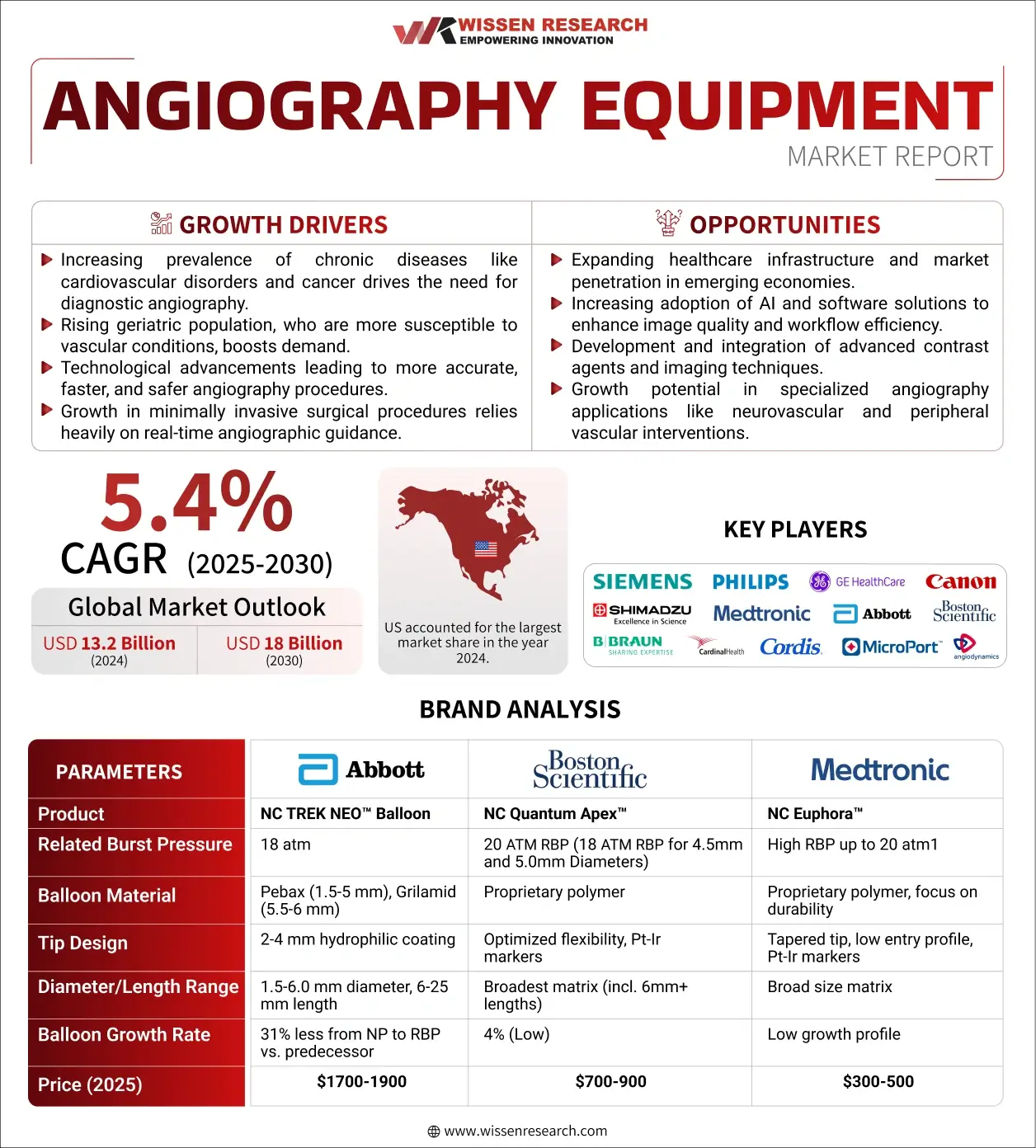

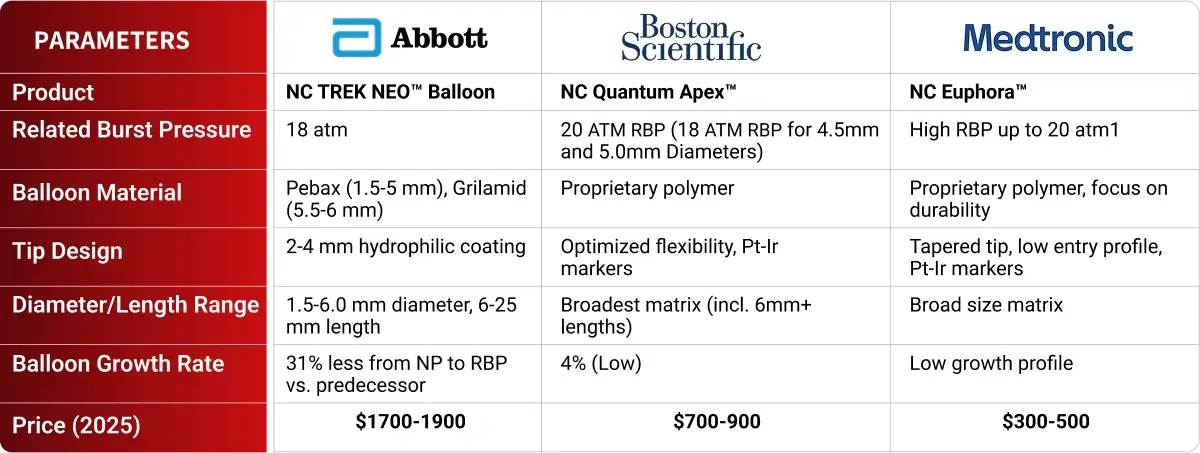

Wissen Research analyzed that the global angiography equipment market was valued at USD 13.2 billion in 2024 and is projected to reach USD 18 billion by 2030, expected to grow at a CAGR of 5.4 % during the forecast period, 2025-2030.

Lucrative Opportunities: Angiography Equipment Market

Global Angiography Equipment market is anticipated to reach USD 18 bn by 2030 from USD 13.2 bn in 2024, growing at an annualized rate of 5.4 % during the forecast period, 2025-2030 | Europe currently holds the second largest market for angiography equipment, supported by well-established healthcare systems, high awareness of cardiovascular health, strong regulatory standards ensuring high-quality equipment, and substantial investments in medical research and interventional procedures across its countries. | Asia-Pacific The Asia-Pacific region is experiencing highest growth in the hematology market, fueled by a rapidly expanding and aging population increasing the burden of hematological conditions, substantial investments in upgrading healthcare facilities and diagnostic infrastructure, and rising disposable incomes leading to greater access to advanced diagnostic services. |

Advances in angiography equipment, including higher resolution detectors, lower radiation dose technologies, and sophisticated software integration including AI for image analysis and workflow optimization, are enabling clinicians to perform complex vascular interventions more safely and accurately. | Global investment in angiography R&D is heavily focused on developing more integrated and intelligent systems, enhancing image quality while minimizing radiation exposure, advancing flat-panel VC (Vascular C-arm) technology for peripheral and emergency use, and integrating AI for procedural guidance and efficiency. These advancements aim to improve patient outcomes through less invasive treatments, enable more precise interventions, support complex cases like neurovascular procedures, and streamline workflows in hybrid operating rooms. |

Strategic Activities

Drivers: Rising Cardiovascular Disease Prevalence

The most significant and persistent driver fuelling the angiography equipment market is the relentless global escalation of cardiovascular diseases (CVDs). These conditions, encompassing coronary artery disease, stroke, peripheral artery disease, and others, remain unequivocally the leading causes of mortality worldwide. Data from the World Health Organization underscores this stark reality, reporting approximately 17.9 million CVD-related deaths annually, which translates to roughly 32% of all global deaths. This represents an urgent and continuously expanding need for effective diagnostic solutions capable of identifying and managing these life-threatening conditions promptly. The burden is particularly pronounced in developed nations; for instance, the American Heart Association highlights that nearly half of all adults in the United States live with at least one form of CVD, fuelling unprecedented demand for advanced medical imaging tools, including angiography equipment. Hospitals and specialized cardiac centers worldwide now routinely rely on angiography as the gold standard for diagnosing blocked or narrowed arteries. This equipment provides rapid, high-resolution visualization of blood vessels, enabling physicians to pinpoint blockages with remarkable accuracy.

Opportunities: Hybrid Operating Rooms & Technological Innovation

Among the most promising opportunities poised to drive significant growth in the angiography equipment market is the burgeoning integration of hybrid operating rooms (ORs) and the relentless pace of technological innovation within digital imaging technologies. Hybrid ORs represent a transformative convergence of surgical environments and high-end imaging capabilities, creating versatile spaces where clinicians can perform complex, minimally invasive diagnostic procedures and therapeutic interventions with unprecedented precision and speed within a single setting. This integration eliminates the need to move critically ill patients between different locations for imaging and surgery, reducing potential risks and streamlining care pathways. For instance, the Cleveland Clinic has strategically invested in multiple hybrid ORs equipped with state-of-the-art real-time angiography units, enabling seamless and immediate transitions from diagnostic angiography to complex interventions like stent placements or aneurysm coiling, particularly vital in cardiac and neurosurgical emergencies. The adoption of such integrated environments has demonstrably driven improvements in patient outcomes, characterized by reduced procedural times, lower rates of post-procedural complications, and significantly faster patient recoveries and hospital discharges. A concrete example from 2024 highlights this benefit: a leading hospital in Singapore reported a substantial 30% reduction in overall hospital stays for patients treated using hybrid ORs that were specifically installed with advanced angiography equipment, underscoring the efficiency gains.

Challenges: High Equipment Costs and Skill Shortages

The most formidable challenge constraining the angiography equipment market is the substantial financial burden associated with acquiring, installing, and maintaining these advanced imaging systems. The initial capital expenditure for a modern digital angiography suite is exceptionally high; the total cost, encompassing the imaging table hardware, sophisticated software, necessary radiation shielding infrastructure, and dedicated post-processing workstations, can easily exceed $500,000, and sometimes reach well over a million dollars depending on the system’s complexity and features. This significant upfront cost acts as a major financial barrier, effectively excluding many small and mid-sized hospitals, particularly those located in developing nations and underserved rural regions where healthcare budgets are often constrained. Consistently, public health officials and administrators in regions like India and Southeast Asia report significant delays in facility upgrades and new equipment purchases due to the prohibitive expense of expensive imaging equipment like angiography systems. A concrete example from 2024 illustrates this challenge: a prominent hospital located outside São Paulo, Brazil, was forced to postpone an essential angiography lab renovation for over a year, citing severe budgetary constraints as the primary reason. This delay necessitated that patients requiring essential cardiovascular diagnostics travel long distances to city hospitals, potentially compromising timely care.

The angiography equipment market stands as a critical pillar within the global medical imaging landscape, specializing in the visualization of blood vessels and the diagnosis and treatment of cardiovascular and related neurological conditions. This market is fundamental to modern interventional cardiology, radiology, and vascular surgery, enabling both precise diagnostics and minimally invasive therapeutic procedures. Valued at USD 13.2 billion in 2024, the angiography equipment market is projected to reach around USD 18 billion by 2030, reflecting a CGAR of 5.4% during the forecast period. This significant expansion is driven by the escalating global burden of cardiovascular diseases (CVDs), including coronary artery disease, stroke, and peripheral artery disease, which necessitate advanced diagnostic and interventional capabilities. Continuous technological advancements are pivotal, featuring the development of high-resolution flat-panel detectors, advanced digital subtraction angiography (DSA), and the integration of artificial intelligence (AI) for enhanced image analysis, workflow optimization, and procedural guidance.

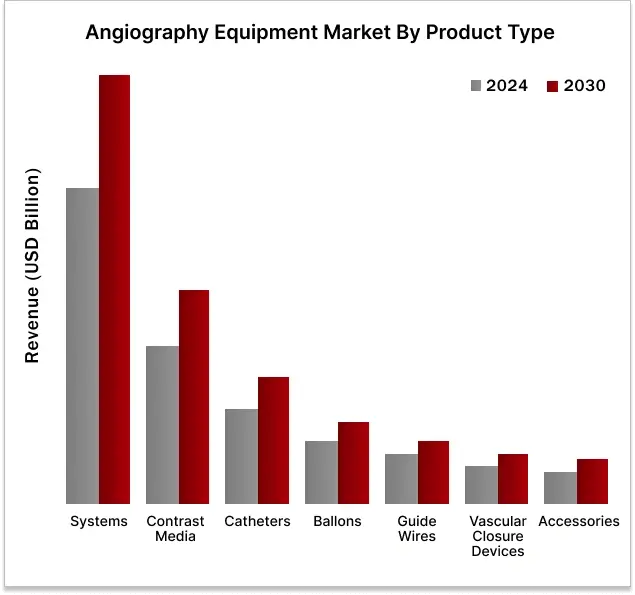

Systems by Angiography product type dominated the market in 2024

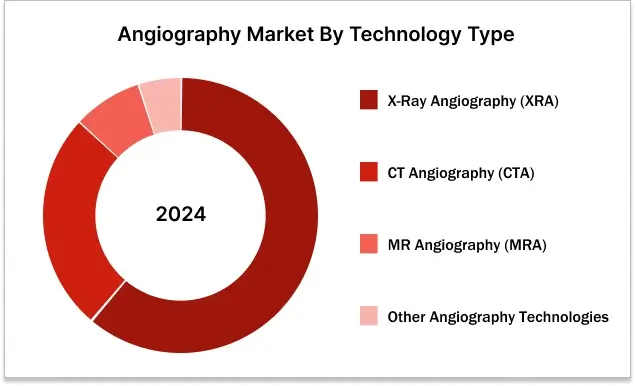

X-Ray by technology type held the largest share in the angiography market in 2024.

Asia Pacific will show the highest growth rate in the angiography market in the forecast period (2025-2030)

The angiography equipment market is poised for the most significant growth rate in the Asia Pacific region during the forecast period (2025-2030), driven by a powerful confluence of demographic, economic, and healthcare-related factors unique to the region. Key drivers fueling this expansion include the rapidly growing and aging populations across major economies, such as China, India, and Southeast Asian nations. This demographic shift inherently increases the prevalence of cardiovascular diseases (CVDs) and stroke, the primary indications for angiography, thereby boosting the demand for diagnostic imaging and interventional procedures. Concurrently, there is a significant rise in disposable incomes and increasing healthcare expenditure, leading to greater public and private investment in healthcare infrastructure, including the establishment and upgrade of hospitals and cardiac centres equipped with advanced angiography suites.

Furthermore, the burgeoning medical tourism sector within several Asia Pacific countries, coupled with the increasing adoption of minimally invasive surgical techniques, is driving demand for state-of-the-art angiography equipment. This includes not only cardiac angiography but also its expanding applications in neurovascular interventions, peripheral vascular disease management, and oncology (e.g., tumour embolization). The region is also witnessing a heightened focus on improving healthcare access and quality, particularly in underserved areas. Rising regulatory standards and proactive government initiatives aimed at strengthening healthcare systems, establishing national cardiac programs, and enhancing emergency medical services are driving the adoption of modern diagnostic and interventional technologies, including advanced angiography systems. Additionally, significant foreign direct investment (FDI) and the establishment of manufacturing hubs and regional headquarters for global medical device companies in the Asia Pacific further stimulate market growth through technology transfer, localized production, and aggressive market expansion efforts, making angiography equipment the fastest-growing segment globally.

“The angiography market is seeing a significant push towards hybrid operating rooms where diagnosis and treatment happen seamlessly. This convergence allows for more complex, efficient procedures and reduces patient transfers.”Director of Cardiovascular Services, Large Academic Medical Centre (North America)“Radiation safety and image quality are paramount; hospitals increasingly prioritize systems offering high resolution at the lowest possible dose. Advanced detector tech and dose-reduction software are now key selling points.”Interventional Radiologist, Tertiary Care Hospital (Europe)“We’re observing strong growth in portable/mobile angiography units, bringing vascular imaging capabilities directly to patients in emergency and surgical settings. This enables faster decision-making outside traditional Cath labs.”Head of Medical Imaging Strategy, Healthcare Consulting Firm (Asia-Pacific)“AI integration is rapidly transforming angiography, automating tasks like vessel analysis and dose optimization. This boosts procedural efficiency and accuracy for clinicians.”Senior Product Manager – Angiography, Major Medical Device Manufacturer (Latin-America)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. ANGIOGRAPHY EQUIPMENT MARKET: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. REGULATORY SCENARIO & TRENDS

4.5. NEED GAP ANALYSIS

4.6. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.7. REIMBURSEMENT SCENARIO

4.8. TRADE ANALYSIS

4.9. INDUSTRY TRENDS

4.10. TECHNOLOGIES ANALYSIS

4.11. USE OF AI IN ANGIOGRAPHY EQUIPMENT MARKET

4.12. PORTER’S FIVE FORCES ANALYSIS

4.13. REGULATORY LANDSCAPE

4.13.1. NORTH AMERICA

4.13.2. EUROPE

4.13.3. ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. GLOBAL ANGIOGRAPHY EQUIPMENT MARKET, BY PRODUCT TYPE (2024-2030, USD MILLION)

6.1. ANGIOGRAPHY SYSTEMS

6.2. ANGIOGRAPHY CATHETERS

6.3. ANGIOGRAPHY GUIDEWIRE

6.4. ANGIOGRAPHY BALLOONS

6.5. ANGIOGRAPHY CONTRAST MEDIA

6.6. VASCULAR CLOSURE DEVICES

6.7. ANGIOGRAPHY ACCESSORIES

7. GLOBAL ANGIOGRAPHY EQUIPMENT MARKET, BY PROCEDURE TYPE (2024-2030, USD MILLION)

7.1. ENDOVASCULAR ANGIOGRAPHY

7.2. CORONARY ANGIOGRAPHY

7.3. NEUROANGIOGRAPHY

7.4. ONCO-ANGIOGRAPHY

7.5. OTHER ANGIOGRAPHY PROCEDURES

8. GLOBAL ANGIOGRAPHY EQUIPMENT MARKET, BY TECHNOLOGY TYPE (2024-2030, USD MILLION)

8.1. CT ANGIOGRAPHY

8.2. MR ANGIOGRAPHY

8.3. X-RAY ANGIOGRAPHY

8.4. OTHER ANGIOGRAPHY TECHNOLOGIES

9. GLOBAL ANGIOGRAPHY EQUIPMENT MARKET, BY DISEASE TYPE (2024-2030, USD MILLION)

9.1. VALVULAR HEART DISEASE

9.2. CONGENITAL HEART DISEASE

9.3. CONGESTIVE HEART DISEASE

9.4. CORONARY ARTERY DISEASE

9.5. OTHER DISEASE

10. GLOBAL ANGIOGRAPHY EQUIPMENT MARKET, BY APPLICATION TYPE (2024-2030, USD MILLION)

10.1. THERAPEUTICS

10.2. DIAGNOSTICS

11. GLOBAL ANGIOGRAPHY EQUIPMENT MARKET, BY END USER TYPE (2024-2030, USD MILLION)

11.1. HOSPITAL & CLINICS

11.2. RESEARCH INSTITUTES

11.3. DIAGNOSTICS & IMAGING CENTER

12. GLOBAL ANGIOGRAPHY EQUIPMENT MARKET, BY REGION (2024-2030, USD MILLION)

12.1. NORTH AMERICA

12.1.1. US

12.1.2. CANADA

12.2. EUROPE

12.2.1. GERMANY

12.2.2. FRANCE

12.2.3. SPAIN

12.2.4. ITALY

12.2.5. UK

12.2.6. REST OF THE EUROPE

12.3. ASIA-PACIFIC

12.3.1. CHINA

12.3.2. JAPAN

12.3.3. INDIA

12.3.4. AUSTRALIA AND NEW ZEALAND

12.3.5. SOUTH KOREA

12.3.6. REST OF THE ASIA-PACIFIC

12.4. MIDDLE EAST AND AFRICA

12.5. LATIN AMERICA

13. COMPETITIVE ANALYSIS

13.1. PRODUCT PIPELINE: ANGIOGRAPHY EQUIPMENT

13.2. KEY PLAYERS FOOTPRINT ANALYSIS

13.3. MARKET SHARE ANALYSIS (2023/2024)

13.4. REGIONAL SNAPSHOT OF KEY PLAYERS

13.5. R&D EXPENDITURE OF KEY PLAYERS

14. COMPANY PROFILES

14.1. SIEMENS HEALTHINEERS AG (GERMANY)

14.1.1. BUSINESS OVERVIEW

14.1.2. PRODUCT PORTFOLIO

14.1.3. FINANCIAL SNAPSHOT

14.1.4. RECENT DEVELOPMENTS

14.1.4.1. MERGER/ACQUISITIONS

14.1.4.2. PRODUCT APPROVAL/LAUNCHES

14.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

14.2. KONINKLIJKE PHILIPS N.V. (NETHERLAND)

14.3. GE HEALTHCARE (US)

14.4. SHIMADZU CORPORATION (JAPAN)

14.5. CANON CORPORATION (JAPAN)

14.7. BOSTON SCIENTIFIC CORPORATION (US)

14.8. ABBOTT LABORATORIES (US)

14.9. MICROPORT SCIENTIFIC CORPORATION (CHINA)

14.10. B. BRAUN SE (GERMANY)

14.11. CARDINAL HEALTH, INC. (US)

14.12. CORDIS CORPORATION (US)

14.13. ANGIODYNAMICS (US)

15. APPENDIX

15.1. INDUSTRY SPEAK

15.2. QUESTIONNAIRE/DISCUSSION GUIDE

15.3. AVAILABLE CUSTOM WORK

15.4. ADJACENT STUDIES

15.5. AUTHORS

16. REFERENCES

Market Definition: Angiography Market

The angiography market represents a critical and high-value segment within the broader medical imaging and interventional cardiology/peripheral vascular disease market. It focuses on visualizing the inside of blood vessels and organs using imaging techniques, primarily to diagnose blockages, aneurysms, and other cardiovascular or neurological conditions, and to guide minimally invasive therapeutic procedures. This market encompasses imaging systems (like C-arm fluoroscopy units and flat-panel detectors), contrast media, guidewires, catheters, balloons, stents, vascular closure devices, and various accessories essential for both diagnostic imaging and interventional treatments.

These analytical and interventional techniques provide essential real-time visualization of blood flow and vessel anatomy. Angiography methods typically involve the injection of a radiopaque contrast agent into the bloodstream, followed by imaging using X-rays (fluoroscopy or angiography) to highlight the vascular structure. This enables the assessment of arterial and venous patency, identification of stenosis, aneurysms, or malformations, and facilitates minimally invasive interventions such as angioplasty, stenting, thrombectomy, and embolization.

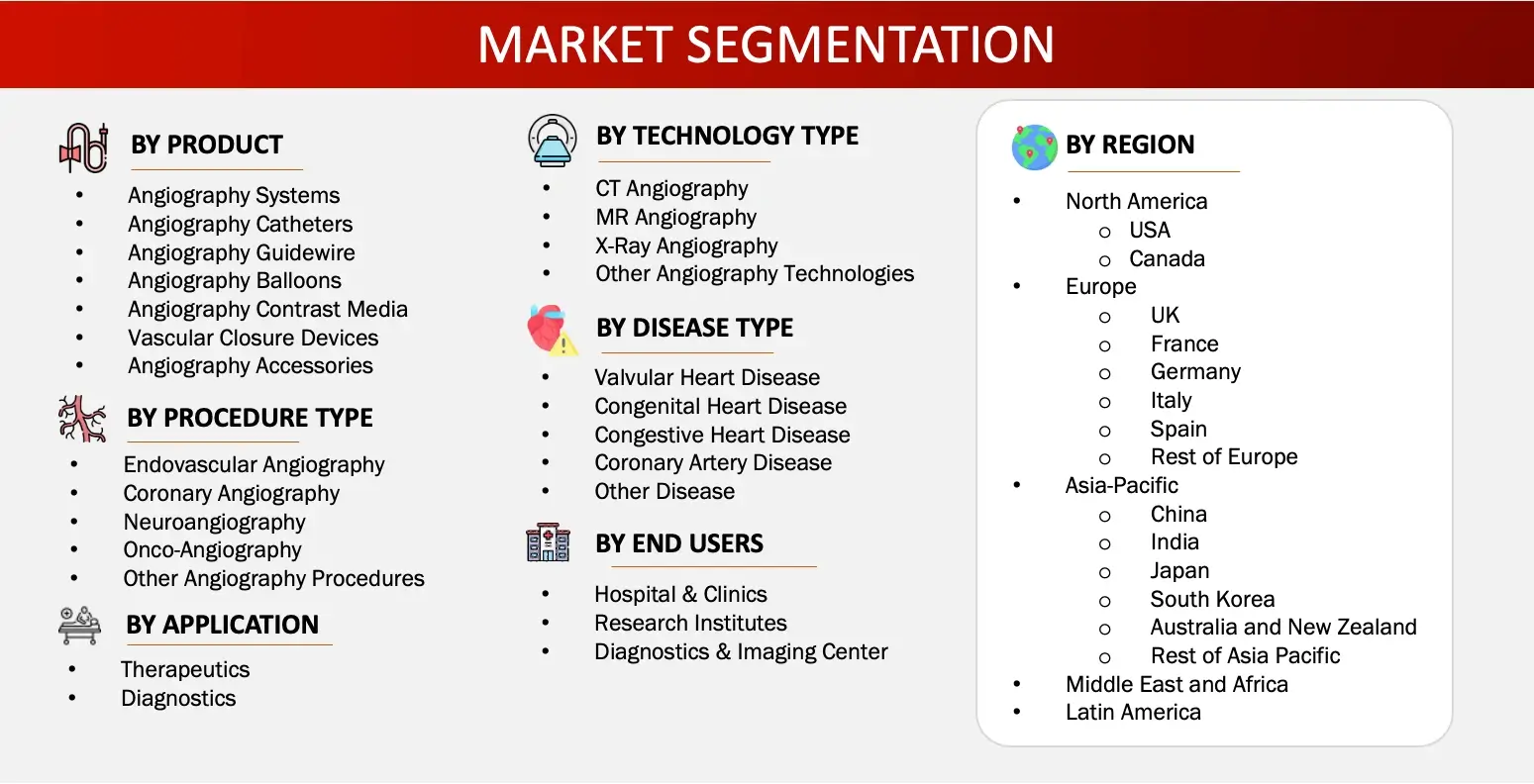

FIGURE: ANGIOGRAPHY EQUIPMENT MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the angiography equipment market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the angiography equipment market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the angiography equipment market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major developers offering various angiography equipment will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of angiography equipment market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the angiography equipment industry.