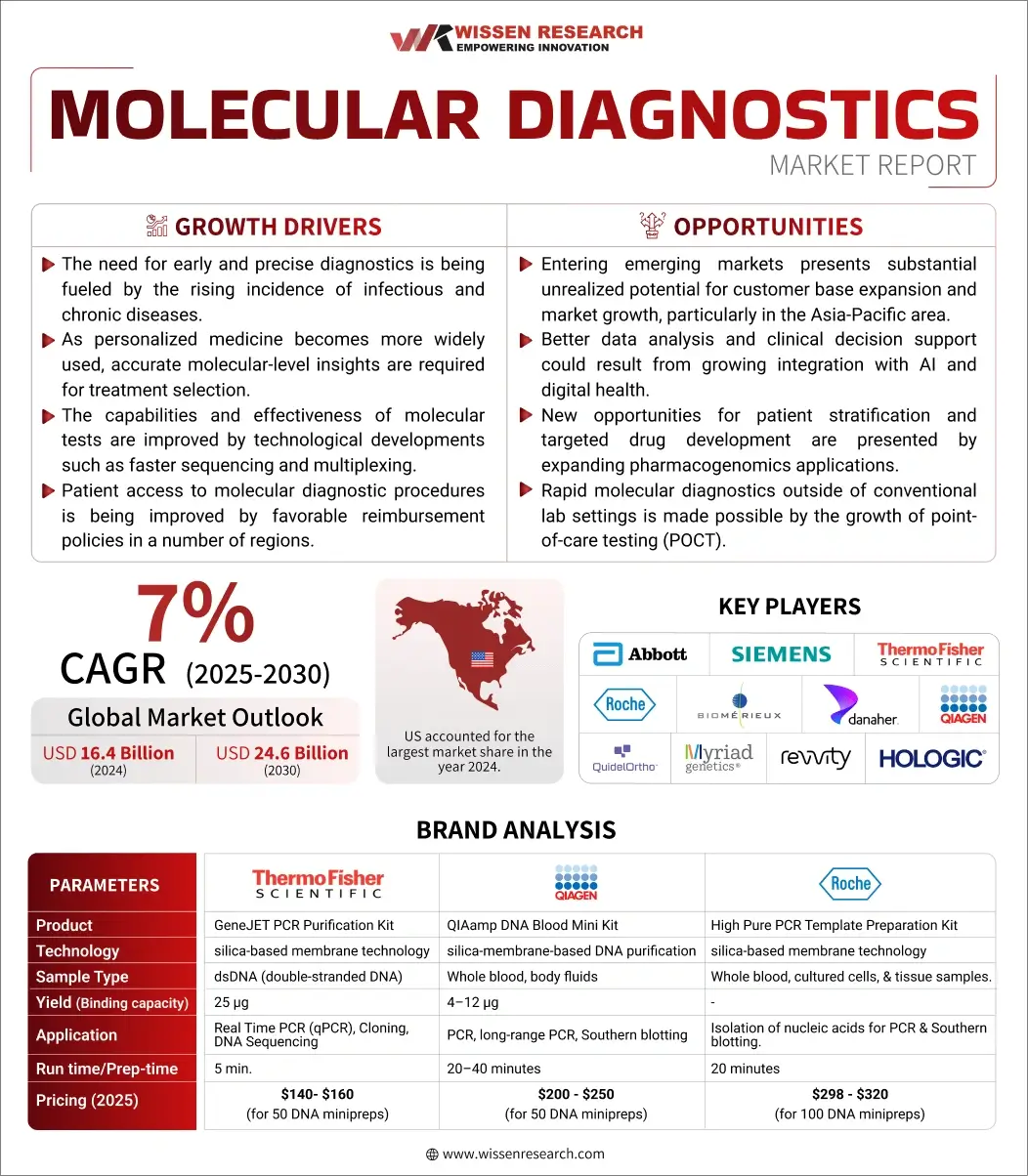

Wissen Research analyzed that the global molecular diagnostics market was valued at USD 16.4 billion in 2024 and is projected to reach USD 24.6 billion by 2030, expected to grow at a CAGR of 7% during the forecast period, 2025-2030.

Furthermore, the US with USD 5.1 billion market in 2024, held the largest share in the global molecular diagnostics market and is likely to show the growth at a CAGR of 7.2% within this market, during the forecast period (2025-2030).

Global molecular diagnostics market is anticipated to reach USD 24.6 billion by 2030 from USD 16.4 billion in 2024, growing at an annualized rate of 7% during the period, 2025-2030 | North America represents a significant and mature market for molecular diagnostics, driven by high disease awareness, advanced healthcare infrastructure, strong pharmaceutical and biotechnology sectors, and significant R&D investment. The region benefits from early adoption of innovative diagnostic technologies, substantial healthcare spending, and the presence of major market players with extensive distribution networks, particularly strong in next-generation sequencing and PCR technologies. | Asia-Pacific Asia-Pacific’s molecular diagnostics market is growing significantly, driven by rapid urbanization, major healthcare infrastructure investments, and expanding life sciences sectors. Favorable government policies and increasing adoption of advanced genetic testing for clinical and research applications are key factors boosting this regional expansion. |

Molecular diagnostics market is evolving rapidly, driven by increasing demand for high-sensitivity, high-resolution, & comprehensive genetic testing solutions across key areas like infectious disease detection, oncology, genetic disorder screening, pharmacogenomics, & clinical research. | Global investment in molecular diagnostics R&D is heavily focused on increasing sensitivity, expanding testing panels (multiplexing), developing point-of-care testing (POCT) formats, enhancing sample preparation methods, and improving data analysis capabilities, particularly for Next-Generation Sequencing (NGS). This innovation is enabling earlier disease detection (especially for infectious diseases and cancer), personalized medicine through pharmacogenomics and companion diagnostics, rapid pathogen identification, and more comprehensive genetic insights, highlighting the industry’s critical role in modern healthcare and life sciences. |

Drivers: Rising Demand for Genetic Insights Drives Molecular Diagnostics Market

The increasing prevalence of infectious diseases and genetic disorders, coupled with growing demand from oncology for liquid biopsies and companion diagnostics, is driving the market. Strong adoption in clinical diagnostics labs, research institutions, and increasingly in point-of-care settings, alongside advancements in PCR and Next-Generation Sequencing (NGS) technologies, fuels market growth. The push for personalized medicine, early disease detection, and pharmacogenomics, supported by significant healthcare spending and R&D investment, particularly in North America and Europe, is stimulating widespread use across diverse healthcare applications.

Opportunities: Market Expansion Through Innovation and Diversification

The molecular diagnostics market is experiencing significant expansion driven by technological advancements and the exploration of new application areas. Opportunities are abundant in the development and refinement of cutting-edge technologies like Next-Generation Sequencing (NGS), which offers unparalleled depth of genetic analysis, and the creation of rapid molecular tests that deliver results much faster than traditional methods. A key focus is on identifying and validating novel genetic biomarkers, crucial for improving the accuracy of diagnoses in fields like oncology and inherited diseases. The integration of molecular diagnostics with digital health platforms and Artificial Intelligence (AI) is opening doors for better data management, interpretation, and the potential for telemedicine applications. Furthermore, the market is diversifying into new sectors, including the burgeoning field of direct-to-consumer genetic testing, offering personalized insights. With the persistent need for rapid pathogen identification, especially highlighted by recent global health events, and the growing importance of pharmacogenomics and non-invasive prenatal testing (NIPT), there are substantial prospects for companies that can innovate in assay development, offer value-added data interpretation services, and strategically expand their presence into emerging markets where access to advanced genetic testing is increasing.

Challenges: Navigating Regulatory, Technical, and Economic Barriers

Despite its growth potential, the molecular diagnostics market encounters substantial obstacles that impede its full advancement. A primary challenge lies in the significant financial investment required; sophisticated instruments like NGS platforms and the complex reagents and assays are expensive, creating a barrier to adoption, particularly for smaller labs or in resource-limited settings. Navigating the complex and often stringent regulatory landscape for genetic tests, which requires approvals from regulatory bodies like the FDA or CE marking, is another major hurdle, adding time and cost to product development. The field also demands high levels of expertise; interpreting the vast amounts of data generated, especially from NGS, requires specialized bioinformatics skills that are not universally available. Furthermore, ensuring the reliability and standardization of assays across different platforms and laboratories remains technically challenging. Practical issues such as maintaining sample stability during collection, transport, and storage for sensitive genetic materials, and preventing contamination in high-throughput environments, also pose significant difficulties. These multifaceted challenges—ranging from high costs and regulatory complexities to technical requirements and personnel expertise—create substantial barriers to market entry, widespread implementation, and maintaining cost-effective services.

The global molecular diagnostics market, crucial for pathogen detection, genetic disorder screening, oncology management, and personalized medicine, is experiencing high expansion driven by aging populations, rising disease burdens (especially cancer), and significant technological advancements. Valued at approximately USD 16.4 billion in 2024, the market is projected to reach nearly USD 24.6 billion by 2030, growing at a CAGR of 7%. Key drivers include increasing demand for rapid and accurate genetic testing, the growing use of PCR and NGS technologies in clinical diagnostics and drug development, the shift towards liquid biopsies and companion diagnostics, and the expanding applications in pharmacogenomics and infectious disease surveillance.

North America dominates the market share, fueled by advanced healthcare infrastructure, high R&D investment, and strong market players. Europe remains significant, supported by robust pharmaceutical industries and early technology adoption. The Asia-Pacific region is experiencing the fastest growth, driven by increasing healthcare investments, large populations, growing chronic and infectious disease prevalence, and expanding access to advanced diagnostics. Ongoing advancements in sequencing technologies, development of novel genetic biomarkers, and the increasing adoption of automation and AI for data analysis are expected to further propel the global molecular diagnostics market in the coming years

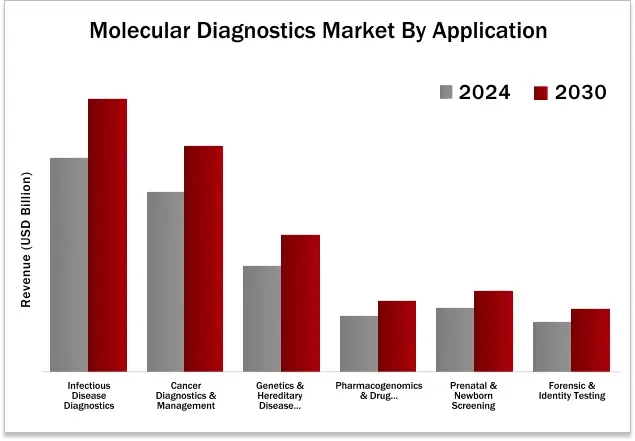

The molecular diagnostics market was dominated by infectious disease diagnostics by application type in 2024.

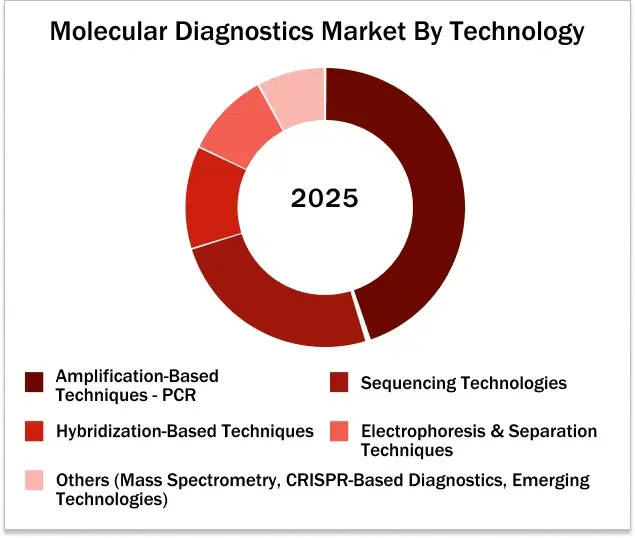

Polymerase Chain Reaction (Amplification-based technique) are estimated to hold the largest market share in the global molecular diagnostics market by technology in 2025.

Asia-Pacific is projected to be the fastest growing segment by region, in the forecast period (2025-2030)

The Asia Pacific molecular diagnostics market is set for strong growth. It is expected to be a major driver in the overall diagnostics sector and will likely outpace many other regions globally. This rapid growth results from several factors. First, there is an increasing burden of infectious diseases and chronic conditions, including various cancers, in the region. This makes highly sensitive and specific molecular diagnostics essential. Additionally, aging populations and changing lifestyles in countries like China, India, Japan, and South Korea raise the prevalence of chronic diseases.

These diseases require molecular testing for early detection, screening, and personalized management. Importantly, governments in the Asia Pacific are investing significantly to modernize healthcare systems. They are expanding insurance coverage and implementing national disease control programs with funding for advanced diagnostic capabilities, including molecular testing. At the same time, awareness is growing among clinicians and the public about the benefits of molecular diagnostics. These tools can lead to faster and more accurate diagnoses, better management of infectious diseases (including tracking antimicrobial resistance), and personalized medicine, especially in oncology, where companion diagnostics for targeted therapies are becoming the norm. The region is also quickly adopting new molecular technologies like Next-Generation Sequencing (NGS), Digital PCR (dPCR), and Multiplex PCR.

These technologies enable comprehensive genomic profiling, liquid biopsies, and the detection of multiple targets simultaneously. Moreover, the large patient population creates significant demand for diagnostics and positions the region as an attractive hub for global clinical trials. This requires strong support from molecular diagnostics. Support from international bodies, increasing regulatory efforts towards standardization, and more market opportunities are attracting investment. This investment is fostering local manufacturing and driving the introduction of innovative, often cost-effective, molecular biomarker technologies. These technologies are tailored to various healthcare settings, from major urban areas to remote regions. Together, these elements contribute to the dynamic and rapid growth of the molecular diagnostics market in Asia Pacific.

Major players operating in the molecular diagnostics market are;

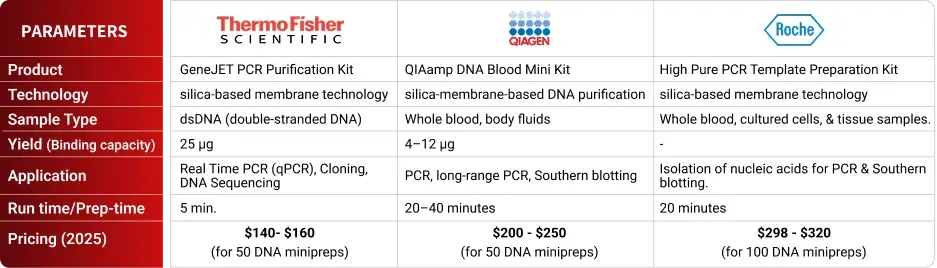

Note: The price given above is from the company’s websites or third-party websites.

Sources: Secondary Research

“Successfully transitioning advanced molecular diagnostics from large central labs to decentralized, point-of-care settings hinges on developing significantly more compact, automated, and user-friendly platforms, but achieving this technical leap while maintaining high sensitivity and specificity is proving extremely difficult and costly.

CEO – Molecular Diagnostics Instrumentation Company (North America)

“The sheer volume of raw data generated by next-generation sequencing and multiplex PCR platforms is outpacing our ability to develop scalable, cost-effective, and clinically validated bioinformatics solutions, creating a significant R&D bottleneck that impacts product time-to-market.”

CTO – Molecular Diagnostics Platform Company (Europe)

“Despite the clear clinical value of molecular diagnostics for guiding treatment, the fragmented global reimbursement landscape and lengthy payer approval processes remain a major strategic hurdle, forcing companies to navigate complex, often unpredictable, market access challenges.”

CEO – Molecular Diagnostics Service Provider (Asia-Pacific)

“Securing consistent and sustainable reimbursement models for novel molecular diagnostic tests, especially those used for prognostic or predictive purposes in oncology, is a major financial obstacle, limiting market access and return on investment for developers.”

Regulatory Affairs Lead – Molecular Diagnostics (MDx) Company (Global)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. MOLECULAR DIAGNOSTICS MARKET: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS AND DEMAND PROJECTION IN USD, TILL 2030

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. RECENT DEVELOPMENT AND TRENDS

4.5. TECHNOLOGIES ANALYSIS

4.6. PRICING ANALYSIS

4.7. NEED GAP ANALYSIS

4.8. KEY CONFERENCES

4.9. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.10. INDUSTRY TRENDS

4.11. PORTER’S FIVE FORCES ANALYSIS

4.12. REGULATORY LANDSCAPE

4.12.1. NORTH AMERICA

4.12.2. EUROPE

4.12.3. ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. CLINICAL TRIAL ANALYSIS

6.1. ANALYSIS BY TRIAL REGISTRATION YEAR

6.2. ANALYSIS BY PHASE OF DEVELOPMENT

6.3. ANALYSIS BY TRIAL STATUS

6.4. ANALYSIS BY NUMBER OF PATIENTS ENROLLED

6.5. ANALYSIS BY STUDY DESIGN

6.6. ANALYSIS BY TYPE OF THERAPY / DRUG

6.7. ANALYSIS BY GEOGRAPHY

6.8. ANALYSIS BY KEY SPONSORS / COLLABORATORS

7. MOLECULAR DIAGNOSTICS MARKET, BY PRODUCT (2024-2030, USD MILLION)

7.1. REAGENT & KITS

7.2. SOFTWARE & SERVICES

7.3. INSTRUMENTS

8. MOLECULAR DIAGNOSTICS MARKET, BY TECHNOLOGY (2024-2030, USD MILLION)

8.1. AMPLIFICATION-BASED TECHNIQUES

8.1.1.POLYMERASE CHAIN REACTION (PCR)

8.1.2.NUCLEIC ACID SEQUENCE-BASED AMPLIFICATION (NASBA)

8.1.3.LOOP-MEDIATED ISOTHERMAL AMPLIFICATION (LAMP)

8.1.4.STRAND DISPLACEMENT AMPLIFICATION (SDA)

8.2. SEQUENCING TECHNOLOGIES

8.2.1. SANGER SEQUENCING (CAPILLARY ELECTROPHORESIS)

8.2.2. NEXT-GENERATION SEQUENCING (NGS) / HIGH-THROUGHPUT SEQUENCING (HTS)

8.2.3. THIRD-GENERATION SEQUENCING (LONG-READ SEQUENCING)

8.3. HYBRIDIZATION-BASED TECHNIQUES

8.3.1. MICROARRAY TECHNOLOGIES

8.3.2. FLUORESCENCE IN SITU HYBRIDIZATION (FISH)

8.3.3. IN SITU PCR / RT-PCR

8.4. ELECTROPHORESIS & SEPARATION TECHNIQUES

8.4.1. CAPILLARY ELECTROPHORESIS (CE)

8.4.2. GEL ELECTROPHORESIS

8.5. MASS SPECTROMETRY (MS)

8.6. BIOCHIP & MICROFLUIDIC TECHNOLOGIES

8.7. CRISPR-BASED DIAGNOSTICS

8.8. OTHER & EMERGING TECHNOLOGIES

9. MOLECULAR DIAGNOSTICS MARKET, BY SAMPLE (2024-2030, USD MILLION)

9.1. BLOOD

9.2. SALIVA

9.3. URINE

9.4. OTHER SPECIMENS

10. MOLECULAR DIAGNOSTICS MARKET, BY APPLICATION (2024-2030, USD MILLION)

10.1. INFECTIOUS DISEASE DIAGNOSTICS

10.2. CANCER DIAGNOSTICS & MANAGEMENT

10.3. GENETIC & HEREDITARY DISEASE DIAGNOSTICS

10.4. PHARMACOGENOMICS & DRUG RESPONSE

10.5. PRENATAL & NEWBORN SCREENING

10.6. FORENSIC & IDENTITY TESTING

11. MOLECULAR DIAGNOSTICS MARKET, BY END USER (2024-2030, USD MILLION)

11.1. HOSPITALS & CLINICS

11.2. DIAGNOSTICS LABORATORIES

11.3. OTHER END USERS

12. MOLECULAR DIAGNOSTICS MARKET, BY REGION (2024-2030, USD MILLION)

12.1. NORTH AMERICA

12.1.1. US

12.1.2. CANADA

12.2. EUROPE

12.2.1. GERMANY

12.2.2. FRANCE

12.2.3. SPAIN

12.2.4. ITALY

12.2.5. UK

12.2.6. REST OF THE EUROPE

12.3. ASIA-PACIFIC

12.3.1. CHINA

12.3.2. JAPAN

12.3.3. INDIA

12.3.4. AUSTRALIA AND NEW ZEALAND

12.3.5. SOUTH KOREA

12.3.6. REST OF THE ASIA-PACIFIC

12.4. MIDDLE EAST AND AFRICA

12.5. LATIN AMERICA

13. COMPETITIVE ANALYSIS

13.1. REVENUE ANALYSIS

13.2. KEY PLAYERS FOOTPRINT ANALYSI

13.3. MARKET SHARE ANALYSIS (2023/2024)

13.4. REGIONAL SNAPSHOT OF KEY PLAYERS

13.5. R&D EXPENDITURE OF KEY PLAYERS

13.6. BRAND/ PRODUCT COMPARISON

14. COMPANY PROFILES

14.1. F. HOFFMANN – LA ROCHE LTD. (SWITZERLAND)

14.1.1. BUSINESS OVERVIEW

14.1.2. PRODUCT PORTFOLIO

14.1.3. FINANCIAL SNAPSHOT

14.1.4. RECENT DEVELOPMENTS

14.1.4.1. MERGER/ACQUISITIONS

14.1.4.2. PRODUCT APPROVAL/LAUNCHES

14.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

14.1.4.4. EXPANSIONS

14.2. ABBOTT (US)

14.3. SIEMENS HEALTHINEERS (GERMANY)

14.4. THERMO FISHER SCIENTIFIC INC (US)

14.5. BIOMÉRIEUX (FRANCE)

14.6. DANAHER CORPORATION (US)

14.7. QIAGEN N.V. (GERMANY)

14.8. MYRIAD GENETICS INC. (US)

14.9. REVVITY (US)

14.10. HOLOGIC, INC (US)

14.11. ILLUMINA, INC (US)

14.12. OTHER PLAYERS

14.12.1. GENETIC SIGNATURES (AUSTRALIA)

14.12.2. AGILENT TECHNOLOGIES, INC. (US)

14.12.3. MDXHEALTH (BELGIUM)

14.12.4. BIOCARTIS (BELGIUM)

14.12.5. TBG DIAGNOSTICS LIMITED (AUSTRALIA)

14.12.6. HTG MOLECULAR DIAGNOSTICS, INC. (US)

14.12.7. VELA DIAGNOSTICS (SINGAPORE)

14.12.8. AMOY DIAGNOSTICS CO., LTD. (CHINA)

14.12.9. ELITECHGROUP (FRANCE)

14.12.10. MOLBIO DIAGNOSTICS PVT. LTD. (INDIA)

14.12.11. GENEOMBIO TECHNOLOGIES (INDIA)

14.12.12. SAVYON DIAGNOSTICS (ISRAEL)

14.12.13. UNIOGEN OY (FINLAND)

14.12.14. BECTON, DICKINSON AND COMPANY (US)

14.12.15. GRIFOLS, S.A. (SPAIN)

14.12.16. QUIDELORTHO CORPORATION (US)

14.12.17. DIASORIN S.P.A. (ITALY)

14.12.18. EXACT SCIENCES CORPORATION (US)

15. APPENDIX

15.1. INDUSTRY SPEAK

15.2. QUESTIONNAIRE/DISCUSSION GUIDE

15.3. AVAILABLE CUSTOM WORK

15.4. ADJACENT STUDIES

15.5. AUTHORS

The molecular diagnostics market encompasses the research, development, production, and distribution of tests that analyse genetic material—DNA and RNA—to detect and quantify specific nucleic acid sequences associated with diseases, pathogens, or genetic traits. These assays are fundamental to applications ranging from identifying infectious agents and screening for genetic disorders to guiding cancer therapy through companion diagnostics and enabling pharmacogenomics. The scope includes the development of sophisticated reagents (like PCR primers and probes, NGS libraries), specialized instruments (such as thermal cyclers and sequencers), bioinformatics platforms for data interpretation, and rigorous quality control processes to ensure accuracy and reproducibility, all adhering to stringent regulatory standards like FDA, CE-IVD, and CLIA.

Driven by the escalating global burden of infectious diseases and cancer, the demand for precise molecular insights, and the burgeoning field of personalized medicine, molecular diagnostics have become indispensable in modern healthcare and life sciences. The market is characterized by rapid technological evolution, including advancements in Next-Generation Sequencing (NGS), digital PCR, and rapid PCR platforms, alongside the increasing complexity of data analysis and interpretation. This landscape involves navigating complex regulatory pathways for genetic tests and ensuring robust validation across diverse clinical and research settings. With molecular testing playing an increasingly critical role in early disease detection, treatment selection, and population health management, the market continues to innovate, offering faster, more comprehensive, and more accessible genetic testing solutions, driving progress in clinical diagnostics, research, and specialized areas like prenatal testing and pharmacogenomics.

FIGURE: MOLECULAR DIAGNOSTICS MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the molecular diagnostics market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the molecular diagnostics technology market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the molecular diagnostics market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major manufacturers offering various molecular diagnostics will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of molecular diagnostics market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size using the market size estimation processes the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the molecular diagnostics market industry.