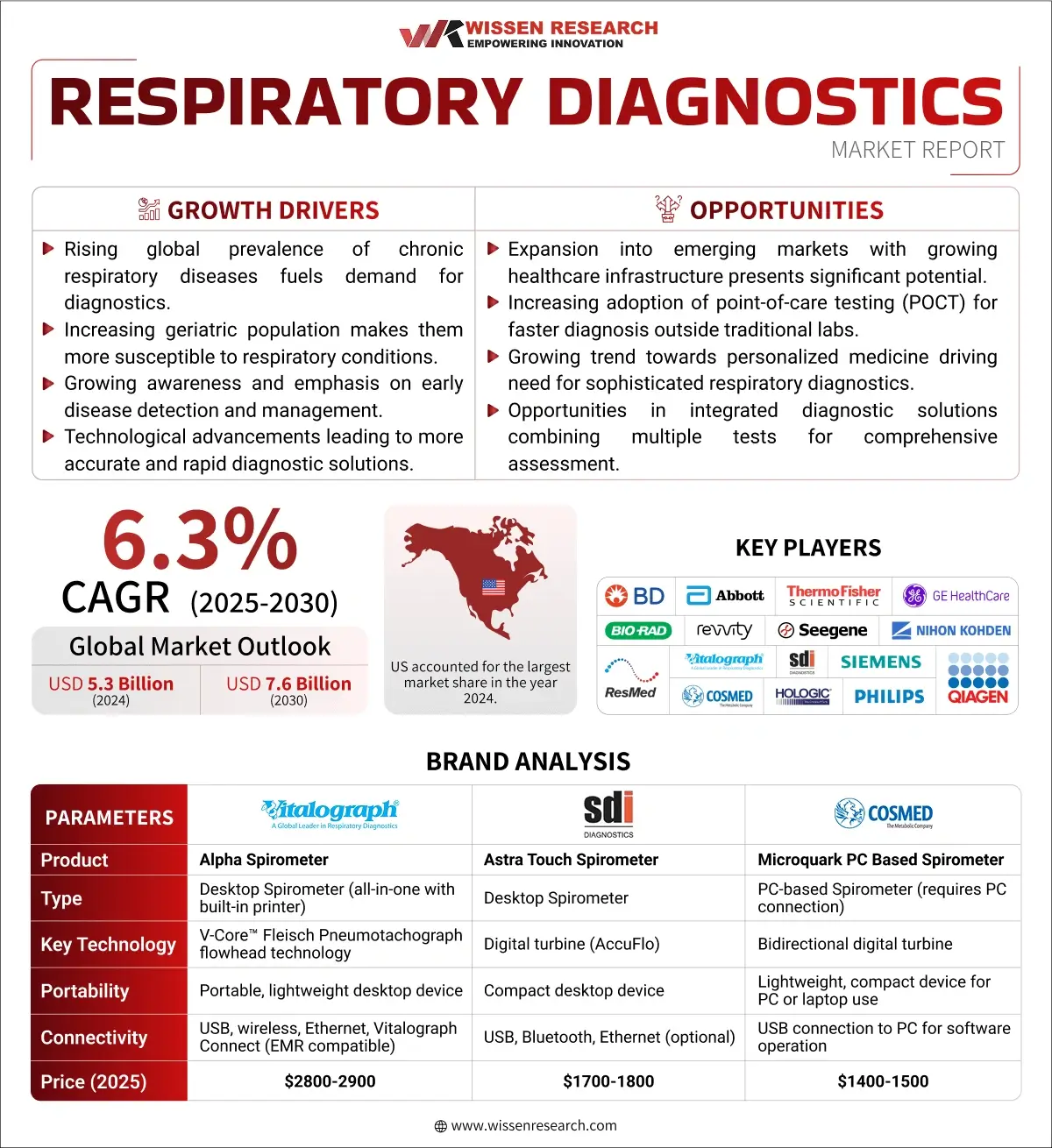

Wissen Research analyzed that the global respiratory diagnostics market was valued at USD 5.3 billion in 2024 and is projected to reach USD 7.6 billion by 2030, expected to grow at a CAGR of 6.3 % during the forecast period, 2025-2030.

Lucrative Opportunities: Respiratory Diagnostics Market

Global respiratory diagnostics market is anticipated to reach USD 7.6 billion by 2030 from USD 5.3 billion in 2024, growing at an annualized rate of 6.3% during the forecast period, 2025-2030 | Europe is an important player in the respiratory diagnostics market. This is due to its well-established healthcare systems, strong regulatory frameworks, significant investments in respiratory health research, and a high prevalence of respiratory diseases like asthma and COPD across its countries. | Asia-Pacific The Asia-Pacific region is seeing rapid growth in the respiratory diagnostics market. This growth is driven by a large aging population, the increasing prevalence of respiratory diseases worsened by air pollution, rising healthcare investment, and expanding local diagnostic and biotech efforts. |

Technologies like Next-Generation Sequencing (NGS) for identifying genetic causes of respiratory conditions, molecular diagnostics such as PCR and digital PCR for rapid pathogen detection, and pulmonary function monitoring systems are changing respiratory diagnostics. | Globally, research in respiratory diagnostics focuses on validating biomarkers for early detection of lung cancer and flare-ups in chronic diseases. It aims to improve the accuracy and accessibility of Point-of-Care (POC) testing devices, predict patient outcomes based on diagnostic data, integrate multi-omics approaches for a better understanding of disease mechanisms, standardize testing methods across different platforms, and apply new diagnostic discoveries in clinical practice for better patient management. |

Strategic Activities

Drivers: Rising Prevalence of Respiratory Diseases

The most significant driver of the respiratory diagnostic market is the escalating global prevalence of respiratory diseases, fueled by multiple interconnected factors that are fundamentally reshaping healthcare demands worldwide. Air pollution has emerged as a critical catalyst, with the State of Global Air Report 2024 revealing that air pollution accounts for 8.1 million deaths globally in 2021, becoming the second leading risk factor for death worldwide. The report specifically notes that 99% of the global population breathes air exceeding World Health Organization guideline limits, with fine particulate matter (PM2.5) responsible for 90% of the total air pollution disease burden. This environmental crisis is directly manifesting in respiratory health statistics that validate the market’s growth trajectory. Chronic obstructive pulmonary disease (COPD) alone affects over 550 million adults globally, while asthma impacts more than 262 million people worldwide. The aging population compounds this challenge significantly, as individuals aged over 65 years are at substantially higher risk for developing COPD and other respiratory conditions. According to the World Health Organization, the global population aged 60 years or older is expected to grow by 56% from 2015 to 2030, creating an unprecedented demand for respiratory diagnostic solutions. The market’s response to this demand is reflected in high growth projections.

Opportunities: Point-of-Care Testing and AI Integration.

Most promising opportunity in the respiratory diagnostic market lies in the convergence of point-of-care testing technologies with artificial intelligence integration, creating transformative potential for healthcare delivery accessibility and diagnostic accuracy. Point-of-care testing represents a paradigm shift from centralized laboratory diagnostics to decentralized, immediate testing capabilities. The respiratory segment is particularly well-positioned to benefit from this transformation, as POC tests offer the advantage of quick results, often within minutes, which is critical in managing and controlling respiratory diseases. The convenience and speed of POC tests have led to their widespread adoption in various settings, including hospitals, clinics, and even home care, with 68,000 healthcare facilities globally implementing POCT programs in 2024, a significant increase from 42,000 in 2020. The integration of artificial intelligence with respiratory diagnostics presents unprecedented opportunities for enhanced accuracy and efficiency. AI algorithms demonstrate remarkable potential in respiratory diagnostics through image recognition and machine learning, showing high accuracy in diagnosing respiratory conditions from medical images such as chest X-rays or CT scans. Research indicates that AI-driven diagnostic approaches can improve diagnostic speed by 30-40%, allowing healthcare professionals to make faster, more informed decisions.

Challenges: Point-of-Care Testing and AI Integration

Substantial challenge constraining the respiratory diagnostic market is the high cost associated with advanced diagnostic equipment and tests, which significantly limits accessibility, particularly in low- and middle-income countries. This financial barrier creates a multi-layered challenge that affects both healthcare providers and patients across different economic strata. Healthcare facilities face substantial capital investment requirements for advanced diagnostic technologies, with sophisticated imaging equipment, molecular diagnostic systems, and AI-powered diagnostic platforms demanding significant upfront costs that many institutions cannot afford. The challenge extends beyond initial purchase costs to include ongoing maintenance, staff training, and infrastructure requirements necessary to operate complex diagnostic equipment. Research indicates that the high cost of advanced diagnostic tests can be a barrier for healthcare facilities, especially in resource-limited settings. Reimbursement challenges compound the cost barrier, with insufficient public funding for point-of-care testing creating inequities across medical practices. In many regions, patients must pay for respiratory diagnostic tests out-of-pocket, creating significant financial barriers to access.

The global respiratory diagnostics market stands as a critical component of modern healthcare, driving the accurate identification, management, and monitoring of respiratory conditions that affect millions worldwide. Valued at approximately USD 5.3 billion in 2024, this market is poised for high growth, projected to reach over USD 7.6 billion by 2030, reflecting a CAGR of 6.3%. This expansion is fundamentally fuelled by the escalating global prevalence of respiratory diseases, a trend starkly highlighted by factors like pervasive air pollution affecting 99% of the global population – and an aging demographic that places higher individuals at greater risk, creating an urgent need for advanced diagnostic solutions. Significant opportunities emerge from technological breakthroughs such as point-of-care (POC) testing and artificial intelligence (AI) integration, which are revolutionizing diagnostic accessibility and precision.

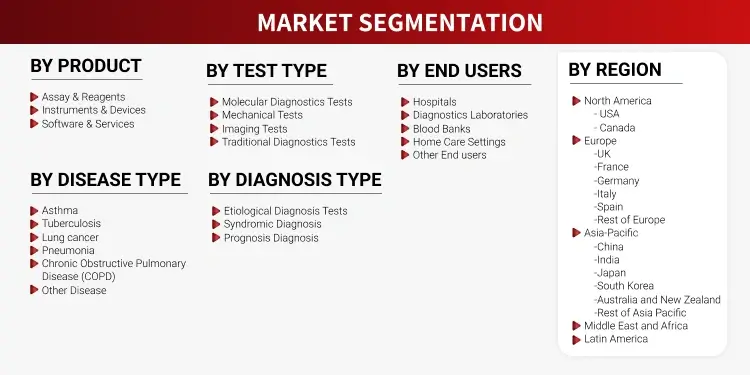

Mechanical tests dominated the Respiratory market by test type in 2024.

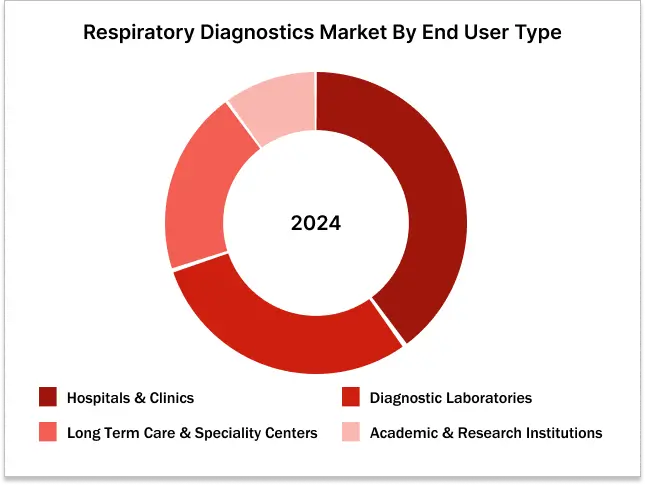

Hospitals and Clinics held the largest share in the respiratory diagnostics market by end user in 2024.

Asia Pacific will show the highest growth rate in the respiratory market in the forecast period. (2025-2030)

The respiratory diagnostics market in the Asia Pacific region is set to grow the fastest globally during the forecast period. This rapid growth is driven by several factors, including a rising burden of respiratory diseases due to urbanization, industrialization, and increasing pollution in major economies like China and India. Alongside this health issue, the aging population is more likely to suffer from chronic respiratory conditions. Governments in the region are investing in healthcare infrastructure and improving access to diagnostic services, often with expanded insurance coverage. There is a significant rise in both public and clinical awareness of the importance of early and accurate diagnosis for conditions like asthma, COPD, and various infectious respiratory illnesses. The region is also quickly adopting new diagnostic technologies, such as advanced molecular testing platforms and better pulmonary function testing equipment.

Additionally, Asia Pacific’s large and diverse population makes it an attractive area for global pharmaceutical and diagnostics companies to carry out research, development, and clinical trials, which drives innovation and market entry. Strong government initiatives aimed at enhancing public health programs, strengthening national healthcare systems, and promoting international diagnostic standards are crucial. Support from international organizations, along with increased participation in global health collaborations, is also helping build the region’s diagnostic capacity. These opportunities are encouraging investments, the establishment of local manufacturing capabilities, and the introduction of innovative respiratory diagnostic solutions tailored to the region’s needs, leading to significant market growth in Asia Pacific.

BRAND ANALYSIS: RESPIRATORY DIAGNOSTICS SPIROMETERS

“Next-generation imaging techniques, such as quantitative CT analysis and hyperpolarized gas MRI, are offering unprecedented insights into lung structure and function at a microstructural level, allowing for earlier detection of subtle lung disease.”Director of Pulmonary Research – Academic Medical Center (North America)“Advances in rapid molecular diagnostics, particularly multiplexed PCR and CRISPR-based assays, are significantly shortening the time-to-result for identifying respiratory pathogens like influenza and RSV at the point-of-care, enabling earlier initiation of targeted antiviral therapies and reducing unnecessary antibiotic use..”Head of Infectious Disease Diagnostics – Hospital Network (Europe)“Integrating digital biomarkers derived from wearable sensors and digital health apps with traditional spirometry data is providing a more comprehensive and real-time picture of asthma and COPD control, facilitating proactive management and reducing exacerbations through continuous monitoring.”Chief Medical Information Officer – Digital Health Company (Asia-Pacific)“The increasing adoption of liquid biopsy technologies, analyzing cell-free DNA or exosomes in blood samples for non-invasive monitoring, is revolutionizing the management of lung cancer by enabling frequent assessment of treatment response.”Vice President of Oncology Diagnostics – In Vitro Diagnostics Company (Europe)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. RESPIRATORY DIAGNOSTICS MARKET: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. REGULATORY SCENARIO & TRENDS

4.5. NEED GAP ANALYSIS

4.6. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.7. CASE STUDY ANALYSIS

4.8. TECHNOLOGY ANALYSIS

4.9. TRADE ANALYSIS

4.10. INDUSTRY TRENDS

4.11. PRICING ANALYSIS

4.12. REIMBURSEMENT SCENARIO

4.13. USE OF AI IN RESPIRATORY DIAGNOSTICS DEVICE

4.14. PORTER’S FIVE FORCES ANALYSIS

4.15. REGULATORY LANDSCAPE

4.15.1. NORTH AMERICA

4.15.2. EUROPE

4.15.3. ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. GLOBAL RESPIRATORY DIAGNOSTICS MARKET, BY PRODUCT TYPE (2024-2030, USD MILLION)

6.1. ASSAY & REAGENTS

6.2. INSTRUMENTS & DEVICES

6.3. SOFTWARE & SERVICES

7. GLOBAL RESPIRATORY DIAGNOSTICS MARKET, BY DISEASE TYPE (2024-2030, USD MILLION)

7.1. ASTHMA

7.2. TUBERCULOSIS

7.3. LUNG CANCER

7.4. PNEUMONIA

7.5. CHRONIC OBSTRUCTIVE PULMONARY DISEASE (COPD)

7.6. OTHER DISEASE

8. GLOBAL RESPIRATORY DIAGNOSTICS MARKET, BY TEST TYPE (2024-2030, USD MILLION)

8.1. MOLECULAR DIAGNOSTICS TESTS

8.1.1.POLYMERASE CHAIN REACTION (PCR)

8.1.2.NUCLEIC ACID AMPLIFICATION TESTS (NAAT)

8.1.3.IN SITU HYBRIDIZATION (ISH)

8.1.4.DNA SEQUENCING & NEXT GENERATION SEQUENCING

8.1.5.MICROARRAYS

8.1.6.OTHER MOLECULAR DIAGNOSTICS TESTS

8.2. MECHANICAL TESTS

8.2.1.OBSTRUCTIVE SLEEP APNEA DIAGNOSTICS TESTS

8.2.2.PULMONARY FUNCTION TESTS

8.2.3.OTHER MECHANICAL TESTS

8.3. IMAGING TESTS

8.3.1.X-RAY

8.3.2.MAGNETIC RESONANCE IMAGING (MRI)

8.3.3.COMPUTED TOMOGRAPHY

8.3.4.POSITRON EMISSION TOMOGRAPHY (PET)

8.3.5.OTHER IMAGING TESTS

8.4. TRADITIONAL DIAGNOSTICS TESTS

8.4.1.IMMUNODIAGNOSTICS

8.4.2.MICROSCOPY

8.4.3.BIOCHEMICAL TESTS

9. GLOBAL RESPIRATORY DIAGNOSTICS MARKET, BY DIAGNOSIS TYPE (2024-2030, USD MILLION)

9.1. ETIOLOGICAL DIAGNOSIS TESTS

9.2. SYNDROMIC DIAGNOSIS

9.3. PROGNOSIS DIAGNOSIS

10. GLOBAL RESPIRATORY DIAGNOSTICS MARKET, BY END USERS TYPE (2024-2030, USD MILLION)

10.1. DIAGNOSTIC LABORATORIES

10.2. HOSPITALS & CLINICS

10.3. ACADEMIC & RESEARCH INSTITUTIONS

10.4. LONG TERM CARE & SPECIALTY CENTERS

11. GLOBAL RESPIRATORY DIAGNOSTICS MARKET, BY REGION (2024-2030, USD MILLION)

11.1. NORTH AMERICA

11.1.1. US

11.1.2. CANADA

11.2. EUROPE

11.2.1. GERMANY

11.2.2. FRANCE

11.2.3. SPAIN

11.2.4. ITALY

11.2.5. UK

11.2.6. REST OF THE EUROPE

11.3. ASIA-PACIFIC

11.3.1. CHINA

11.3.2. JAPAN

11.3.3. INDIA

11.3.4. AUSTRALIA AND NEW ZEALAND

11.3.5. SOUTH KOREA

11.3.6. REST OF THE ASIA-PACIFIC

11.4. MIDDLE EAST AND AFRICA

11.5. LATIN AMERICA

12. COMPETITIVE ANALYSIS

12.1. KEY PLAYERS FOOTPRINT ANALYSIS

12.2. MARKET SHARE ANALYSIS (2023/2024)

12.3. REGIONAL SNAPSHOT OF KEY PLAYERS

12.4. R&D EXPENDITURE OF KEY PLAYERS

13. COMPANY PROFILES

13.1. KONINKLIJKE PHILIPS N.V. [NETHERLANDS]

13.1.1. BUSINESS OVERVIEW

13.1.2. PRODUCT PORTFOLIO

13.1.3. FINANCIAL SNAPSHOT

13.1.4. RECENT DEVELOPMENTS

13.1.4.1. MERGER/ACQUISITIONS

13.1.4.2. PRODUCT APPROVAL/LAUNCHES

13.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

13.2. BECTON, DICKINSON AND COMPANY (BD) [US]

13.3. ABBOTT LABORATORIES [US]

13.4. THERMO FISHER SCIENTIFIC INC. [US]

13.5. GE HEALTHCARE TECHNOLOGIES INC. [US]

13.6. BIO-RAD LABORATORIES, INC. [US]

13.7. BIOMÉRIEUX [FRANCE]

13.8. REVVITY, INC. [US]

13.9. SEEGENE INC. [SOUTH KOREA]

13.10. NIHON KOHDEN CORPORATION [JAPAN]

13.11. VITALOGRAPH [IRELAND]

13.12. SDI DIAGNOSTICS [US]

13.13. RESMED INC. [US]

13.14. SIEMENS HEALTHINEERS AG [GERMANY]

13.15. COSMED SRL [ITALY]

13.16. HOLOGIC, INC. [US]

13.17. QIAGEN N.V. [GERMANY]

13.18. OTHER PLAYERS

13.18.1. VISBY MEDICAL, INC. [US]

13.18.2. MGC DIAGNOSTICS CORPORATION [US]

13.18.3. BRIOTA TECHNOLOGIES PVT LTD [INDIA]

13.18.4. BIRD HEALTHCARE [US]

13.18.5. LOWENSTEIN MEDICAL SE & CO. KG [GERMANY]

13.18.6. PROAXSIS [US]

13.18.7. NDD MEDICAL TECHNOLOGIES [SWITZERLAND]

13.18.8. COMPUMEDICS LIMITED [AUSTRALIA]

14. APPENDIX

14.1. INDUSTRY SPEAK

14.2. QUESTIONNAIRE/DISCUSSION GUIDE

14.3. AVAILABLE CUSTOM WORK

14.4. ADJACENT STUDIES

14.5. AUTHORS.

15. REFERENCES

Market Definition: Respiratory Diagnostics

The Respiratory Diagnostics Market is an important and quickly changing part of healthcare. It focuses on the tools and technology needed to detect, diagnose, monitor, and manage various respiratory diseases like COPD, asthma, pneumonia, tuberculosis, and lung cancer. This market includes different products, such as pulmonary function testing devices like spirometers, imaging systems, molecular and microbiological tests for detecting pathogens and point-of-care testing devices. By offering key insights into lung function, gas exchange, inflammation, and the causes of respiratory illness, these diagnostics help identify conditions early and accurately. They also allow for effective disease monitoring and treatment adjustments, guide treatment plans, and support public health efforts. Overall, they play a vital role in improving patient outcomes and managing the global challenge of respiratory diseases.

FIGURE: DIAGNOSTICS ECG MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the respiratory diagnostics market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the respiratory diagnostics market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the respiratory diagnostics market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major developers offering various respiratory diagnostics will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of respiratory diagnostics market will also split into various segments and sub segments at the regional level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the respiratory diagnostics industry.