: Asia Pacific’s Digital Surge Unlocks New Growth Frontiers for Conversational AI Solutions

Accelerating digitalization and AI-driven government support in Asia Pacific, most notably in China and India, are establishing fertile ground for conversational AI offerings adapted to local language, cultural environments, and surging internet user bases, offering strong market growth opportunities

Challenges: Regulatory and Tariff Complexities Raise Barriers for Global Conversational AI Deployment

Emerging global data privacy laws and cross-border tariff shocks are mounting compliance expenses and business complexity for conversational AI providers, particularly those depending on foreign cloud infrastructure and real-time data pipelines.

The global conversational AI market, encompassing chatbots, virtual assistants, and AI-powered voice agents, is experiencing rapid expansion driven by surging demand for automated, personalized customer engagement, advances in natural language processing and generative AI, and the proliferation of omnichannel digital platforms. Valued at USD 15 billion in 2024, the market is projected to reach over USD 44.8 billion by 2030, growing at a CAGR of 20%. Key growth drivers include the need for 24/7 customer support, cost-effective automation, and the integration of conversational AI across sectors such as retail, banking, healthcare, and e-commerce, with North America leading in adoption and Asia Pacific emerging as the fastest-growing region.

AI Chatbot segment dominated the Conversational AI Market by Product in 2024

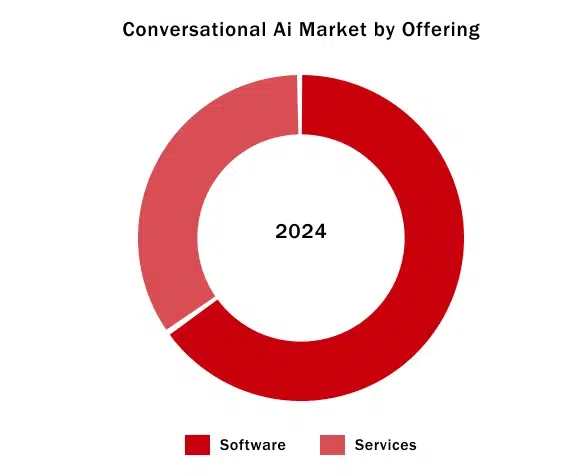

Software Segment held the largest market share in 2024, accounting for a significant market share in Conversational AI market by Offering

North America held the largest market share in conversational AI Market in the forecast period (2025-2030)

North America led the conversational AI market throughout the forecast period (2025–2030), with more than 25% of global market share in 2024, due to the maturity of the digital infrastructure in the region, high density of AI innovators, and early uptake across key industries like healthcare, retail, and financial services. The presence of tech giants such as Google, Microsoft, and Amazon, along with a mature startup ecosystem and record-breaking rates of business formation, has propelled innovation and implementation of AI-based chatbots, virtual assistants, and voice-based solutions. Regulatory environments conducive to AI development, R&D investments, and ubiquitous adoption of smart devices further reinforce North America’s leadership. For instance, the fast spread of voice-activated devices such as Amazon Alexa and Google Assistant and business uptake of conversational AI for customer interaction and operational effectiveness speaks to the region’s role in shaping the global conversational AI market.

Furthermore, the US with USD 3.7 billion market in 2024, holds majority share in the global Conversational AI market and is likely to remain the leading region growing at a CAGR of 20% within this market, during the forecast period.

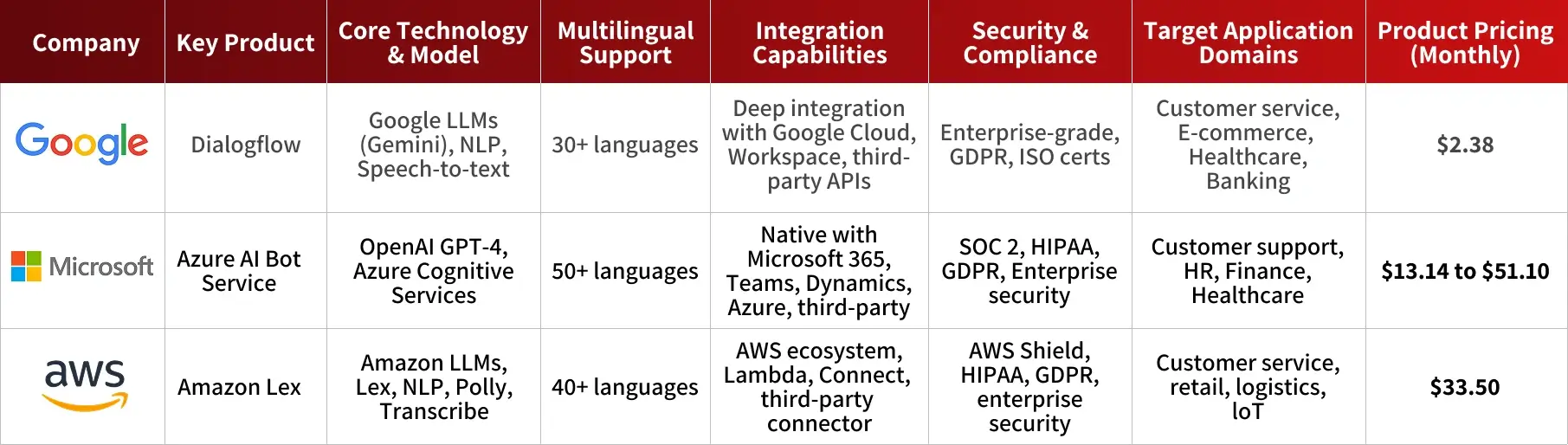

Major players operating in conversational AI market are:

Note: The aforementioned pricing is for the monthly payment cycle of the product, collected from company websites.

Sources: Secondary Research

PRIMARY INSIGHTS FROM KEY OPINION LEADERS

“Generative AI and advanced NLP are enabling conversational AI systems to deliver hyper-personalized, context-aware interactions that drive customer engagement and operational efficiency.”

CEO – Leading Tech Company (Europe)

“The rapid adoption of multimodal conversational AI—integrating voice, text, and visual inputs—is making digital interactions more intuitive and accessible across devices and platforms.”

Head of R&D – Leading Electronics Manufacturer (Asia-Pacific)

“Emotional intelligence and empathy in AI chatbots are emerging as key differentiators, especially in sectors like healthcare and finance where sensitive, human-like support enhances trust and satisfaction.”

CEO- Leading Tech Company (North American)

“Asia Pacific is witnessing explosive growth in conversational AI adoption, propelled by digital transformation initiatives, a large internet user base, and solutions tailored for regional languages and cultural contexts”

Head of R&D- Leading AI and Cloud Software Provider (Asia Pacific)

Particulars | Details |

Report | Conversational AI Market |

Forecast Period | 2025-2030 |

Base Year | 2024 |

Format | |

Market Size (2024) | USD 15 Billion |

CAGR (2025-2030) | 20% |

Number of Pages | 165 |

Number of Tables | 155 |

Number of Figures | 34 |

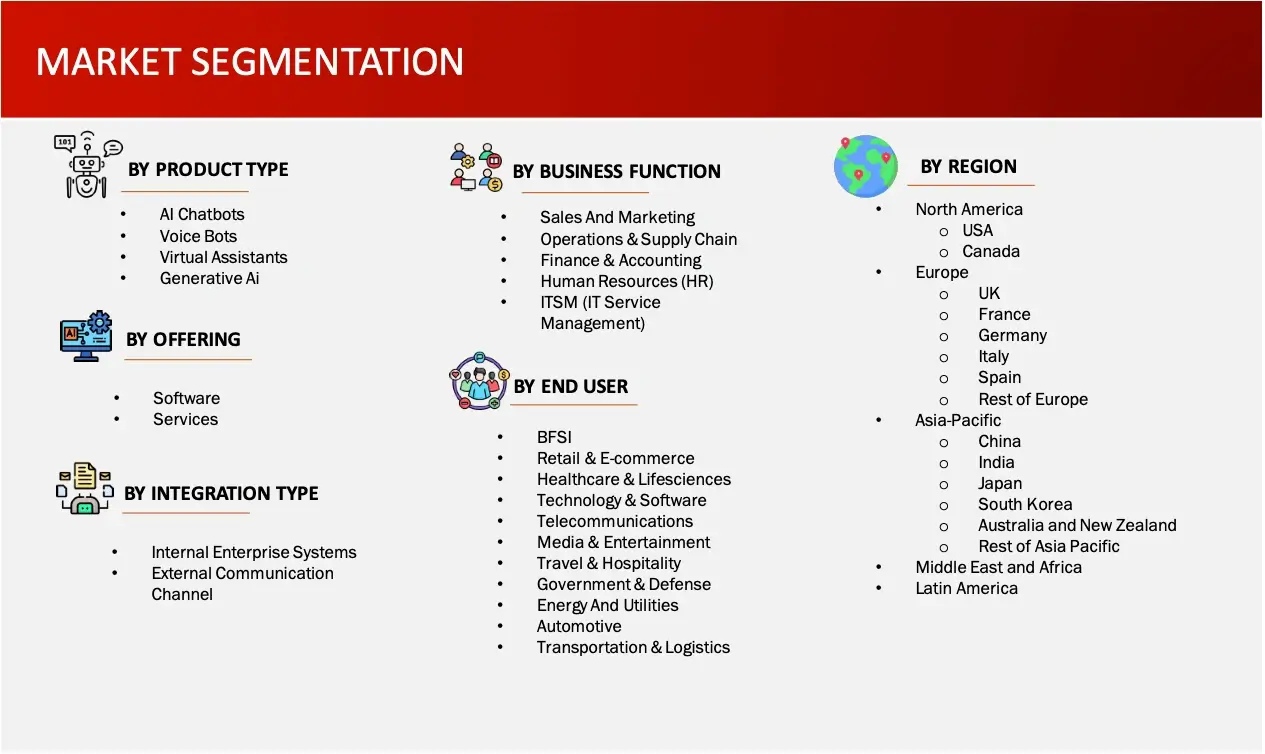

Key Segments | Conversational AI Market Products Outlook (AI Chatbots, Voice Bots, Virtual Assistants, Generative AI) Conversational AI Market Offerings Outlook (Software, Services) Conversational AI Market Integration Outlook (Internal Enterprise Systems, External Communication Channel) Conversational AI Market Business Function Outlook (Sales & Marketing, Operations & Supply Chain, Finance & Accounting, Human Resources (HR), ITSM (IT Service Management) Conversational AI Market End User Outlook (BFSI, Retail & E-commerce, Healthcare & Lifesciences, Technology & Software, Telecommunications, Media & Entertainment, Travel & Hospitality, Government & Defence, Energy & Utilities, Automotive, Transportation & Logistics) |

Regions Covered | § North America: US and Canada § Europe: Germany, UK, France, Italy, Spain, and Rest of the Europe § Asia-Pacific: China, Japan, India, South Korea, Australia and New Zealand, and Rest of the Asia-Pacific § Latin America § Middle East and Africa |

Key Players Covered (Majority Share Holders) | IBM (US), Google (US), AWS (US), Microsoft (US), Kore.AI (US), Oracle (US), OpenAI (US), Baidu (China), SAP (Germany), Liveperson (US), eGain (US), Soundhound AI (US), Verint (US), Anthropic (US), Sprinkler (US), Twilio (US) |

Other Players | Teneo.AI (Sweden), Aisera (US), Laiye (China), Omilia (UK), Inbenta (US), Avaamo (US), Cognigy (Germany), Onereach.AI (US), Boost.AI (Norway), Haptik (India), Conversica (US), Quiq (US), Rasa (Germany), Pypestream (US), Creative Virtual (UK), Senseforth.AI (India) |

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. CONVERSATIONAL AI: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. NEED GAP ANALYSIS

4.5. KEY CONFERENCES

4.6. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.7. INDUSTRY TRENDS

4.8. PORTER’S FIVE FORCES ANALYSIS

4.9. REGULATORY LANDSCAPE

4.9.1.NORTH AMERICA

4.9.2.EUROPE

4.9.3.ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. GLOBAL CONVERSATIONAL AI MARKET BY, OFFERING (2025-2030, USD MILLION)

6.1. SOFTWARE

6.2. SERVICES

7. GLOBAL CONVERSATIONAL AI MARKET BY, PRODUCT TYPE (2025-2030, USD MILLION)

7.1. AI CHATBOTS

7.2. VOICE BOTS

7.3. VIRTUAL ASSISTANTS

7.4. GENERATIVE AI

8. GLOBAL CONVERSATIONAL AI MARKET BY, BUSINESS FUNCTION (2025-2030, USD MILLION)

8.1. SALES AND MARKETING

8.1.1.CONTACT CENTER AUTOMATION

8.1.2.BRANDING & ADVERTISEMENT

8.1.3.CAMPAIGN MANAGEMENT

8.1.4.CUSTOMER ENGAGEMENT & RETENTION

8.1.5.OTHERS

8.2. OPERATIONS & SUPPLY CHAIN

8.2.1.WORKFLOW OPTIMISATION

8.2.2.SCEDULING & ROUTING

8.2.3.INVENTORY MANAGEMENT

8.2.4.VENDOR MANAGEMENT

8.2.5.TASK & PROJECTS MANAGEMENT ASSISTANCE

8.2.6.OTHERS

8.3. FINANCE & ACCOUNTING

8.3.1.VIRTUAL FINANCIAL ADVISORS

8.3.2.EXPENSE TRACKING & REPORTING

8.3.3.DATA PRIVACY AND COMPLIANCE MANAGEMENT

8.3.4.AUTOMATED INVOICE PROCESSING

8.3.5.OTHERS

8.4. HUMAN RESOURCES (HR)

8.4.1.EMPLOYEE ENGAGEMENT & ONBOARDING

8.4.2.PERFORMANCE MANAGEMENT

8.4.3.DOCUMENT MANAGEMENT

8.4.4.RECRUITING ASSISTANTS & SCREENING

8.4.5.OTHERS

8.5. ITSM (IT SERVICE MANGEMENT)

8.5.1.INCIDENT MANAGEMENT

8.5.2.COST OPTIMISATION

8.5.3.QUERY HANDLING

8.5.4.KNOWLEDGE MANAGEMENT

8.5.5.OTHERS

9. GLOBAL CONVERSATIONAL AI MARKET BY, INTEGRATION TYPE (2025-2030, USD MILLION)

9.1. INTERNAL ENTERPRISE SYSTEMS

9.1.1.CRM

9.1.2.KNOWLEDGE BASED SYSTEMS

9.2. EXTERNAL COMMUNICATION CHANNEL

9.2.1.MOBILE APPS

9.2.2.IVR SYSTEMS

9.2.3.MESSAGING SERVICES/ PLATFORMS

9.2.4.WEBSITES

10. GLOBAL CONVERSATIONAL AI MARKET BY, END USER (2025-2030, USD MILLION)

10.1. BFSI (BANKING, FINANCIAL SERVICES, AND INSURANCE)

10.2. RETAIL & E-COMMERCE

10.3. HEALTHCARE & LIFESCIENCES

10.4. TECHNOLOGY & SOFTWARE

10.5. TELECOMMUNICATIONS

10.6. MEDIA & ENTERTAINMENT

10.7. TRAVEL & HOSPITALITY

10.8. GOVERNMENT & DEFENSE

10.9. ENERGY AND UTILITIES

10.10. AUTOMOTIVE

10.11. TRANSPORTATION & LOGISTICS

10.12.OTHER ENTERPRISES

11. GLOBAL CONVERSATIONAL AI MARKET BY, REGION (2025-2030, USD MILLION)

11.1. NORTH AMERICA

11.1.1. US

11.1.2. CANADA

11.2. EUROPE

11.2.1. GERMANY

11.2.2. FRANCE

11.2.3. SPAIN

11.2.4. ITALY

11.2.5. UK

11.2.6. REST OF THE EUROPE

11.3. ASIA-PACIFIC

11.3.1. CHINA

11.3.2. JAPAN

11.3.3. INDIA

11.3.4. AUSTRALIA AND NEW ZEALAND

11.3.5. SOUTH KOREA

11.3.6. REST OF THE ASIA-PACIFIC

11.4. MIDDLE EAST AND AFRICA

11.5. LATIN AMERICA

12. COMPETITIVE ANALYSIS

12.1. REVENUE ANALYSIS

12.2. KEY PLAYERS FOOTPRINT ANALYSIS

12.3. MARKET SHARE ANALYSIS (2023/2024)

12.4. REGIONAL SNAPSHOT OF KEY PLAYERS

12.5. R&D EXPENDITURE OF KEY PLAYERS

12.6. BRAND/ PRODUCT COMPARISON

13.1. IBM

13.1.1. BUSINESS OVERVIEW

13.1.2. PRODUCT PORTFOLIO

13.1.3. FINANCIAL SNAPSHOT

13.1.4. RECENT DEVELOPMENTS

13.1.4.1. MERGER/ACQUISITIONS

13.1.4.2. PRODUCT APPROVAL/LAUNCHES

13.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

13.1.4.4. EXPANSIONS

13.2. GOOGLE (US)

13.3. AWS (US)

13.4. MICROSOFT (US)

13.5. KORE.AI (US)

13.6. ORACLE (US)

13.7. OPEN AI (US)

13.8. BAIDU (China)

13.9. SAP (Germany)

13.10. LIVEPERSON (US)

13.11. EGAIN (US)

13.12. SOUNDHOUND AI (US)

13.13. VERINT (US)

13.14. ANTHROPIC (US)

13.15. SPRINKLR (US)

13.16. TWILIO (US)

13.17. OTHER PLAYERS

13.17.1. ΤΕΝΕΟ.ΑΙ (UK)

13.17.2. AISERA (US)

13.17.3. LAIYE (China)

13.17.4. OMILIA (UK)

13.17.5. INBENTA (US)

13.17.6. AVAAMO (US)

13.17.7. COGNIGY (Germany)

13.17.8. ONEREACH.AI (US)

13.17.9. BOOST.AI (Norway)

13.17.10. HAPTIK (India)

13.17.11. CONVERSICA (US)

13.17.12. QUIQ (US)

13.17.13. RASA (Germany)

13.17.14. PYPESTREAM (US)

13.17.15. CREATIVE VIRTUAL (UK)

13.17.16. SENSEFORTH.AI (India)

13.17.17. RULAI (US)

13.17.18. VERLOOP.IO (India)

13.17.19. KASISTO (US)

13.17.20. EXCEED.AI (US)

13.17.21. CLINC (US)

13.17.22. MINDMELD (US)

14. APPENDIX

14.1. INDUSTRY SPEAK

14.2. QUESTIONNAIRE/DISCUSSION GUIDE

14.3. AVAILABLE CUSTOM WORK

14.4. ADJACENT STUDIES

14.5. AUTHORS

15. REFERENCES

The conversational AI market encompasses software and platforms that enable machines to simulate human-like conversations using natural language processing (NLP), machine learning, and speech recognition technologies. This market includes chatbots, virtual assistants, voice-enabled devices, and automated customer service solutions deployed across industries to enhance user engagement, automate interactions, and improve operational efficiency.

FIGURE: CONVERSATIONAL AI MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the conversational AI market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the conversational AI market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the conversational AI market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major manufacturers offering various conversational AI will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of conversational AI market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the conversational AI market industry.