Wissen Research analyzed that the global CAR-T cell (Chimeric Antigen Receptor-T Cell Therapy) market was valued at USD 5.2 billion in 2024 and is projected to reach USD 26.2 billion by 2030, expected to grow at a CAGR of 31% during the forecast period, 2025-2030.

Lucrative Opportunities: CAR-T Cell Therapy Market

Global CAR T-cell therapy market is anticipated to reach USD 26.2 billion by 2030 from USD 5.2 billion in 2024, growing at an annualized rate of 31% during the forecast period, 2025-2030 | Europe’s CAR T-cell therapy market is experiencing steady growth, driven by the increasing incidence of hematologic malignancies, particularly among aging populations, and the gradual adoption of these novel therapies following regulatory approvals. The region benefits from strong academic research centers, significant investments in oncology, and a presence of key developers, fostering the integration of CAR T-cell therapy into specialized cancer centers across countries like Germany, the UK, and France. | Asia-Pacific The Asia-Pacific CAR T-cell therapy market fueled by a large patient population, increasing investment in oncology research and biotechnology, and growing capabilities in specialized cancer care and active clinical trial activity, with countries like China, South Korea, and Japan playing increasingly prominent roles in both development and market adoption. |

The CAR T-cell therapy market is undergoing significant transformation, propelled by a growing demand for effective treatments for patients with relapsed or refractory hematologic malignancies where conventional therapies offer limited options | Global investment in the CAR T-cell therapy sector is heavily focused on overcoming major challenges, including the high cost and complex logistics of manufacturing, managing severe toxicities like Cytokine Release Syndrome and neurotoxicity, and expanding the applicability of the therapy beyond hematologic cancers to treat solid tumors, which remains a major scientific hurdle. Research is also directed towards developing “off-the-shelf” allogeneic CAR T products to reduce costs and turnaround times. |

Strategic Activities Within the CAR-T Cell Therapy Market

Drivers: Escalating Global Cancer Prevalence and Unmet Need

The most compelling driver for the CAR T-cell therapy market is the relentlessly escalating global burden of cancer, creating an immense and growing unmet medical need, particularly for advanced therapies targeting hematological malignancies where CAR T has shown efficacy. This is powerfully validated by the latest IARC estimates for 2022, which reveal a staggering 20 million new cancer cases and 9.7 million deaths worldwide according to WHO 2024 report. The sheer scale of this burden is further underscored by the statistic that approximately 1 in 5 individuals will develop cancer during their lifetime. While lung cancer remains the most common cancer globally (2.5 million cases, 12.4%), breast cancer (2.3 million cases, 11.6%) has emerged as the leading cancer type for women in the vast majority of countries (157 of 185). This highlights the widespread nature of the challenge. Looking ahead, the projected increase is alarming; over 35 million new cancer cases are expected by 2050, representing a 77% rise from 2022, driven by population growth, aging, and increasing exposure to risk factors like tobacco, alcohol, and obesity. This profound and expanding unmet need for effective treatments, especially for aggressive cancers where standard therapies fail, provides a powerful impetus for the development, approval, and adoption of innovative therapies like CAR T-cell therapy, particularly in regions where access to advanced care remains limited.

Opportunities: Process Automation and AI Integration

Significant opportunity lies in revolutionizing CAR T-cell manufacturing through the integration of artificial intelligence (AI) and advanced automation technologies. Current manufacturing processes are complex, labor-intensive, and prone to variability, contributing significantly to the high cost and limited scalability of these therapies. Implementing AI for real-time process control, quality monitoring, and predictive analytics can dramatically reduce human error, enhance production speed, and ensure batch-to-batch consistency. Automation can streamline critical steps, from cell collection and expansion to final product formulation, potentially enabling remote oversight and decentralization of production. Furthermore, integrating smart wearables and digital health tools, powered by AI, allows for continuous, real-time patient monitoring post-infusion, facilitating early detection of adverse events like cytokine release syndrome (CRS) and neurotoxicity. This not only improves patient safety and clinical outcomes but also paves the way for more personalized treatment adjustments, ultimately reducing costs and expanding market access to geographies currently underserved by specialized centers.

Challenges: High Cost & Global Accessibility

The most formidable challenge confronting the CAR T-cell therapy market is the exceptionally high cost associated with treatments and the resulting barriers to global accessibility. The price tag for a single course of CAR T-cell therapy remains staggering, often ranging between $373,000 and $475,000 in the United States. This cost frequently exceeds the annual Gross Domestic Product (GDP) per capita in both developed and, more significantly, developing nations, making these therapies financially prohibitive for many healthcare systems and patients. Accessibility is further hindered by complex logistical requirements, including lengthy “vein-to-vein” times (the period from blood collection to infusion) and the necessity for specialized treatment centers equipped with manufacturing capabilities and experienced clinical teams. These centers are concentrated primarily in North America and Western Europe, leaving vast populations globally without access. Patients also face significant indirect costs related to travel, extended hospital stays, and supportive care. While strategies like on-site manufacturing and local production are being explored to mitigate costs, the substantial investments in facility setup, specialized labor, and comprehensive post-treatment support remain major obstacles to widespread adoption and equitable access.

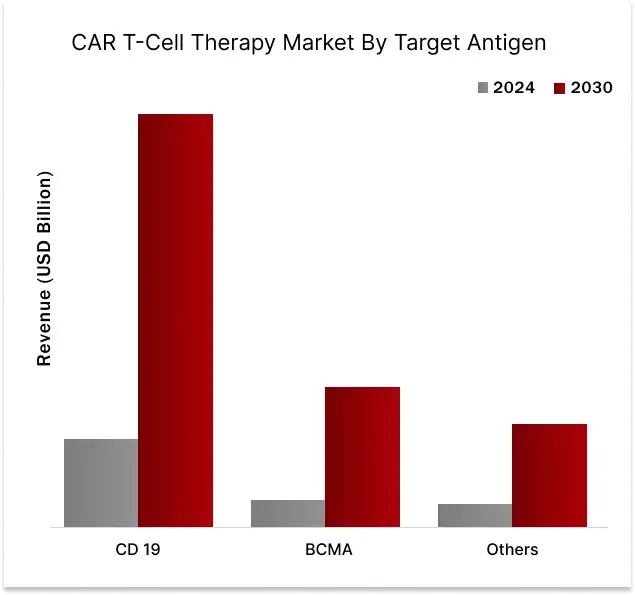

CD19 by target antigen dominated the CAR T-Cell therapy market in the year 2024

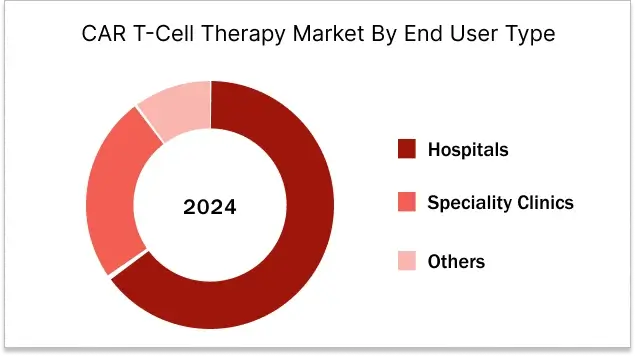

Hospitals held the largest market share by end user type in CAR-T cell therapy market in the year 2024.

Furthermore, the requirement for intensive patient monitoring both before and after infusion, along with the need for immediate access to critical care, aligns perfectly with the comprehensive inpatient and specialized outpatient services provided by hospitals. This concentration of necessary resources and capabilities makes hospitals the primary and most logical setting for CAR T-cell therapy administration, solidifying their dominant position as the leading end-user type.

Asia Pacific will show the highest growth rate in the CAR-T cell therapy market in the forecast period. (2025-2030)

This is driven by a confluence of demographic, economic, and healthcare infrastructure factors. A primary driver is the significantly larger patient population suffering from hematological malignancies and solid tumours across countries like China, India, and Japan, creating a vast unmet medical need that CAR T-cell therapies can address. Concurrently, substantial investments are being made by both governments and private entities to enhance healthcare infrastructure, including the establishment of advanced oncology centers and biotechnology hubs equipped to develop, manufacture, and administer these complex therapies. Rising disposable incomes in developing nations are gradually increasing patient access and affordability, while growing awareness among healthcare professionals and the general population about innovative cancer treatments is fuelling demand.

Furthermore, regulatory bodies in the region, such as China’s NMPA, are actively working to streamline approval processes for cellular therapies, evidenced by the approval of Yescarta (axicabtagene ciloleucel) for relapsed or refractory large B-cell lymphoma in China in 2022, and the continued expansion of clinical trial activities. For instance, Carma Clinical Trials, a Singapore-based company specializing in cell and gene therapies, has been actively expanding its operations and trial networks across Asia, highlighting the region’s growing importance as a clinical research hub for CAR T therapies. Additionally, major global players like Novartis and Gilead Sciences (now Kite Pharma) are strategically increasing their presence and partnerships within Asia Pacific to tap into this burgeoning market, further validating the region’s high growth potential. This combination of a large patient base, improving healthcare capabilities, increasing affordability, supportive regulatory developments, and active participation from industry stakeholders’ positions Asia Pacific for the most rapid expansion in the CAR T-cell therapy market over the coming years.

“The significant cost associated with manufacturing and delivering CAR T-cell therapies, coupled with complex reimbursement landscapes, is creating financial pressures on healthcare systems and driving exploration of value-based payment models to ensure sustainable access.”

Healthcare Economist – Consulting Firm (Global)

“The ongoing development of next-generation CAR T-cell therapies targeting antigens beyond CD19, particularly for solid tumours and hematologic malignancies that relapse after CD19-targeted therapy, is expanding the potential market reach but also increasing the need for biomarker identification to predict patient response.”

Oncology Drug Development Scientist – Biotechnology Company (Europe)

“The shift towards outpatient administration for certain CAR T-cell therapies, enabled by improved understanding of toxicity management and patient selection criteria, is reducing hospital lengths of stay and costs, while presenting new operational challenges for outpatient centers.”

Hospital Administrator – Oncology Center (North America)

“The increasing incidence of hematologic malignancies combined with the growing body of evidence demonstrating durable remissions with CAR T-cell therapy is steadily improving physician confidence and prescribing patterns, albeit tempered by concerns regarding toxicities like Cytokine Release Syndrome and neurotoxicity management.”

Oncology Physician – Academic Medical Center (Asia-Pacific)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. CAR T-CELL THERAPY MARKET: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. REGULATORY SCENARIO & TRENDS

4.5. NEED GAP ANALYSIS

4.6. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.7. CASE STUDY ANALYSIS

4.8. TRADE ANALYSIS

4.9. INDUSTRY TRENDS

4.10. TECHNOLOGY ANALYSIS

4.10.1. VIRAL VECTOR TECHNOLOGY

4.10.2. CAR DESIGN AND OPTIMIZATION

4.10.3. CELL CULTURE AND EXPANSION TECHNIQUES

4.10.4. GENE EDITING TECHNOLOGY

4.11. PRICING ANALYSIS

4.12. PORTER’S FIVE FORCES ANALYSIS

4.13. REGULATORY LANDSCAPE

4.13.1. NORTH AMERICA

4.13.2. EUROPE

4.13.3. ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. CLINICAL TRIAL ANALYSIS

6.1. ANALYSIS BY TRIAL REGISTRATION YEAR

6.2. ANALYSIS BY PHASE OF DEVELOPMENT

6.3. ANALYSIS BY TRIAL STATUS

6.4. ANALYSIS BY NUMBER OF PATIENTS ENROLLED

6.5. ANALYSIS BY STUDY DESIGN

6.6. ANALYSIS BY TYPE OF THERAPY / DRUG

6.7. ANALYSIS BY GEOGRAPHY

6.8. ANALYSIS BY KEY SPONSORS / COLLABORATORS

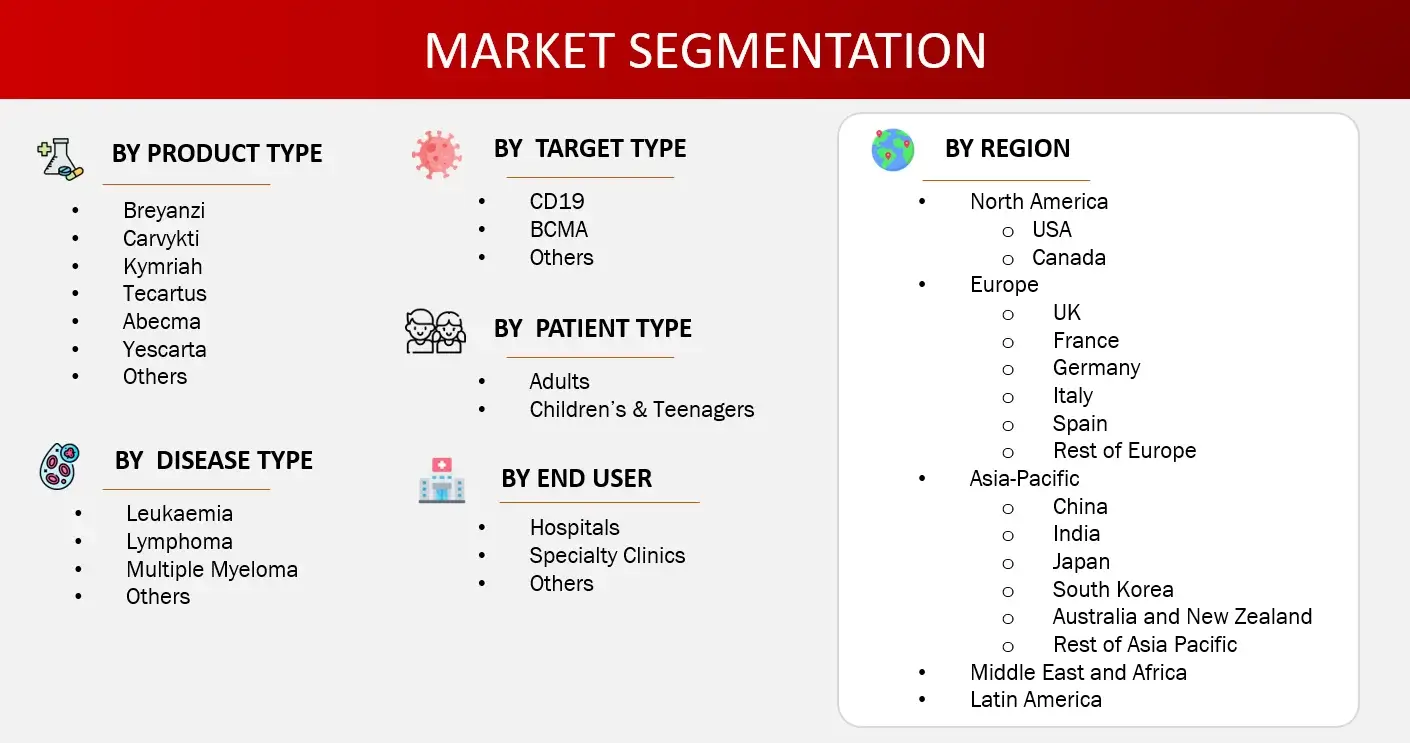

7. GLOBAL CAR T-CELL THERAPY MARKET, BY PRODUCT TYPE (2024-2030, USD MILLION)

7.1. BREYANZI

7.2. CARVYKTI

7.3. KYMRIAH

7.4. TECARTUS

7.5. ABECMA

7.6. YESCARTA

7.7. OTHERS

8. GLOBAL CAR T-CELL THERAPY MARKET, BY DISEASE TYPE (2024-2030, USD MILLION)

8.1. LEUKAEMIA

8.2. LYMPHOMA

8.3. MULTIPLE MYELOMA

8.4. OTHERS

9. GLOBAL CAR T-CELL THERAPY MARKET, BY TARGET ANTIGEN (2024-2030, USD MILLION)

9.1. CD19

9.2. BCMA

9.3. OTHERS

10. GLOBAL CAR T-CELL THERAPY MARKET, BY PATIENT TYPE (2024-2030, USD MILLION)

10.1. ADULTS

10.2. CHILDREN’S & TEENAGERS

11. GLOBAL CAR T-CELL THERAPY MARKET, BY END USERS (2024-2030, USD MILLION)

11.1. HOSPITALS

11.2. SPECIALTY CLINICS

11.3. OTHERS

12. GLOBAL CAR T-CELL THERAPY MARKET, BY REGION (2024-2030, USD MILLION)

12.1. NORTH AMERICA

12.1.1. US

12.1.2. CANADA

12.2. EUROPE

12.2.1. GERMANY

12.2.2. FRANCE

12.2.3. SPAIN

12.2.4. ITALY

12.2.5. UK

12.2.6. REST OF THE EUROPE

12.3. ASIA-PACIFIC

12.3.1. CHINA

12.3.2. JAPAN

12.3.3. INDIA

12.3.4. AUSTRALIA AND NEW ZEALAND

12.3.5. SOUTH KOREA

12.3.6. REST OF THE ASIA-PACIFIC

12.4. MIDDLE EAST AND AFRICA

12.5. LATIN AMERICA

13. COMPETITIVE ANALYSIS

13.1. PRODUCT PIPELINE: CAR T-CELL THERAPY DEVICES

13.2. KEY PLAYERS FOOTPRINT ANALYSIS

13.3. MARKET SHARE ANALYSIS (2023/2024)

13.4. REGIONAL SNAPSHOT OF KEY PLAYERS

13.5. R&D EXPENDITURE OF KEY PLAYERS

14. COMPANY PROFILES

14.1. BRISTOL-MYERS SQUIBB COMPANY (US)

14.1.1. BUSINESS OVERVIEW

14.1.2. PRODUCT PORTFOLIO

14.1.3. FINANCIAL SNAPSHOT

14.1.4. RECENT DEVELOPMENTS

14.1.4.1. MERGER/ACQUISITIONS

14.1.4.2. PRODUCT APPROVAL/LAUNCHES

14.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

14.1.4.4. EXPANSIONS

14.2. NOVARTIS AG (SWITZERLAND)

14.3. GILEAD SCIENCES, INC. (US)

14.4. JOHNSON & JOHNSON. (US)

14.5. JW THERAPEUTICS (SHANGHAI) CO., LTD. (CHINA)

14.6. BLUEBIRD BIO, INC. (US)

14.7. MERCK & CO., INC. (US)

14.8. SANGAMO THERAPEUTICS (US)

14.9. SORRENTO THERAPEUTICS, INC. (US)

14.10. GSK PLC. (UK)

14.11. IMMUNOACT PVT LTD (INDIA)

14.12. CARSGEN THERAPEUTICS HOLDINGS LTD. (CHINA)

14.13. IASO BIOTHERAPEUTICS. (CHINA)

14.14. CARTESIAN THERAPEUTICS, INC. (US)

14.15. AUTOLUS THERAPEUTICS. (UK)

14.16. ALLOGENE THERAPEUTICS. (US)

14.17. CRISPR THERAPEUTICS. (SWITZERLAND)

14.18. WUGEN. (US)

14.19. GUANGZHOU BIO-GENE TECHNOLOGY CO., LTD (CHINA)

15. APPENDIX

15.1. INDUSTRY SPEAK

15.2. QUESTIONNAIRE/DISCUSSION GUIDE

15.3. AVAILABLE CUSTOM WORK

15.4. ADJACENT STUDIES

15.5. AUTHORS.

16. REFERENCES

Market Definition: CAR-T Cell Therapy

The CAR T-Cell therapy market represents a revolutionary and rapidly evolving segment within the global biopharmaceutical and oncology landscape. This market is driven by the groundbreaking approach of engineering a patient’s own immune cells (T-cells) to specifically target and destroy cancer cells, particularly in hematologic malignancies. It encompasses the complex ecosystem surrounding the development, manufacturing, distribution, and clinical application of Chimeric Antigen Receptor (CAR) T-cell products. Key components include sophisticated biologic drugs (autologous or, increasingly, allogeneic cell therapies), advanced manufacturing technologies and facilities capable of handling personalized cell processing, specialized logistics for handling living cells, and dedicated healthcare delivery infrastructure, including specialized infusion centers and clinical staff trained in managing these therapies.

The market also involves supportive technologies like patient selection tools, genetic engineering platforms, and monitoring systems for tracking treatment response and managing potential side effects such as Cytokine Release Syndrome (CRS) and Immune Effector Cell-Associated Neurotoxicity Syndrome (ICANS). CAR T-cell therapy is fundamentally transforming the treatment paradigm for certain types of leukaemia, lymphoma, and multiple myeloma, offering durable remissions and potential cures for patients with limited or no other effective options. By providing a targeted, personalized immunotherapy approach, the CAR T-cell therapy market plays an indispensable role in offering hope to patients with aggressive blood cancers, redefining treatment standards, and paving the way for the future of cancer immunotherapy, despite challenges related to cost, manufacturing complexity, and management of severe adverse events within specialized healthcare settings.

FIGURE: CAR T-CELL THERAPY MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the CAR T-cell therapy market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the CAR T-cell therapy market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the CAR T-cell therapy market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major developers offering various CAR T-cell therapy will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of CAR T-cell therapy market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the CAR T-cell therapy industry.