According to our latest industry forecast report 2025, the global Immunoassay market was valued at USD 31.6 billion in 2024 and is projected to reach USD 44.8 billion by 2030, expected to grow at a CAGR of 6% during the forecast period, 2025-2030.

Furthermore, the US with USD 10.1 billion market in 2024, held a significant share in the global immunoassay market and is likely to show the growth at a CAGR of 6.2% within this market, during the forecast period (2025-2030).

Global Immunoassay market is anticipated to reach USD 44.8 billion by 2030 from USD 31.6 billion in 2024, growing at an annualized rate of 6% during the period, 2025-2030 | North America represents a significant and mature market for immunoassays, driven by high disease awareness, advanced healthcare infrastructure, strong pharmaceutical and biotechnology sectors, and significant R&D investment. The region benefits from early adoption of innovative diagnostic technologies, substantial healthcare spending, and the presence of major market players with extensive distribution networks. | Asia-Pacific Asia-Pacific’s immunoassay market is experiencing significant growth, fueled by rapid urbanization, substantial investments in healthcare infrastructure development, and the growing pharmaceutical and biotechnology sectors. Favorable government policies promoting healthcare access, coupled with increasing adoption of advanced diagnostics in clinical and research settings, are key drivers propelling market expansion in the region. |

The immunoassay market is evolving rapidly, driven by increasing demand for high-sensitivity, high-throughput, and multiplex testing solutions across key areas like clinical diagnostics, research, and point-of-care testing. | Global investment in immunoassay R&D is heavily focused on increasing sensitivity, multiplexing capabilities, point-of-care testing (POCT) formats, and automation. This innovation is enabling earlier disease detection, personalized medicine, rapid diagnostics (especially crucial for infectious diseases), and more efficient research processes, highlighting the industry’s critical role in modern healthcare and life sciences. |

Drivers: Rising Disease Burden and Diagnostic Needs Drive Immunoassay Market Growth

Strong demand from key end-use sectors such as clinical diagnostics labs (for infectious diseases, cancer, cardiac markers), point-of-care testing (POCT) sites (for rapid results in emergencies and remote areas), and research institutions (for biomarker discovery and drug development), coupled with advancements in immunoassay technologies (e.g., increased sensitivity, automation, multiplexing), is fueling market adoption. The convergence of growing chronic and infectious disease burdens, the need for personalized medicine and companion diagnostics, and the shift towards more efficient and accessible testing methods (like POCT) is supporting the widespread use of immunoassays across diverse healthcare and research applications, stimulating market growth.

Opportunities: Exploring New Horizons: Expanding Applications and Innovative Formats

The market is rapidly expanding through innovation in multiplex assays (enabling simultaneous detection of multiple biomarkers), development of novel biomarkers for earlier and more accurate diagnoses, and the integration of digital health solutions (for data management and telemedicine). Forming partnerships across sectors like oncology (companion diagnostics), infectious disease surveillance, and veterinary diagnostics creates a fertile ground for assay innovation. With the growing global demand for precision medicine, rapid diagnostics (especially for critical conditions), and improved healthcare access, there are significant opportunities for both established immunoassay companies and new players to innovate and succeed, particularly in developing niche applications and expanding into emerging markets.

Challenges: Regulatory and Technical Hurdles Impede Immunoassay Market Progress

Despite growing demand, the immunoassay industry confronts significant obstacles. Key challenges include the high cost of advanced instruments and reagents, stringent and varying regulatory approvals (e.g., FDA, CE Mark) required for new assays, and the substantial investment required for R&D and extensive validation to meet increasingly demanding performance specifications. Furthermore, difficulties arise in achieving high sensitivity and specificity, managing cross-reactivity, ensuring assay standardization across different platforms, and managing the complexities of sample collection and logistics. These factors create hurdles for product development, market entry, and maintaining competitive pricing and consistent performance.

The global immunoassay market, serving critical needs in clinical diagnostics, pharmaceutical development, and research, is experiencing robust expansion driven by aging populations, rising disease burdens, and technological advancements. Valued at approximately USD 31.6 billion in 2024, the market is projected to reach nearly USD 44.8 billion by 2030, growing at a CAGR of 6%. Key drivers include increasing demand for molecular diagnostics and companion diagnostics in healthcare, the shift towards multiplex and high-sensitivity assays, and the expanding use in point-of-care testing (POCT) and academic research.

North America dominates the market share, fueled by advanced healthcare infrastructure and high disease awareness. Europe remains significant, supported by strong pharmaceutical industries and regulatory frameworks. The Asia-Pacific region is experiencing the fastest growth, driven by increasing healthcare investments, large populations, and growing chronic disease prevalence. Ongoing advancements in assay technologies, development of novel biomarkers, and the increasing adoption of automation in laboratory settings are expected to further propel the global immunoassay market in the coming years.

Furthermore, its long history and extensive literature base make it a trusted and standard method in many laboratories. The continued strength of research and development activities, along with its widespread use in clinical diagnostics, food safety testing, and drug discovery, serves as a major driver for this technology. Additionally, the relative simplicity of the basic technique and the availability of numerous commercial kits contribute to its enduring market leadership.

Furthermore, investments in healthcare infrastructure, particularly in developing regions, and the adoption of automated immunoassay systems capable of high throughput testing within hospital settings serve as major drivers for this segment. The critical role hospitals play in emergency care and managing acute conditions also necessitates readily available immunoassay capabilities.

Asia-Pacific projected to be the fastest-growing segment by region in the forecast period (2025-2030)

In the forecast period from 2025 to 2030, Asia-Pacific is projected to be the fastest growing segment in the global immunoassay market by region. This rapid growth trajectory is driven by factors such as significant economic development and expanding healthcare infrastructure, a large population, therefore a bigger pool of people. These countries are witnessing substantial increases in healthcare spending and a growing awareness of the importance of diagnostics. The large and often young populations contribute to a higher incidence of infectious diseases and an increasing burden of chronic conditions requiring continuous monitoring, driving demand for both clinical laboratory and point-of-care testing. Furthermore, expanding pharmaceutical and biotechnology sectors in the region are increasing R&D activities, utilizing immunoassays for drug discovery and development. Government initiatives to improve public health access also play a significant role in boosting the adoption of diagnostic tools across the region.

Major players operating in the immunoassay market are;

Note; The price above given is from the company’s websites or third-party websites.

Sources: Secondary Research

“Adherence to stringent quality control standards and regulatory approvals (like FDA and CE-IVD) for immunoassay kits and instruments is becoming a major bottleneck, forcing companies to invest heavily in compliance expertise and documentation.”

Regulatory Affairs Lead – In Vitro Diagnostics (IVD) Company(North America)

“The increasing prevalence of chronic diseases and cancer globally is driving significant demand for rapid point-of-care (POC) immunoassay devices, pushing manufacturers to focus on miniaturization and faster turnaround times.”

Immunoassay Product Manager – Medical Device Manufacturer(Europe)

“The growing adoption of automated immunoassay systems in clinical laboratories to enhance throughput and reduce manual errors is compelling manufacturers to integrate sophisticated software and connectivity features.”

CEO – Healthcare Consulting Firm (Asia-Pacific)

“Fluctuations in the supply chain for critical raw materials, such as specific enzymes and antibodies used in immunoassay reagents, are impacting production stability and forcing companies to seek alternative suppliers or develop more resilient sourcing strategies.”

Supply Chain Director – Diagnostic Reagents Provider (Europe)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. IMMUNOASSAY MARKET: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS AND DEMAND PROJECTION IN USD, TILL 2030

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. RECENT DEVELOPMENT AND TRENDS

4.5. TECHNOLOGIES ANALYSIS

4.6. CASE STUDY ANALYSIS

4.7. PRICING ANALYSIS

4.8. NEED GAP ANALYSIS

4.9. KEY CONFERENCES

4.10. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.11. INDUSTRY TRENDS

4.12. PORTER’S FIVE FORCES ANALYSIS

4.13. REGULATORY LANDSCAPE

4.13.1. NORTH AMERICA

4.13.2. EUROPE

4.13.3. ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. CLINICAL TRIAL ANALYSIS

6.1. ANALYSIS BY TRIAL REGISTRATION YEAR

6.2. ANALYSIS BY PHASE OF DEVELOPMENT

6.3. ANALYSIS BY TRIAL STATUS

6.4. ANALYSIS BY NUMBER OF PATIENTS ENROLLED

6.5. ANALYSIS BY STUDY DESIGN

6.6. ANALYSIS BY TYPE OF THERAPY / DRUG

6.7. ANALYSIS BY GEOGRAPHY

6.8. ANALYSIS BY KEY SPONSORS / COLLABORATORS

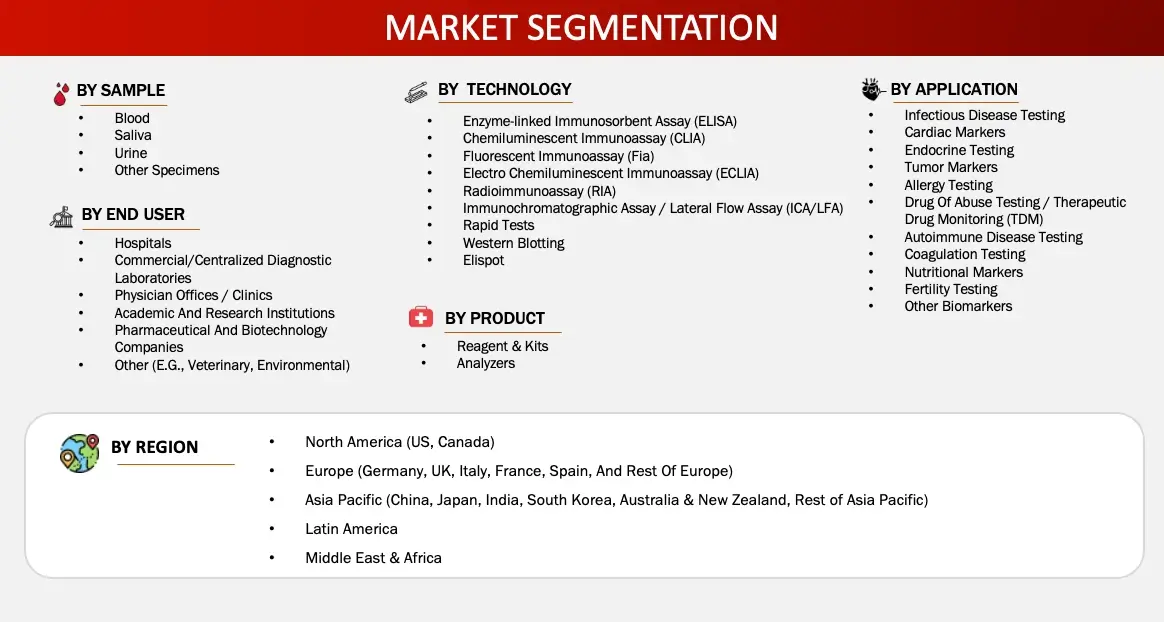

7. GLOBAL IMMUNOASSAY MARKET, BY PRODUCT (2024-2030, USD MILLION)

7.1. REAGENT & KITS

7.1.1. ELISA REAGENTS & KITS

7.1.2. CLIA REAGENTS & KITS

7.1.3. FIA REAGENTS & KITS

7.1.4. RAPID TEST REAGENTS & KITS

7.1.5. ELISPOT REAGENTS & KITS

7.1.6. WESTERN BLOT REAGENTS & KITS

7.1.7. OTHER REAGENTS & KITS

7.2. ANALYSERS

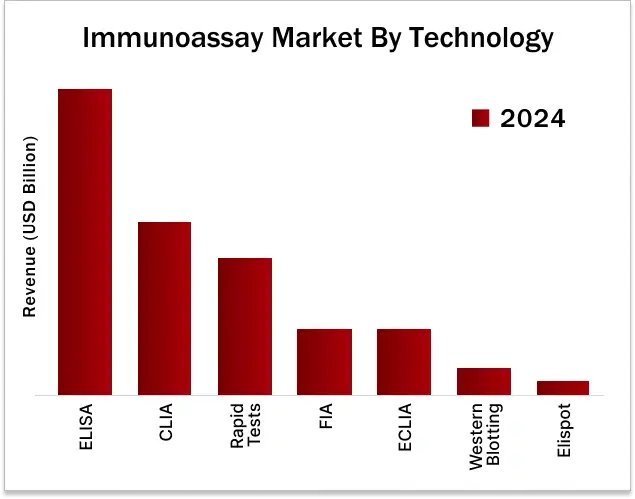

8. GLOBAL IMMUNOASSAY MARKET, BY TECHNOLOGY (2024-2030, USD MILLION)

8.1. ENZYME-LINKED IMMUNOSORBENT ASSAY (ELISA)

8.2. CHEMILUMINESCENT IMMUNOASSAY (CLIA)

8.3. FLUORESCENT IMMUNOASSAY (FIA)

8.4. ELECTRO CHEMILUMINESCENT IMMUNOASSAY (ECLIA)

8.5. RAPID TESTS

8.6. WESTERN BLOTTING

8.7. ELISPOT

9. GLOBAL IMMUNOASSAY MARKET, BY SAMPLE (2024-2030, USD MILLION)

9.1. BLOOD

9.2. SALIVA

9.3. URINE

9.4. OTHER SPECIMENS

10. GLOBAL IMMUNOASSAY MARKET, BY APPLICATION (2024-2030, USD MILLION)

10.1. INFECTIOUS DISEASE TESTING

10.2. CARDIAC MARKERS

10.3. ENDOCRINE TESTING

10.4. TUMOUR MARKERS

10.5. ALLERGY TESTING

10.6. DRUG OF ABUSE TESTING / THERAPEUTIC DRUG MONITORING (TDM)

10.7. AUTOIMMUNE DISEASE TESTING

10.8. COAGULATION TESTING

10.9. NUTRITIONAL MARKERS

10.10. FERTILITY TESTING

10.11. OTHER BIOMARKERS

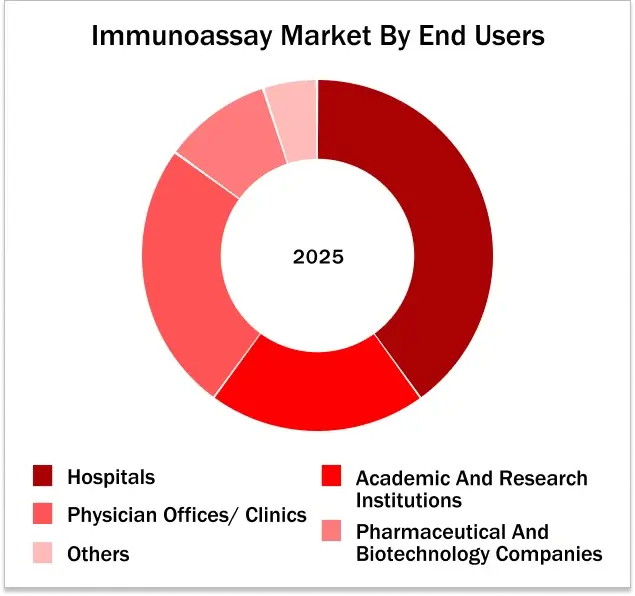

11. GLOBAL IMMUNOASSAY MARKET, BY END USERS (2024-2030, USD MILLION)

11.1. HOSPITALS

11.2. COMMERCIAL/CENTRALIZED DIAGNOSTIC LABORATORIES

11.3. PHYSICIAN OFFICES / CLINICS

11.4. ACADEMIC AND RESEARCH INSTITUTIONS

11.5. PHARMACEUTICAL AND BIOTECHNOLOGY COMPANIES

11.6. OTHER (E.G., VETERINARY, ENVIRONMENTAL)

12. GLOBAL IMMUNOASSAY MARKET, BY REGION (2024-2030, USD MILLION)

12.1. NORTH AMERICA

12.1.1. US

12.1.2. CANADA

12.2. EUROPE

12.2.1. GERMANY

12.2.2. FRANCE

12.2.3. SPAIN

12.2.4. ITALY

12.2.5. UK

12.2.6. REST OF THE EUROPE

12.3. ASIA-PACIFIC

12.3.1. CHINA

12.3.2. JAPAN

12.3.3. INDIA

12.3.4. AUSTRALIA AND NEW ZEALAND

12.3.5. SOUTH KOREA

12.3.6. REST OF THE ASIA-PACIFIC

12.4. MIDDLE EAST AND AFRICA

12.5. LATIN AMERICA

13. COMPETITIVE ANALYSIS

13.1. REVENUE ANALYSIS

13.2. KEY PLAYERS FOOTPRINT ANALYSIS

13.3. MARKET SHARE ANALYSIS (2023/2024)

13.4. REGIONAL SNAPSHOT OF KEY PLAYERS

13.5. R&D EXPENDITURE OF KEY PLAYERS

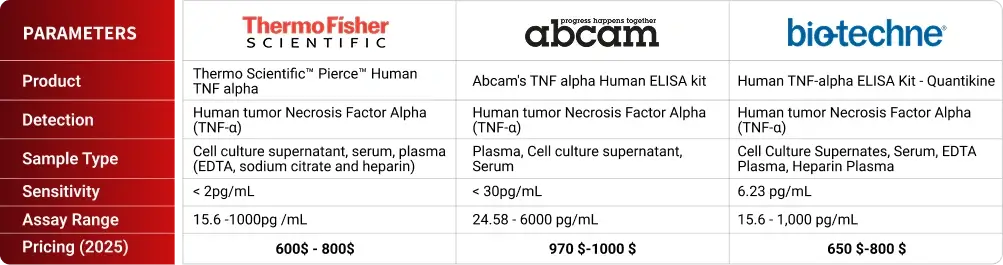

13.6. BRAND/ PRODUCT COMPARISON

14. COMPANY PROFILES

14.1. F. HOFFMANN – LA ROCHE LTD. (SWITZERLAND)

14.1.1. BUSINESS OVERVIEW

14.1.2. PRODUCT PORTFOLIO

14.1.3. FINANCIAL SNAPSHOT

14.1.4. RECENT DEVELOPMENTS

14.1.4.1. MERGER/ACQUISITIONS

14.1.4.2. PRODUCT APPROVAL/LAUNCHES

14.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

14.1.4.4. EXPANSIONS

14.2. ABBOTT (US)

14.3. AGILENT TECHNOLOGIES, INC. (US)

14.4. SIEMENS HEALTHINEERS (GERMANY)

14.5. THERMO FISHER SCIENTIFIC INC (US)

14.6. BIOMÉRIEUX (FRANCE)

14.7. DANAHER CORPORATION (US)

14.8. BIO-RAD LABORATORIES INC. (US)

14.9. FUJIREBIO (JAPAN)

14.10. PERKINELMER INC (

14.11. BECTON DICKENSON AND COMPANY (BD) (US)

14.12. DIASORIN S.P.A (ITALY)

14.13. QUIDELORTHO CORPORATION (US)

14.14. QIAGEN (NETHERLANDS)

14.15. SYSMEX CORPORATION (JAPAN)

14.16. MINDRAY (CHINA)

14.17. OTHER PLAYERS

14.17.1. J. MITRA & CO. PVT. LTD. (INDIA)

14.17.2. MERIDIAN BIOSCIENCE (US)

14.17.3. BIO-TECHNE (US)

14.17.4. ABNOVA CORPORATION (TAIWAN)

14.17.5. REVVITY (US), CELLABS (AUSTRALIA)

14.17.6. TOSOH CORPORATION (JAPAN)

14.17.7. ENZO BIOCHEM (US), CREATIVE DIAGNOSTICS (US)

14.17.8. BOSTER BIOLOGICAL TECHNOLOGY (US)

14.17.9. ELABSCIENCE (US)

14.17.10. WAK-CHEMIE MEDICAL GMBH (GERMANY)

14.17.11. KAMIYA BIOMEDICAL COMPANY (US)

14.17.12. GYROS PROTEIN TECHNOLOGIES (SWEDEN)

14.17.13. MERCK KGAA (GERMANY)

15. APPENDIX

15.1. INDUSTRY SPEAK

15.2. QUESTIONNAIRE/DISCUSSION GUIDE

15.3. AVAILABLE CUSTOM WORK

15.4. ADJACENT STUDIES

15.5. AUTHORS

16. REFERENCES

The immunoassay market encompasses the research, development, production, and distribution of biochemical tests that detect and quantify specific biological molecules (like antigens and antibodies) using the principles of antigen-antigen/antibody interactions. These assays are integral to various applications, from routine clinical diagnostics and disease monitoring to complex pharmaceutical research and development, providing critical information about health status, disease presence, and biological processes. The scope of the industry includes not just the development of specific antibodies and reagents, but also the design of assay platforms, instruments, and software necessary for accurate detection and data analysis, along with the quality control processes ensuring reliable and reproducible results, including adherence to regulatory standards like FDA, CE Mark, and IVDR.

Driven by the increasing global burden of chronic and infectious diseases, the demand for rapid and accurate diagnostic information, as well as advancements in medical research and personalized medicine, immunoassays have become essential tools in healthcare and biotechnology. The market is characterized by continuous innovation in assay technologies (such as high-sensitivity chemiluminescent and multiplex assays), detection methods (like lateral flow and digital assays), and automation, alongside a complex landscape of regulatory requirements (e.g., IVD regulations) and the need for precise validation across diverse clinical and research settings. With the expanding role of diagnostics in patient care, disease management, and drug development, the immunoassay market continues to adapt, offering faster, more sensitive, and more accessible testing solutions, driving innovation in clinical diagnostics, research, and point-of-care testing.

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the immunoassay market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the immunoassay technology market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the immunoassay market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major manufacturers offering various immunoassay will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of immunoassay market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the immunoassay market industry.