The global wearable technology market was valued at USD 80 billion in 2024 and is projected to reach USD 185 billion by 2030, expected to grow at a CAGR of 15% during the forecast period, 2025-2030.

Key driving factors of the wearables technology market include increasing consumer demand for health and fitness monitoring, rapid advancements in sensor and connectivity technologies, growing integration with healthcare systems, and expanding applications across wellness, medical, and enterprise sectors.

Challenges in the wearables technology domain include concerns over data privacy and security, limited battery life and device durability, regulatory complexities for medical-grade devices, and market saturation in mature segments.

Smart watches have held the largest share in the market since 2022, with North America dominating the regional market share.

Key players operating in global wearables technology sector are, Samsung, Xiaomi, Huawei Technology Co., Ltd., Garmin Ltd., Sony Corporation, LG Electronics, Microsoft, Lenovo, Meta, Amazon Inc., Oppo, among others.

Global Wearable Technology market is anticipated to reach USD 185 billion by 2030 from USD 80 billion in 2024, growing at an annualized rate of 15% during the period, 2025-2030 | Emerging economies like India, China, Brazil, South Korea, present significant growth opportunities for the wearable technology market. India is anticipated to show the highest growth rate in the Asia-Pacific region | ASIA-PACIFIC Growing research and reliance on wearable technology in emerging countries is expected to provide lucrative opportunities for market players. |

The wearable technology market is being revolutionized by breakthroughs in semiconductor design, including the adoption of Gate-All-Around transistors and advanced chip packaging, enabling smaller, more energy-efficient, and powerful devices that support AI-driven features and extended battery life critical for next-gen wearables like smart glasses and smart fabrics | Convergence of edge computing and generative AI in wearables is revolutionizing the devices from basic trackers to smart personal assistants with real-time health scoring, contextual suggestions, and conversational interfaces, and hence increasing user engagement while broadening the use cases to lifestyle and productivity areas. Fashion and technology convergence, facilitated by improvements in flexible sensors and smart textiles, is driving wearables into everyday clothing, allowing continuous biometric sensing without the loss of comfort or fashion, creating new markets in sports, rehabilitation, and occupational safety while lowering user adoption barriers |

Drivers: Rapid advancements in semiconductor technology and sensor miniaturization are enabling the development of more powerful, compact, and energy-efficient wearable devices with advanced features and longer battery life

Emerging semiconductor technology advancements, including Gate-All-Around (GAA) transistor innovation and new chip packaging, are enabling makers to create more compact, powerful chips that use less power, which immediately helps wearable devices. Sensor miniaturization makes it possible to pack several advanced sensors, such as ECG, SpO2, and temperature, into small devices without compromise on comfort or battery life. For instance, the newest Apple Watch uses next-generation silicon and compact sensors to enable constant health monitoring, sophisticated fitness tracking, and long battery life all within a thin form factor

Opportunities: Expanding integration of wearables with IoT ecosystems and smart products—such as smart home devices, AR/VR headsets, and enterprise solutions—offers new avenues for innovation and market growth beyond health and fitness

Wider integration of wearables with IoT systems and intelligent products is turning these devices into a hub of connected living, facilitating smooth interaction with smart home appliances, AR/VR headsets, and enterprise offerings for productivity and security. For instance, a smartwatch now can manage home lighting, obtain real-time health notifications, and be synchronized with AR glasses for extended navigation or hands-free office guidance, demonstrating how wearables are progressing much beyond fitness to fuel smarter, more connected lives

Challenges: Data privacy and security concerns, especially as wearables collect increasingly sensitive personal and biometric information, remain a significant barrier to widespread adoption and user trust

Since wearables capture and send extremely sensitive biometric and personal information—heart rate, sleeping patterns, and location—they make for compelling attack targets for cyberattackers and data thieves, thus posing very relevant privacy and security concerns. To illustrate, researchers have shown that fitness tracker vulnerabilities can enable attackers to tamper with health information or leverage compromised devices as doors to extended healthcare networks, potentially leading to perilous treatment prescriptions or extensive system intrusions. This highlights the desperate need for strong encryption, secure data protocols, and explicit user consent to preserve confidence and facilitate secure use of wearable technology

The global wearable technology market, spanning smartwatches, fitness trackers, smart clothing, and enterprise wearables, is experiencing robust growth driven by rising health awareness, rapid advancements in sensor and semiconductor technologies, and expanding integration with IoT and AR/VR applications. Valued at USD 80 billion in 2024, the market is projected to reach USD 185 billion by 2030, expanding at a CAGR of 15%. Key drivers include increasing consumer demand for health and lifestyle monitoring, innovation in device form factors, and strong investment from leading technology companies, with North America maintaining the largest market share and Asia Pacific emerging as a major growth engine

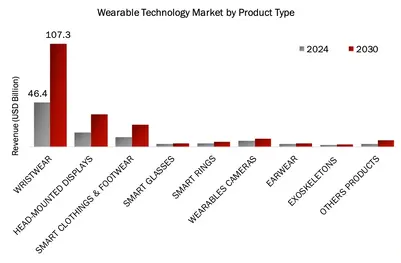

Wrist-Wear segment dominated the wearable technology Market by Product type in 2024

The wrist-wear segment led the wearable technology market in 2024 with more than 58% of global revenue, driven by growing demand for health and fitness monitoring, lifestyle tracking, and effortless smartphone connectivity. Ongoing evolution in sensor accuracy and battery life has converted smartwatches such as the Apple Watch into health-oriented smart companions that are able to monitor ECG, blood oxygen level, and sleep duration, and these have become an absolute necessity for millions of consumers across the globe.

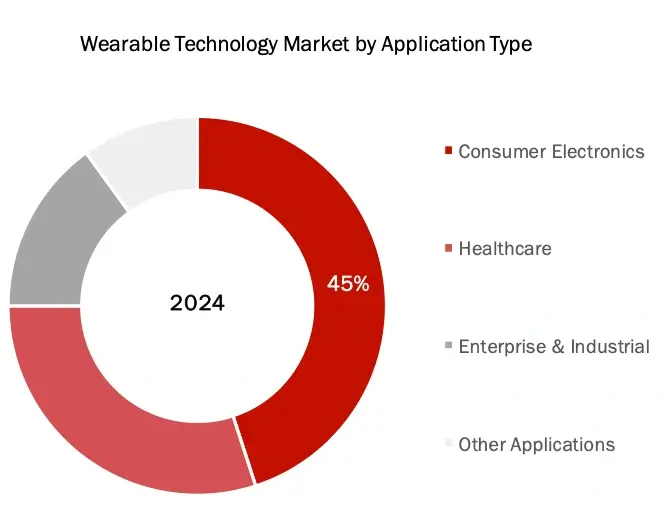

Consumer Electronics held the largest market share in 2024, accounting for a significant 45% market share in the Wearable Technology market

Consumer electronics was the category with the largest market share in the wearables technology market in 2024, contributing to around 45% of overall revenue, as brands such as Samsung fueled adoption with a wide range of smartwatches and fitness bands at various price levels. For instance, Samsung delivered 11.5 million wrist-worn wearables during the first three quarters of 2024, riding on items such as the Galaxy Watch Ultra and Galaxy Fit 3 in order to target entry-level as well as premium customers, cementing its powerful position in the international market.

North America dominated the market share in the wearable technology space during the forecast period (2025–2030), led by the concentration of strong market leaders like Apple, Alphabet, Garmin, and Fitbit within the region, along with a highly tech-savvy population willing to incorporate the latest innovation. High levels of urbanization, pervasive internet connectivity, and strong digital infrastructure have helped drive the adoption of smartwatches, fitness bands, and wearable medical devices in consumer as well as enterprise markets. Also, North America’s sophisticated R&D environment and early adoption of AI, IoT, and cloud-enabled analytics have helped drive quick product innovation and integration, solidifying the region’s position as a leader in wearables for health, lifestyle, and productivity applications

Furthermore, the US with USD 24 billion market in 2024, holds majority share in the global wearable technology market and is likely to remain the leading region growing a CAGR of 15.4% within this market, during the forecast period.

Major players operating in Wearable Technology market are:

Sources: Secondary Research

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

Particulars | Details |

Report | Wearables Technology Market |

Forecast Period | 2025-2030 |

Base Year | 2024 |

Format | |

Market Size (2024) | USD 80 Billion |

CAGR (2025-2030) | 15% |

Number of Pages | 171 |

Number of Tables | 160 |

Number of Figures | 34 |

Key Segments | Wearables Technology Market Products Outlook (Wristwear, Head-mounted Displays, Smart Clothing & Footwear, Smart Glasses, Smart Rings, Wearables Cameras, Earwear, Exoskeletons) Wearables Technology Market Operation Outlook (AI, Conventional) Wearables Technology Market Application Outlook (Consumer Electronics, Healthcare, Enterprise & Industrial) Wearables Technology Market Distribution Channel Outlook (Online channels, Direct-to-consumers, Retail shops, Hospitals and clinics) |

Regions Covered | § North America: US and Canada § Europe: Germany, UK, France, Italy, Spain, and Rest of the Europe § Asia-Pacific: China, Japan, India, South Korea, Australia and New Zealand, and Rest of the Asia-Pacific § Latin America § Middle East and Africa |

Key Players Covered (Majority Share Holders) | Apple Inc. (US), Samsung (South Korea), Xiaomi (China), Huawei Technology Co., Ltd. (China), Garmin Ltd. (US/Switzerland), Sony Corporation (Japan), LG Electronics (South Korea), Microsoft (US), Lenovo (China/US), Meta (US), Amazon Inc. (US), Oppo (China) |

Other Players | Vuzix (US), Motorola Mobility LLC (US), Intellitix (Canada), Innominds Software India Private Limited (India), Comau (Italy), Hyundai Motor Company (South Korea), Cyberdyne Inc. (Japan), Ekso Bionics (US), Mclear Ltd. (UK), Jakcom Technology Co., Ltd. (China), Token (US), Infineon Technologies AG (Germany), Qualcomm Technologies, Inc. (US), Adidas AG (Germany), Fossil Group, Inc. (US), Lifesense Group B.V. (Netherlands), Dynabook Americas, Inc. (US), Optinvent (France), Seiko Epson Corporation (Japan), Humane Inc. (US) |

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. WEARABLE TECHNOLOGY: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. NEED GAP ANALYSIS

4.5. KEY CONFERENCES

4.6. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.7. INDUSTRY TRENDS

4.8. PORTER’S FIVE FORCES ANALYSIS

4.9. REGULATORY LANDSCAPE

4.9.1.NORTH AMERICA

4.9.2.EUROPE

4.9.3.ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. GLOBAL WEARABLE TECHNOLOGY MARKET BY, PRODUCT (2025-2030, USD MILLION)

6.1. WRISTWEAR

6.1.1.SMARTWATCHES

6.1.2.FITNESS TRACKERS

6.2. HEAD-MOUNTED DISPLAYS

6.2.1.AUGMENTED REALITY

6.2.2.VIRTUAL REALITY

6.2.3.OTHER HEAD-MOUNTED DISPLAYS

6.3. SMART CLOTHINGS & FOOTWEAR

6.3.1.SMART SHOES

6.3.2.SMART VESTS

6.3.3.OTHER SMART CLOTHINGS & FOOTWEAR

6.4. SMART GLASSES

6.5. SMART RINGS

6.6. WEARABLES CAMERAS

6.7. EARWEAR

6.8. EXOSKELETONS

6.9. OTHERS PRODUCTS

7. GLOBAL WEARABLES TECHNOLOGY TREATMENT MARKET BY, OPERATION (2025-2030, USD MILLION)

7.1. AI-BASED

7.1.1.ON-DEVICE AI

7.1.2.CLOUD-BASED AI

7.2. CONVENTIONAL

8. GLOBAL WEARABLES TECHNOLOGY MARKET BY, APPLICATION (2025-2030, USD MILLION)

8.1. CONSUMER ELECTRONICS

8.1.1.FITNESS & SPORTS

8.1.2.INFOTAINMENT & MULTIMEDIA

8.1.3.GARMENTS & FASHION

8.1.4.MULTIFUNCTION

8.2. HEALTHCARE

8.2.1.CLINICAL

8.2.2.NON-CLINICAL

8.3. ENTERPRISE & INDUSTRIAL

8.3.1.LOGICAL, PACKAGING & WAREHOUSE

8.3.2.OTHER ENTERPRISE & INDUSTRIAL

8.4. OTHERS APPLICATIONS

9. GLOBAL WEARABLES TECHNOLOGY MARKET BY, DISTRIBUTION CHANNEL (2025-2030, USD MILLION)

9.1. ONLINE CHANNELS

9.2. DIRECT-TO-CONSUMERS

9.3. RETAIL SHOPS

9.4. HOSPITALS AND CLINICS

10. GLOBAL WEARABLES TECHNOLOGY MARKET BY, REGION (2025-2030, USD MILLION)

10.1. NORTH AMERICA

10.1.1. US

10.1.2. CANADA

10.2. EUROPE

10.2.1. GERMANY

10.2.2. FRANCE

10.2.3. SPAIN

10.2.4. ITALY

10.2.5. UK

10.2.6. REST OF THE EUROPE

10.3. ASIA-PACIFIC

10.3.1. CHINA

10.3.2. JAPAN

10.3.3. INDIA

10.3.4. AUSTRALIA AND NEW ZEALAND

10.3.5. SOUTH KOREA

10.3.6. REST OF THE ASIA-PACIFIC

10.4. MIDDLE EAST AND AFRICA

10.5. LATIN AMERICA

11. COMPETITIVE ANALYSIS

11.1. REVENUE ANALYSIS

11.2. KEY PLAYERS FOOTPRINT ANALYSIS

11.3. MARKET SHARE ANALYSIS (2023/2024)

11.4. REGIONAL SNAPSHOT OF KEY PLAYERS

11.5. R&D EXPENDITURE OF KEY PLAYERS

11.6. BRAND/ PRODUCT COMPARISON

12. COMPANY PROFILES

12.1. APPLE INC.

12.1.1. BUSINESS OVERVIEW

12.1.2. PRODUCT PORTFOLIO

12.1.3. FINANCIAL SNAPSHOT

12.1.4. RECENT DEVELOPMENTS

12.1.4.1. MERGER/ACQUISITIONS

12.1.4.2. PRODUCT APPROVAL/LAUNCHES

12.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

12.1.4.4. EXPANSIONS

12.2. SAMSUNG

12.3. XIAOMI

12.4. HUAWEI TECHNOLOGY CO., LTD.

12.5. IMAGINE MARKETING LIMITED

12.6. GARMIN LTD.

12.7. SONY CORPORATION

12.8. LG ELECTRONICS

12.9. ALPHABET INC.

12.10. MICROSOFT

12.11. LENOVO

12.12. META

12.13. AMAZON INC.

12.14. OPPO

12.15. OTHER PLAYERS

12.15.1. VUZIX

12.15.2. MOTOROLA MOBILITY LLC

12.15.3. INTELLITIX

12.15.4. INNOMINDS SOFTWARE INDIA PRIVATE LIMITED

12.15.5. COMAU

12.15.6. HYUNDAI MOTOR COMPANY

12.15.7. CYBERDYNE INC.

12.15.8. EKSO BIONICS

12.15.9. MCLEAR LTD.

12.15.10. JAKCOM TECHNOLOGY CO., LTD.

12.15.11. TOKEN

12.15.12. INFINEON TECHNOLOGIES AG

12.15.13. QUALCOMM TECHNOLOGIES, INC.

12.15.14. ADIDAS AG.

12.15.15. FOSSIL GROUP, INC.

12.15.16. LIFESENSE GROUP B.V.

12.15.17. DYNABOOK AMERICAS, INC.

12.15.18. OPTINVENT

12.15.19. SEIKO EPSON CORPORATION

12.15.20. HUMANE INC.

13. APPENDIX

13.1. INDUSTRY SPEAK

13.2. QUESTIONNAIRE/DISCUSSION GUIDE

13.3. AVAILABLE CUSTOM WORK

13.4. ADJACENT STUDIES

13.5. AUTHORS

Introduction

Market Definition

The wearables technology market comprises electronic devices designed to be worn on the body—such as smartwatches, fitness trackers, and smart clothing—that integrate advanced sensors, software, and connectivity to monitor health, track fitness, enable communication, and provide real-time data. These devices, often part of the Internet of Things (IoT), are driven by growing consumer demand for health and fitness tracking, advancements in sensor and miniaturization technologies, and expanding applications across consumer electronics, healthcare, and enterprise sectors

FIGURE : WEARABLES TECHNOLOGY MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

•Device Manufacturers

•Component and Technology Suppliers (sensor, chip, battery, and connectivity module providers)

•Software Developers (operating systems, health and fitness app developers)

•Healthcare Providers (hospitals, clinics, telemedicine companies)

•Pharmaceutical Companies

•Biotechnology Firms

•Insurance Providers (private and public health insurers)

•Regulatory Authorities (FDA, EMA, etc.)

•Research Institutions and Universities

•Patient Advocacy Groups

•Pharmacy and Distribution Networks (wholesale distributors, pharmacies, retail channels)

•Policy Makers (government bodies, health ministries, legislators)

•Contract Research Organizations (CROs)

•Investors (venture capitalists, private equity firms)

Key objectives of the Study

•To define, describe, analyze, segment, and forecast the wearables technology market by products, by operation and by applications.

•To describe and forecast the market for four key regions: North America, Europe, Asia Pacific, and Rest of the World.

•To provide detailed information regarding key drivers, restraints, opportunities, and challenges influencing market growth

•To strategically analyze the micro indicators with respect to individual growth trends, prospects, and contributions to the overall market size

•To analyze opportunities for stakeholders in the wearables technology treatment industry and emphasize on competitive landscape of the market.

•To develop competitive benchmarking of the key market players based on technology specifications and end users.

•To strategically profile key players and comprehensively analyze their product portfolio offerings, and core competencies

•To analyze competitive developments, such as launches and approvals, agreements, mergers and acquisitions, partnerships, joint ventures, investments and expansions, and collaborations, wearables technology domain.

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the wearables technology market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the wearables technology market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the wearables technology market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major manufacturers offering various wearables technology will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be

extrapolated to arrive at the global market value of each type of segment. The market value of wearables technology market will also split into various segments and sub segments at the region level based on:

•Product and services mapping of various players for each type of wearables technology market at the regional-level

•Relative adoption pattern of the testing devices market among key application segments at the regional-level

•Detailed primary research to gather qualitative and quantitative information related to segments and sub segments at the regional level.

•Detailed secondary research to gauge the prevailing market trends at the regional level

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the wearables technology market industry.