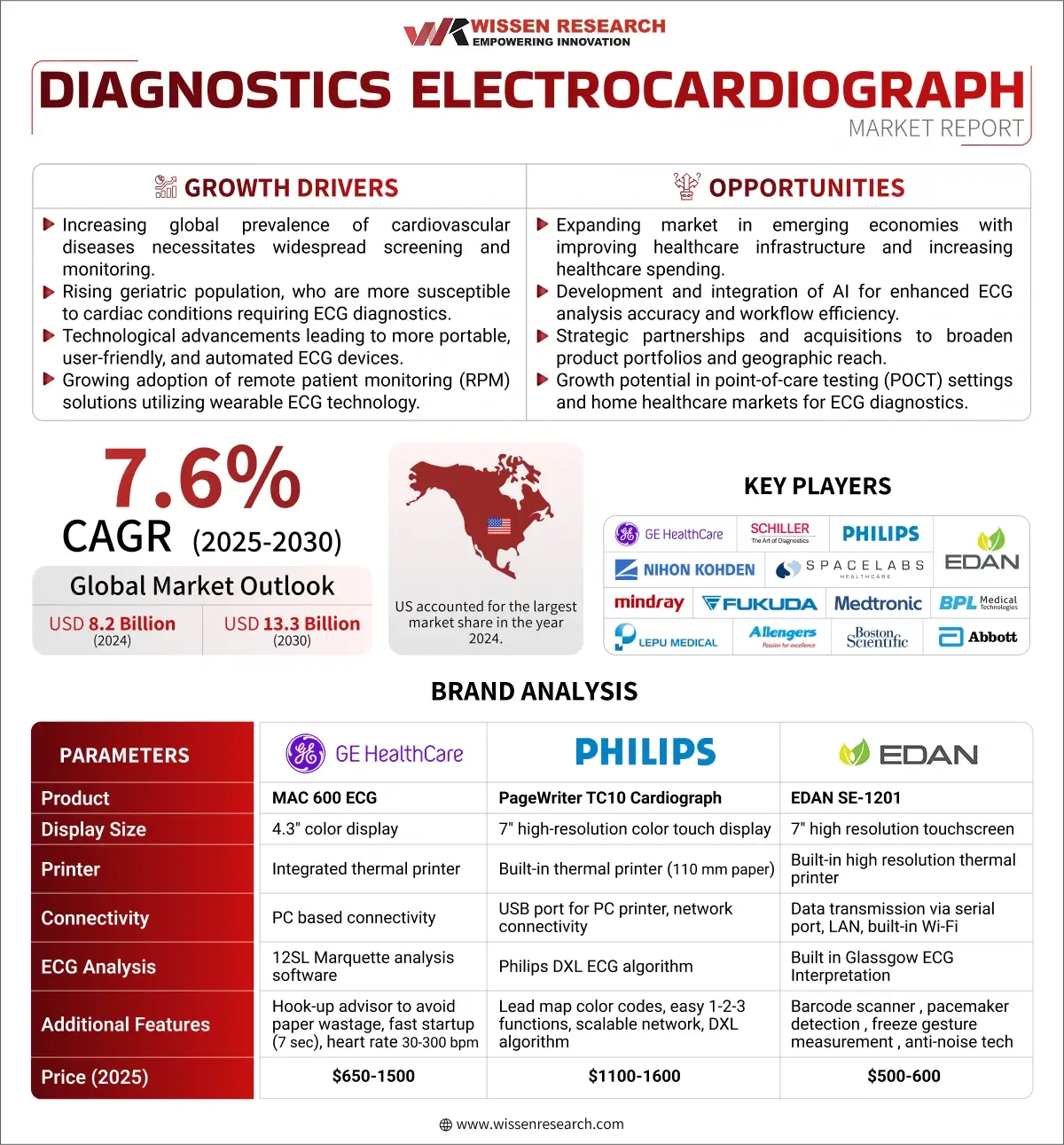

Wissen Research analyzed that the global diagnostics ECG market was valued at USD 8.2 billion in 2024 and is projected to reach USD 13.3 billion by 2030, expected to grow at a CAGR of 7.6 % during the forecast period, 2025-2030.

Lucrative Opportunities: Diagnostics ECG Market

Global diagnostics ECG market is anticipated to reach USD 13.3 billion by 2030 from USD 8.2 billion in 2024, growing at an annualized rate of 7.6% during the forecast period, 2025-2030 | Europe’s ECG market is experiencing steady growth, driven by the increasing prevalence of cardiovascular diseases and a growing geriatric population requiring continuous cardiac monitoring and management. The region also benefits from significant investments in advanced healthcare technologies and a strong presence of key ECG market players, particularly in countries like Germany, France, and the UK. | Asia-Pacific The Asia-Pacific ECG market is expanding rapidly, fueled by rising disposable incomes, growing awareness of cardiovascular health, and significant urbanization leading to increased access to healthcare services. This growth is further propelled by substantial investments in healthcare infrastructure development and a burgeoning middle class demanding better cardiac care. Countries like China, India, and Japan are key contributors to this dynamic market expansion. |

| The electrocardiography (ECG) market is undergoing significant transformation, propelled by a growing demand for high-resolution, accessible, and continuous cardiac monitoring solutions essential for precise diagnosis, risk stratification, and management of cardiovascular diseases (CVDs), which remain a leading global health burden. | Global Investment in the ECG sector are heavily focused on enhancing device connectivity, developing more compact, wearable, and user-friendly monitors, integrating advanced software for automated analysis and AI-driven interpretation, and advancing remote patient monitoring capabilities. The rapid adoption of ambulatory ECG monitoring (like Holters and event recorders) for arrhythmia detection and wearable ECG devices (including smartwatches) for continuous and consumer-friendly monitoring are key trends reshaping clinical workflows and patient care. |

Strategic Activities

Drivers: Rising Prevalence of Cardiovascular Diseases.

One major driver propelling the diagnostic ECG market is the increasing global burden of cardiovascular diseases (CVDs). CVDs remain the world’s leading cause of mortality, with approximately 17.9 million deaths annually, accounting for 32% of all deaths globally. Early detection and ongoing monitoring are crucial in managing these health risks, and diagnostic ECG devices have become fundamental in both clinical and home-care settings. Factors such as a sedentary lifestyle, aging demographics, and escalating obesity rates have led to a surge in CVD incidence, prompting greater demand for ECG systems. The rise in awareness regarding preventive healthcare and the emphasis on routine cardiac screenings have further fueled market adoption. Moreover, technological innovations—from portable ECG devices to AI-based analysis—have enhanced diagnostic convenience and accuracy, making ECG solutions essential in the push for earlier intervention and improved patient outcomes. As a result, the need for reliable, accessible, and advanced diagnostic ECG solutions is poised to grow even further with the increasing prevalence of heart-related illnesses worldwide.

Opportunities: Integration of AI and Remote Monitoring in ECG Diagnostics

A significant opportunity in the diagnostic ECG market lies in leveraging artificial intelligence (AI) and remote monitoring technologies to transform cardiac care. AI-powered ECG platforms can analyze cardiac data in real-time, identify subtle abnormalities, and alert clinicians to potential arrhythmias or ischemic events—enabling faster and more accurate decision-making. The fusion of intelligent software with wearable ECG devices allows for continuous monitoring beyond traditional care environments, expanding access for rural populations and the elderly. These technologies simplify workflows, streamline data interpretation, and utilize predictive analytics for improved outcomes. As digital healthcare adoption accelerates, especially post-pandemic, remote patient monitoring is increasingly recognized for its ability to deliver preventive care and timely interventions. Emerging markets also present vast potential, with growing investments in healthcare technology and infrastructure supporting widespread implementation of advanced ECG platforms. Companies that prioritize AI integration, user-friendly connectivity, and remote accessibility are well-positioned to capture new market share and meet changing healthcare needs.

Challenges: Lack of Data Standardization and Interoperability

Despite technological advancements, one persistent challenge for the diagnostics ECG market is the lack of standardization and interoperability in data and device integration. ECG systems from various manufacturers frequently use divergent data formats, complicating seamless exchange with electronic health records (EHRs). Legacy ECG machines may lack digital connectivity altogether, necessitating manual data entry—a process prone to errors and delays in diagnosis. Additionally, restricted real-time access and inefficient integration can hinder clinical workflows, adversely affecting patient care. These technical barriers slow the adoption of next-generation ECG diagnostics that rely on rapid data transfers and integration with broader healthcare platforms. Addressing these limitations requires concerted efforts among device makers, regulators, and healthcare institutions to establish uniform data protocols and interoperability standards. Without these improvements, the market’s growth will be restrained, particularly as demand rises for AI-powered, connected diagnostic solutions.

The global diagnostic ECG (Electrocardiography) market plays a vital role in modern healthcare by providing essential information for the diagnosis, monitoring, and management of cardiovascular diseases (CVDs). As CVDs remain a leading cause of mortality and morbidity worldwide, the accurate and timely assessment of heart function through ECG is indispensable for patient care. The market is valued at USD 8.2 billion in 2024 and is projected to grow at a steady CAGR of around 7.6%, potentially reaching over USD 13.3 billion by 2030. The market encompasses a wide range of segments, reflecting its diverse applications and technological evolution, primary segments include by product type, including resting ECG devices, ambulatory ECG devices like holters and event monitors, and stress ECG systems; by lead configuration, such as 12-lead ECG for comprehensive views, 3/5-lead ECG for critical care, and single-lead ECG for rhythm monitoring; and by end-user, encompassing hospitals, diagnostic imaging centers & laboratories, ambulatory surgical centers & clinics, home healthcare settings, and specialized cardiac care centers, reflecting its diverse applications in cardiovascular disease diagnosis and monitoring.

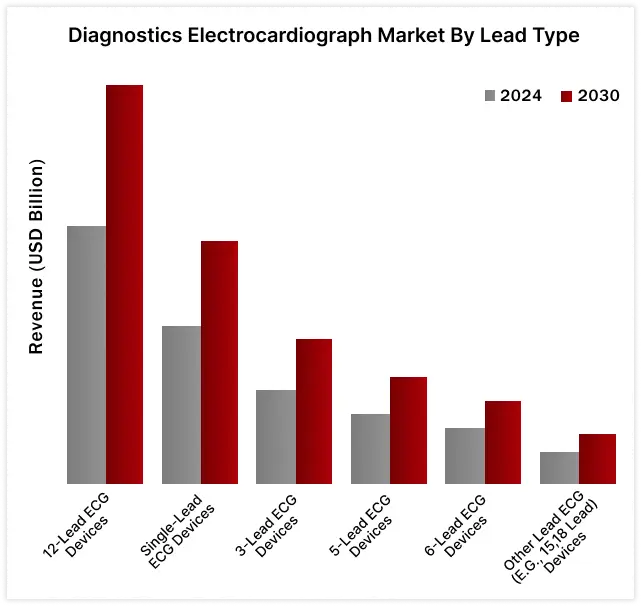

12 Lead ECG devices by lead type dominated the diagnostics ECG market in the year 2024

ECG devices held the largest market share by product type in the diagnostics ECG market in the year 2024

Asia Pacific will show the highest growth rate in the diagnostics ECG market in the forecast period. (2025-2030)

This is driven by several converging factors. Rapid economic development, particularly in countries like China and India, increasing disposable incomes and boosting access to advanced healthcare services, including cardiac diagnostics. The region is also facing a growing burden of cardiovascular diseases (CVDs), fueled by increasing urbanization, sedentary lifestyles, and aging populations, necessitating more widespread ECG screening and monitoring. Substantial investments are being made across the region to upgrade healthcare infrastructure, expanding the availability of diagnostic services in both urban and rural areas. Heightened public awareness regarding heart health and the importance of early detection, coupled with increasing healthcare professional adoption of ECG technology for routine check-ups and disease management, further propel market growth. Furthermore, the rise of telemedicine and remote patient monitoring in the region is increasing the demand for portable and ambulatory ECG devices. Technological advancements, such as the integration of Artificial Intelligence (AI) for automated ECG analysis and the development of more user-friendly and portable devices, are enhancing diagnostic accuracy and patient convenience, driving adoption. For instance, recent data indicates that China’s cardiovascular disease burden is escalating, with the China Cardiovascular Disease Report 2023 highlighting over 330 million CVD patients, creating a massive demand for diagnostic tools like ECGs. Similarly, India’s growing middle class and government initiatives like the National Programme for Prevention and Control of Cancer, Diabetes, Cardiovascular Diseases & Stroke (NPCDCS) are increasing focus on cardiac health screening. These factors, combined with the increasing volume of cardiovascular procedures and the expanding healthcare sector, position Asia Pacific as the key growth engine for the global diagnostic ECG market in the coming years.

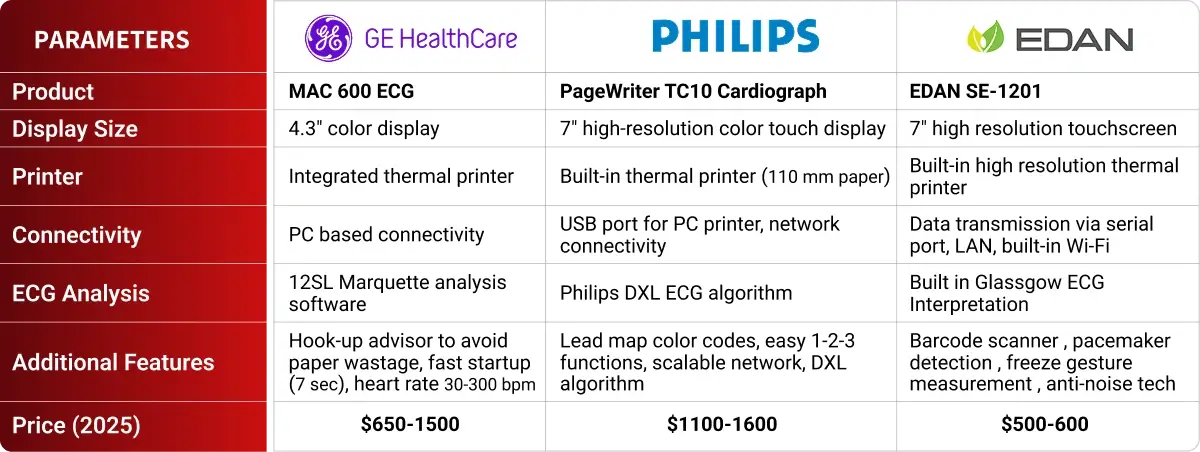

BRAND ANALYSIS: PORTABLE ECG DEVICES

“The integration of artificial intelligence (AI) algorithms with Electrocardiogram (ECG) interpretation platforms is facilitating automated detection and quantification of arrhythmias, ischemic changes, and potential structural heart abnormalities, augmenting clinician decision-making and potentially improving diagnostic accuracy and triage efficiency.”Cardiology Technologist– Large Academic Medical Center (Europe)“The proliferation of wearable ECG monitoring devices, coupled with cloud-based data analytics, is enabling continuous and remote cardiac rhythm surveillance, empowering patients with chronic conditions and facilitating timely intervention while creating new data streams for population health management.”Chief Medical Information Officer– Integrated Healthcare System (Asia Pacific)“The convergence of ECG data with other vital signs, electronic health records, and patient-reported outcomes within unified digital health platforms is providing a more comprehensive clinical picture, enabling more personalized risk stratification and facilitating data-driven improvements in cardiovascular care pathways.”Director of Clinical Informatics– Multi-Specialty Group Practice (North America)“The increasing adoption of automated ECG analysis software in primary care and point-of-care settings is streamlining workflow, reducing interpretation time, and standardizing initial assessments, potentially improving access to basic cardiac screening and early detection of abnormalities outside of specialist environments.”Practice Manager– Primary Care Network (Latin America)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

Particulars | Details |

| Report | Diagnostics ECG Market |

| Forecast Period | 2025-2030 |

| Base Year | 2024 |

| Format | |

| Market Size (2024) | USD 8.2 Billion |

| CAGR (2025-2030) | 7.6 % |

| Number of Pages | 165 |

| Number of Tables | 159 |

| Number of Figures | 40 |

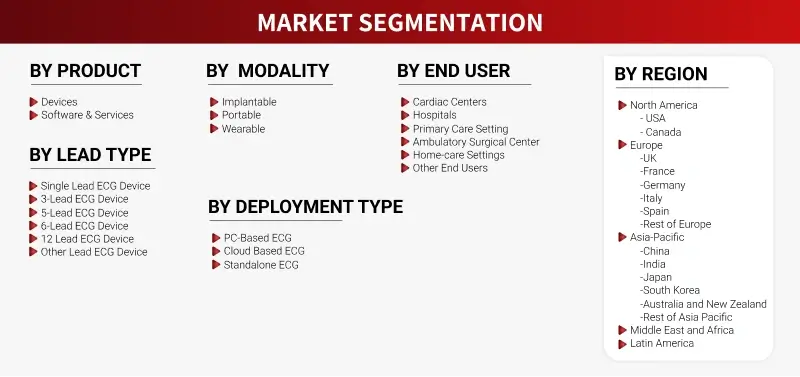

| Key Segments | Diagnostics ECG Market by Product Type. (Devices, Software & Services) Diagnostics ECG Market by Modality Type (Implantable, Portable, Wearable) Diagnostics ECG Market by Lead Type (Single Lead ECG, 3 Lead ECG, 5 Lead ECG, 6 Lead ECG, 12 Lead ECG, Other Lead ECG) Diagnostics ECG Market by Deployment/Connectivity Type (PC-Based ECG, Cloud Based ECG, Standalone ECG) Diagnostics ECG Market by End User Type (Cardiac Centers, Hospitals, Primary Care Setting, Ambulatory Surgical Center, Homecare Settings, Other End Users) |

| Regions Covered | § North America: US and Canada § Europe: Germany, UK, France, Italy, Spain, and Rest of the Europe § Asia-Pacific: China, Japan, India, South Korea, Australia and New Zealand, and Rest of the Asia-Pacific § Latin America § Middle East and Africa |

| Key Players Covered (Majority Share Holders) | GE Healthcare (US), Schiller AG (Switzerland), Koninklijke Philips N.V. (Netherlands), Nihon Kohden Corporation (Japan), Spacelabs Healthcare (US), Edan Instruments Inc. (China), Shenzhen Mindray Biomedical Electronics Co., Ltd. (China), Fukuda Denshi Co., Ltd. (Japan), Medtronic (Ireland), BPL Medical Technologies (India), Lepu Medical Technology (China), Allengers Medical Systems (India), ACS Diagnostics (US) |

| Other Players | AliveCor, Inc. (US), Borsam Medical (China), BTL (UK), Biomedical Instruments Co., Ltd. (China), Cardiac Insight, Inc. (US), Edan Instruments, Inc. (China), Lifesignals (US), Nasiff Associates, Inc. (US), Qingdao Meditech Equipment Co., Ltd. (China), Vectracor, Inc. (US), VitalConnect (US) |

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. DIAGNOSTICS ECG MARKET: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. REGULATORY SCENARIO & TRENDS

4.5. NEED GAP ANALYSIS

4.6. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.7. CASE STUDY ANALYSIS

4.8. TECHNOLOGY ANALYSIS

4.9. TRADE ANALYSIS

4.10. INDUSTRY TRENDS

4.11. PRICING ANALYSIS

4.12. REIMBURSEMENT SCENARIO

4.13. USE OF AI IN DIAGNOSTICS ECG DEVICE

4.14. PORTER’S FIVE FORCES ANALYSIS

4.15. IMPACT OF US TARIFF [2025]

4.16. REGULATORY LANDSCAPE

4.16.1. NORTH AMERICA

4.16.2. EUROPE

4.16.3. ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. GLOBAL DIAGNOSTICS ECG MARKET, BY PRODUCT TYPE (2024-2030, USD MILLION)

6.1. DEVICES

6.1.1.STRESS ECG DEVICES

6.1.2.RESTING ECG DEVICES

6.1.3.HOLTER ECG DEVICES

6.1.4.EVENT MONITOR DEVICES

6.1.5.IMPLANTABLE LOOP RECORDERS

6.1.6.MOBILE CARDIAC TELEMETRY DEVICE

6.1.7.SMART ECG MONITORS

6.2. SOFTWARE & SERVICES

7. GLOBAL DIAGNOSTICS ECG MARKET, BY MODALITY TYPE (2024-2030, USD MILLION)

7.1. IMPLANTABLE

7.2. PORTABLE

7.3. WEARABLE

8. GLOBAL DIAGNOSTICS ECG MARKET, BY LEAD TYPE (2024-2030, USD MILLION)

8.1. SINGLE LEAD ECG

8.2. 3-LEAD ECG

8.3. 5-LEAD ECG

8.4. 6-LEAD ECG

8.5. 12 LEAD ECG

8.6. OTHER LEAD ECG

9. GLOBAL DIAGNOSTICS ECG MARKET, BY DEPLOYMENT/CONNECTIVITY TYPE (2024-2030, USD MILLION)

9.1. PC-BASED ECG

9.2. CLOUD BASED ECG

9.3. STANDALONE ECG

10. GLOBAL DIAGNOSTICS ECG MARKET, BY END USERS (2024-2030, USD MILLION)

10.1. CARDIAC CENTERS

10.2. HOSPITALS

10.3. PRIMARY CARE SETTING

10.4. AMBULATORY SURGICAL CENTER

10.5. HOMECARE SETTINGS

10.6. OTHER END USERS

11. GLOBAL DIAGNOSTICS ECG MARKET, BY REGION (2024-2030, USD MILLION)

11.1. NORTH AMERICA

11.1.1. US

11.1.2. CANADA

11.2. EUROPE

11.2.1. GERMANY

11.2.2. FRANCE

11.2.3. SPAIN

11.2.4. ITALY

11.2.5. UK

11.2.6. REST OF THE EUROPE

11.3. ASIA-PACIFIC

11.3.1. CHINA

11.3.2. JAPAN

11.3.3. INDIA

11.3.4. AUSTRALIA AND NEW ZEALAND

11.3.5. SOUTH KOREA

11.3.6. REST OF THE ASIA-PACIFIC

11.4. MIDDLE EAST AND AFRICA

11.5. LATIN AMERICA

12. COMPETITIVE ANALYSIS

12.1. PRODUCT PIPELINE: DIAGNOSTICS ECG DEVICES

12.2. KEY PLAYERS FOOTPRINT ANALYSIS

12.3. MARKET SHARE ANALYSIS (2023/2024)

12.4. REGIONAL SNAPSHOT OF KEY PLAYERS

12.5. R&D EXPENDITURE OF KEY PLAYERS

13. COMPANY PROFILES

13.1. GE HEALTHCARE (US)

13.1.1. BUSINESS OVERVIEW

13.1.2. PRODUCT PORTFOLIO

13.1.3. FINANCIAL SNAPSHOT

13.1.4. RECENT DEVELOPMENTS

13.1.4.1. MERGER/ACQUISITIONS

13.1.4.2. PRODUCT APPROVAL/LAUNCHES

13.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

13.1.4.4. EXPANSIONS

13.2. SCHILLER AG (SWITZERLAND)

13.3. KONINKLIJKE PHILIPS N.V. (NETHERLANDS)

13.4. NIHON KOHDEN CORPORATION (JAPAN)

13.5. SPACELABS HEALTHCARE (US)

13.6. EDAN INSTRUMENTS INC. (CHINA)

13.7. SHENZHEN MINDRAY BIOMEDICAL ELECTRONICS CO., LTD. (CHINA)

13.8. FUKUDA DENSHI CO., LTD. (JAPAN)

13.9. MEDTRONIC (IRELAND)

13.10. BPL MEDICAL TECHNOLOGIES (INDIA)

13.11. LEPU MEDICAL TECHNOLOGY (CHINA)

13.12. ALLENGERS MEDICAL SYSTEMS (INDIA)

13.13. ACS DIAGNOSTICS (US)

13.14. BOSTON SCIENTIFIC CORPORATION (US)

13.15. ABBOTT LABORATORIES (US)

13.16. BAXTER (HILL-ROM HOLDINGS, INC.). (US)

13.17. OSI SYSTEMS, INC. (US)

13.18. BITTIUM. (FINLAND)

13.19. IRHYTHM TECHNOLOGIES, INC. (US)

13.20. MIDMARK CORPORATION (US)

13.21. BIONET CO., LTD. (SOUTH KOREA)

13.22. OTHER PLAYERS

13.22.1. ALIVECOR, INC. (US)

13.22.2. BORSAM MEDICAL (CHINA)

13.22.3. BTL (UK)

13.22.4. BIOMEDICAL INSTRUMENTS CO., LTD. (CHINA)

13.22.5. CARDIAC INSIGHT, INC. (US)

13.22.6. EDAN INSTRUMENTS, INC. (CHINA)

13.22.7. LIFESIGNALS (US)

13.22.8. NASIFF ASSOCIATES, INC. (US)

13.22.9. QINGDAO MEDITECH EQUIPMENT CO., LTD. (CHINA)

13.22.10. VECTRACOR, INC. (US)

13.22.11. VITALCONNECT (US)

14. APPENDIX

14.1. INDUSTRY SPEAK

14.2. QUESTIONNAIRE/DISCUSSION GUIDE

14.3. AVAILABLE CUSTOM WORK

14.4. ADJACENT STUDIES

14.5. AUTHORS.

15. REFERENCES

Market Definition: Electrocardiography (ECG) Market

The Electrocardiography (ECG) Market is a critical and rapidly evolving sector within the global healthcare industry. It centers on the technology and equipment used to record the electrical activity generated by the heart over time. This market encompasses a wide array of products and services designed for diagnosing, monitoring, and managing cardiovascular conditions. Key components include various ECG devices such as resting ECG machines, stress ECG systems for exercise testing, ambulatory monitors like Holters and event recorders for long-term tracking, and increasingly prevalent wearable ECG devices.

The market also involves ECG analysis software, often incorporating advanced algorithms including artificial intelligence for interpretation assistance, as well as essential consumables like electrodes and lead wires. ECG technology is fundamental for visualizing the heart’s electrical patterns, enabling clinicians to detect arrhythmias, identify signs of a heart attack, assess conduction abnormalities, evaluate chamber enlargement, and monitor overall cardiac function. By providing objective data on heart rhythm and electrical intervals, ECGs are indispensable for accurate diagnosis, risk stratification, guiding therapeutic interventions (such as medication management, pacemaker implantation, or ablation procedures), and monitoring the progression or stability of cardiac diseases.

The ability to quickly and non-invasively obtain reliable cardiac electrical information is vital for improving diagnostic precision, enhancing patient outcomes, increasing efficiency in clinical workflows, and managing both acute cardiac events and chronic heart conditions across various healthcare settings, from hospitals and clinics to ambulatory care and home monitoring environments.

FIGURE: DIAGNOSTICS ECG MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the diagnostics ECG market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the diagnostics ECG market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the diagnostics ECG market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major developers offering various diagnostics ECG will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of diagnostics ECG market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the diagnostics ECG industry.