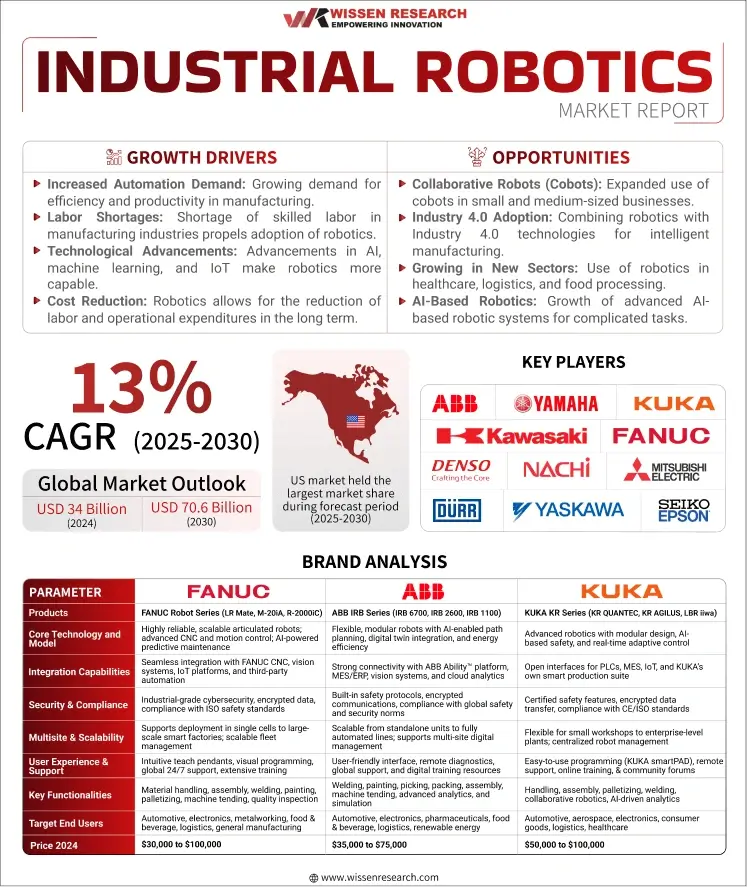

Wissen Research analysed that the global industrial robotics market was valued at USD 34 billion in 2024 and is projected to reach USD 70.6 billion by 2030, expected to grow at a CAGR of 13% during the forecast period, 2025-2030.

Articulated robot segment is expected to register the largest growth rate in the industrial robotics market during the forecast period (2025-2030), with North America dominating the regional market share.

Global Industrial robotics market is anticipated to reach USD 70.6 billion by 2030 from USD 34 billion in 2024, growing at an annualized rate of 13% during the period, 2025-2030 | East Asia, led by China, Japan, and South Korea, dominates global market growth, driven by large-scale investments in smart factories, rising labor costs, and government support for automation, with the region expected to account for over two-thirds of global revenue by 2025 | Trans-Atlantic North America and Europe continue to be ahead of the game in terms of innovation, developing flexible, modular robots and AI-based analytics, while developing markets in Southeast Asia, Latin America, and Eastern Europe are more and more embracing industrial robots to improve productivity, comply with regulations, and deal with labor shortages |

The market for industrial robotics is being transformed by the swift developments in AI, machine vision, and sensor technologies that are making robots capable of executing sophisticated, adaptive tasks with higher autonomy and accuracy in manufacturing, electronics, and logistics industries | The growth in collaborative robots (cobots) is making automation more accessible for small and medium-sized businesses with the promise of safer human-robot interaction, simplified programming, and cost-effective deployment, while robotics platforms in the cloud are facilitating real-time monitoring, predictive maintenance, and remote optimization. Major challenges are high capital expenses, complexity of integration with existing systems, and the requirement for upskilling the workforce, which can discourage adoption in smaller manufacturers and countries with poor digital infrastructure |

Drivers: Transforming Manufacturing with AI, Automation, and Agility

The market for industrial robotics is booming as manufacturers in automotive, electronics, food & beverages, and logistics industries adopt cutting-edge automation to enhance productivity, guarantee uniform quality, and contain operating expenses. Robotics based on AI, machine vision, and IoT are making robots smarter, more adaptive, predictive maintenance capable, and decision-making in real-time. The advent of collaborative robots (cobots) and need for reprogrammable, flexible systems are enabling organizations to quickly respond to changing production requirements and stay competitive in a globally dynamic market.

Opportunities: Unlocking Growth in Emerging and Evolving Industrial Hubs

Faster-than-expected investment in smart factories and state-sponsored automation programs, especially in Asia Pacific dominated by China, Japan, and South Korea, are creating new opportunities for industrial robotics. Cloud robotics, robot-as-a-service (RaaS) offerings, and modular approaches are bringing automation to small and medium-sized businesses, whereas sustainability imperatives and labor availability challenges are propelling adoption in fresh verticals and geographies.

Challenges: Cost, Integration, and Workforce Readiness

High initial investment and integration complexity continue to be major hindrances, particularly for SMEs and existing plants. Interoperability with legacy systems, cyber security threats, and the requirement for experienced operators and continuous workforce upskilling continue to pose challenges. Regional differences in digital infrastructure and standards also complicate scalability and deployment, necessitating market entry and expansion strategies that need to be adapted.

The world industrial robotics market, encompassing a wide range of automated, programmable devices employed in manufacturing, assembly, material handling, and logistics, is witnessing a fast-paced growth as industries hasten automation to increase productivity as well as quality. Worth USD 34 billion in 2024, the market is expected to become USD 70.6 billion by 2030, registering a CAGR of 13%. Pivotal growth drivers are higher adoption of AI, machine vision, and IoT-connected robotics, increasing labor costs, and the imperative for operational efficiency in the automotive, electronics, food & beverage, and logistics industries. Asia Pacific dominates the market with China, Japan, and South Korea providing most of the global installations, followed by North America and Europe, where growth is on the ascendant as driven by investment in smart factories and collaborative robots. The development of the market is also influenced by developments in modular design, cloud robotics, and robot-as-a-service (RaaS) schemes, which make automation available to large corporations and small-to-medium-sized manufacturers alike.

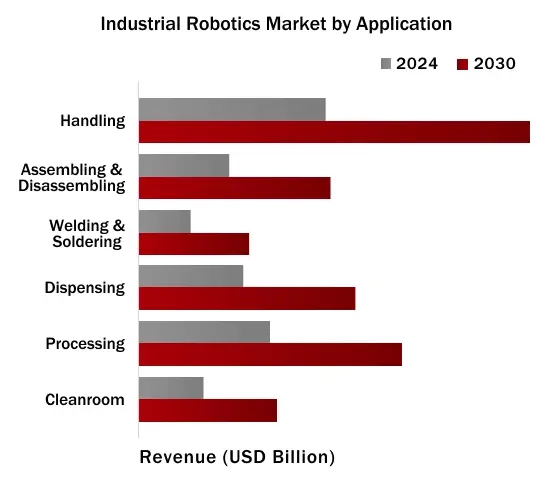

Handling segment dominated the Industrial Robotics Market by Application in 2024

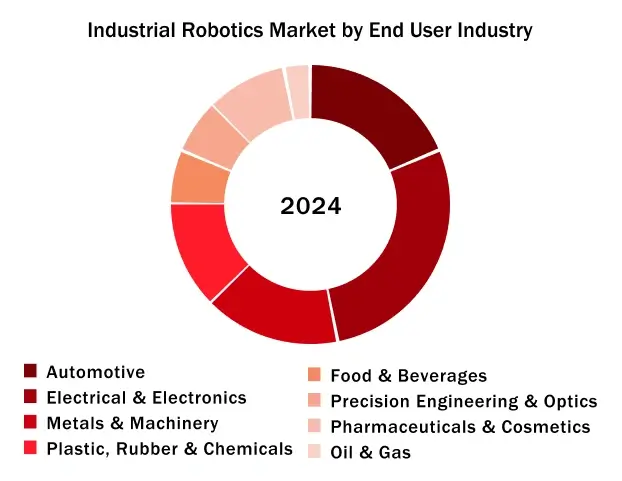

Electrical and Electronics Segment held the largest market share in 2024, accounting for a significant market share in Industrial Robotics market by End User Industry

North America held the largest market share in Industrial Robotics Market in the forecast period (2025-2030)

North America accounted for the highest market share in the Industrial Robotics Market throughout the forecast period (2025–2030) due to strong uptake of sophisticated automation in sectors like automotive, aerospace, and logistics. Businesses within the region are taking advantage of robotics to advance productivity, precision, and cope with ongoing labor shortages, especially in high-skill manufacturing positions. For instance, American automobile makers have considerably increased the utilization of robotic arms for assembly and welding, while logistics companies employ robots for auto-picking and packing to address e-commerce order volumes. Industry 4.0-friendly government programs and continuous investments in reshoring manufacturing facilities have also further boosted the adoption of industrial robots in North America, making it the market leader worldwide.

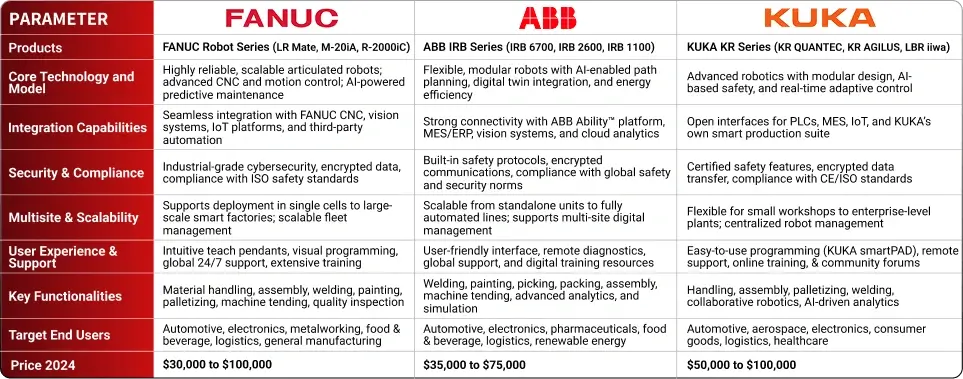

Major players operating in industrial robotics market are:

Note: Above pricing are collected from website and third party sellers.

Sources: Secondary Research

“AI-driven robotics and advanced machine vision are transforming industrial automation, enabling unprecedented precision, flexibility, and efficiency across manufacturing lines.”

Chief Technology Officer – Leading Robotics Manufacturer (Europe)

“Rising labor costs and persistent workforce shortages are accelerating the adoption of industrial robots, especially in automotive, electronics, and logistics sectors.”

Director of Operations – Global Automotive OEM (Asia-Pacific)

“Interoperability and seamless integration with IoT platforms are now essential, as factories demand real-time data, predictive maintenance, and scalable automation solutions.”

VP, Product Development – Industrial Automation Solutions Provider (North American)

“Strategic investments in collaborative robots (cobots) and digital twins are reshaping production environments, allowing for safer human-robot collaboration and rapid process optimization”

Head of Innovation – Advanced Manufacturing Consortium (Asia Pacific)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

Particulars | Details |

Report | Industrial Robotics Market |

Forecast Period | 2025-2030 |

Base Year | 2024 |

Format | |

Market Size (2024) | USD 34 Billion |

CAGR (2025-2030) | 13% |

Number of Pages | 165 |

Number of Tables | 155 |

Number of Figures | 34 |

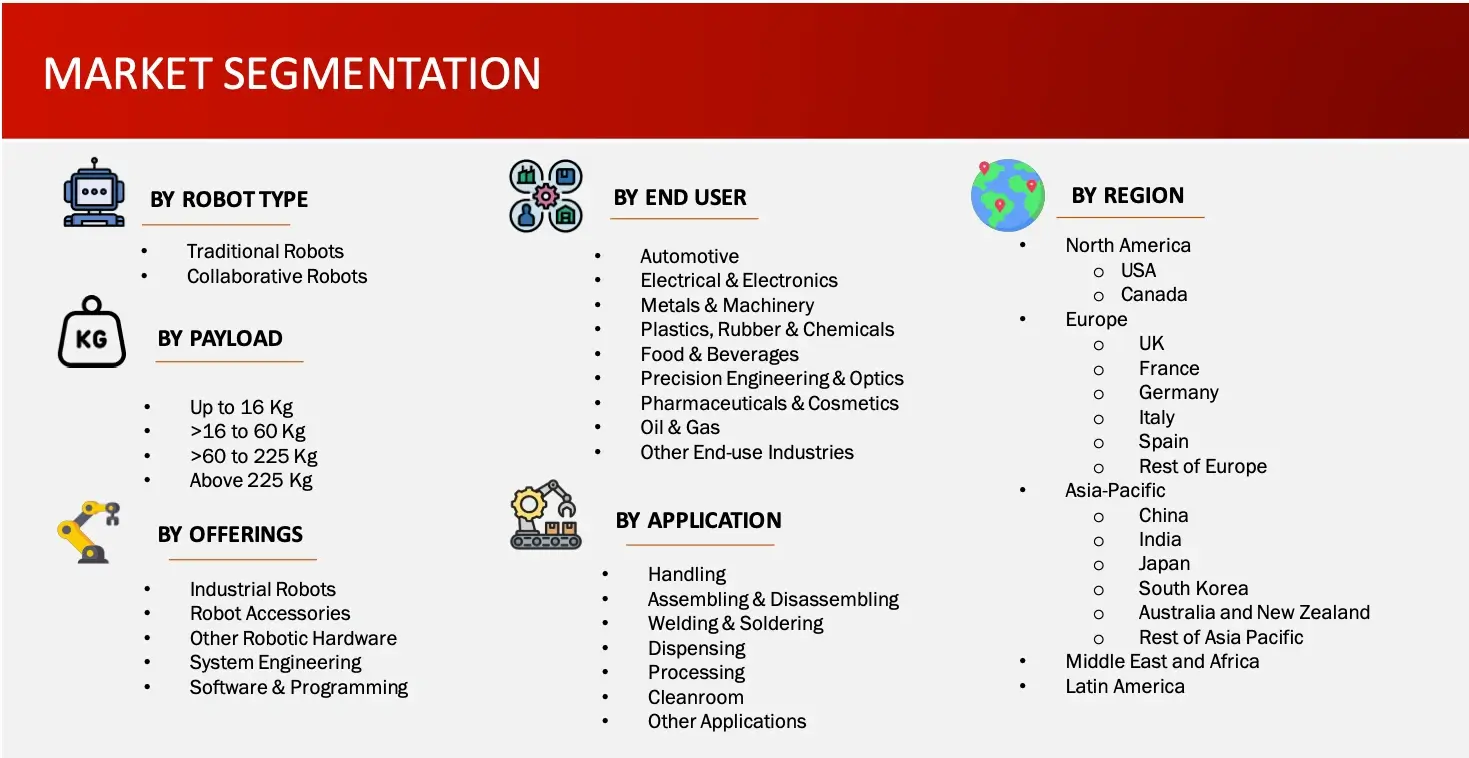

Key Segments | Industrial Robotics Market Robot Type Outlook (Traditional Robots, Collaborative Robots) Industrial Robotics Market Payload Outlook (Up to 16 Kg, >16 to 60 Kg, >60 to 225 Kg, Above 225 Kg) Industrial Robotics Market Offerings Outlook (Industrial Robots, Robot Accessories, Other Robotic Hardware, System Engineering, Software & Programming) Industrial Robotics Market Application Outlook (Handling, Assembling & Disassembling, Welding & Soldering, Dispensing, Processing, Cleanroom, Other Applications) Industrial Robotics Market End User Outlook (Automotive, Electrical & Electronics, Metals & Machinery, Plastics, Rubber & Chemicals, Food & Beverages, Precision Engineering & Optics, Pharmaceuticals & Cosmetics, Oil & Gas, Other End-use Industries) |

Regions Covered | § North America: US and Canada § Europe: Germany, UK, France, Italy, Spain, and Rest of the Europe § Asia-Pacific: China, Japan, India, South Korea, Australia and New Zealand, and Rest of the Asia-Pacific § Latin America § Middle East and Africa |

Key Players Covered (Majority Share Holders) | ABB (Switzerland), Yaskawa Electric Corporation (Japan), Fanuc Corporation (Japan), Kuka AG (Germany), Mitsubishi Electric Corporation (Japan), Kawasaki Heavy Industries (Japan), Denso Corporation (Japan), Nachi-Fujikoshi Corp (Japan), Seiko Epson Corporation (Japan), Dürr Group (Germany) |

Other Players | Yamaha Motor Co., Ltd. (Japan), Estun Automation Co., Ltd. (China), Shibaura Machine (Japan), Dover Corporation (Us), Aurotek Corporation (Taiwan), Hirata Corporation (Japan), Rethink Robotics (Us), Franka Robotics Gmbh (Germany), Techman Robot Inc. (Taiwan), Bosch Rexroth AG (Germany), Universal Robots A/S (Denmark), Omron Corporation (Japan), Staubli International AG (Switzerland), Comau (Italy), B+M Surface Systems Gmbh (Germany), ICR Services (Us), IRS Robotics (Netherlands), HD Hyundai Robotics (South Korea), Siasun Robot & Automation Co., Ltd (China), Robotworx (Us) |

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. INDUSTRIAL ROBOTICS: OVERVIEW

4.1.1. INTRODUCTION

4.1.2.KEY FEATURES AND FUNCTIONALITIES

4.1.3.BENEFITS OF INDUSTRIAL ROBOTICS

4.1.4.TYPES OF INDUSTRIAL ROBOTICS

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. NEED GAP ANALYSIS

4.5. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.6. INDUSTRY TRENDS

4.7. PORTER’S FIVE FORCES ANALYSIS

4.8. REGULATORY LANDSCAPE

4.8.1.NORTH AMERICA

4.8.2.EUROPE

4.8.3.ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. GLOBAL INDUSTRIAL ROBOTICS MARKET, BY ROBOT TYPE (2025-2030, USD MILLION)

6.1. TRADITIONAL ROBOTS

6.1.1.ARTICULATED ROBOTS

6.1.2.SCARA ROBOTS

6.1.3.PARALLEL ROBOTS

6.1.4.CARTESIAN ROBOTS

6.1.5.CYLINDRICAL ROBOTS

6.1.6.OTHER TRADITIONAL ROBOTS

6.2. COLLABORATIVE ROBOTS

7. GLOBAL INDUSTRIAL ROBOTICS MARKET, BY PAYLOAD (2025-2030, USD MILLION)

7.1. UP TO 16 KG

7.2. >16 ΤΟ 60 KG

7.3. >60 ΤΟ 225 KG

7.4. ABOVE 225 KG

8. GLOBAL INDUSTRIAL ROBOTICS MARKET, BY OFFERINGS (2025-2030, USD MILLION)

8.1. INDUSTRIAL ROBOTS

8.2. ROBOT ACCESSORIES

8.2.1.END EFFECTORS

8.2.1.1. WELDING GUNS

8.2.1.2. GRIPPERS

8.2.1.3. TOOL CHANGERS

8.2.1.4. CLAMPS

8.2.1.5. SUCTION CUPS

8.2.1.6. OTHER END EFFECTORS

8.2.2.CONTROLLERS

8.2.3.DRIVE UNITS

8.2.3.1. HYDRAULIC DRIVES

8.2.3.2. ELECTRIC DRIVES

8.2.3.3. PNEUMATIC DRIVES

8.2.4.VISION SYSTEMS

8.2.5.SENSORS

8.2.6.POWER SUPPLY ACCESSORIES

8.2.7.OTHER ROBOT ACCESSORIES

8.3. OTHER ROBOTIC HARDWARE

8.3.1.SAFETY FENCING HARDWARE

8.3.2.FIXTURES TOOLS

8.3.3.CONVEYORS HARDWARE

8.4. SYSTEM ENGINEERING

8.5. SOFTWARE & PROGRAMMING

9. GLOBAL INDUSTRIAL ROBOTICS MARKET, BY APPLICATION (2025-2030, USD MILLION)

9.1. HANDLING

9.1.1.PICK & PLACE

9.1.2.MATERIAL HANDLING

9.1.3.PACKAGING & PALLETIZING

9.2. ASSEMBLING & DISASSEMBLING

9.3. WELDING & SOLDERING

9.4. DISPENSING

9.4.1.GLUING

9.4.2.PAINTING

9.4.3.FOOD DISPENSING

9.5. PROCESSING

9.5.1.GRINDING & POLISHING

9.5.2.MILLING

9.5.3.CUTTING

9.6. CLEANROOM

9.7. OTHER APPLICATIONS

10. GLOBAL INDUSTRIAL ROBOTICS MARKET, BY END-USE INDUSTRY (2025-2030, USD MILLION)

10.1. AUTOMOTIVE

10.2. ELECTRICAL & ELECTRONICS

10.3. METALS & MACHINERY

10.4. PLASTICS, RUBBER & CHEMICALS

10.5. FOOD & BEVERAGES

10.6. PRECISION ENGINEERING & OPTICS

10.7. PHARMACEUTICALS & COSMETICS

10.8. OIL & GAS

10.9. OTHER END-USE INDUSTRIES

11. GLOBAL INDUSTRIAL ROBOTICS MARKET, BY REGION (2025-2030, USD MILLION)

11.1. NORTH AMERICA

11.1.1. US

11.1.2. CANADA

11.2. EUROPE

11.2.1. GERMANY

11.2.2. FRANCE

11.2.3. SPAIN

11.2.4. ITALY

11.2.5. UK

11.2.6. REST OF THE EUROPE

11.3. ASIA-PACIFIC

11.3.1. CHINA

11.3.2. JAPAN

11.3.3. INDIA

11.3.4. AUSTRALIA AND NEW ZEALAND

11.3.5. SOUTH KOREA

11.3.6. REST OF THE ASIA-PACIFIC

11.4. MIDDLE EAST AND AFRICA

11.5. LATIN AMERICA

12. COMPETITIVE ANALYSIS

12.1. PRODUCT PIPELINE: INDUSTRIAL ROBOTICS

12.2. KEY PLAYERS FOOTPRINT ANALYSIS

12.3. MARKET SHARE ANALYSIS (2023/2024)

12.4. REGIONAL SNAPSHOT OF KEY PLAYERS

12.5. R&D EXPENDITURE OF KEY PLAYERS

13. COMPANY PROFILES

13.1. ABB (Switzerland)

13.1.1. BUSINESS OVERVIEW

13.1.2. PRODUCT PORTFOLIO

13.1.3. FINANCIAL SNAPSHOT

13.1.4. RECENT DEVELOPMENTS

13.1.4.1. MERGER/ACQUISITIONS

13.1.4.2. PRODUCT APPROVAL/LAUNCHES

13.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

13.1.4.4. EXPANSIONS

13.2. YASKAWA ELECTRIC CORPORATION (Japan)

13.3. FANUC CORPORATION (Japan)

13.4. KUKA AG (Germany)

13.5. MITSUBISHI ELECTRIC CORPORATION (Japan)

13.6. KAWASAKI HEAVY INDUSTRIES (Japan)

13.7. DENSO CORPORATION (Japan)

13.8. NACHI-FUJIKOSHI CORP (Japan)

13.9. SEIKO EPSON CORPORATION (Japan)

13.10. DÜRR GROUP (Germany)

13.11. OTHER PLAYERS

13.11.1. YAMAHA MOTOR CO., LTD. (Japan)

13.11.2. ESTUN AUTOMATION CO., LTD. (China)

13.11.3. SHIBAURA MACHINE (Japan)

13.11.4. DOVER CORPORATION (US)

13.11.5. AUROTEK CORPORATION (Taiwan)

13.11.6. HIRATA CORPORATION (Japan)

13.11.7. RETHINK ROBOTICS (US)

13.11.8. FRANKA ROBOTICS GMBH (Germany)

13.11.9. TECHMAN ROBOT INC. (Taiwan)

13.11.10. BOSCH REXROTH AG (Germany)

13.11.11. UNIVERSAL ROBOTS A/S (Denmark)

13.11.12. OMRON CORPORATION (Japan)

13.11.13. STAUBLI INTERNATIONAL AG (Switzerland)

13.11.14. COMAU (Italy)

13.11.15. B+M SURFACE SYSTEMS GMBH (Germany)

13.11.16. ICR SERVICES (US)

13.11.17. IRS ROBOTICS (Netherlands)

13.11.18. HD HYUNDAI ROBOTICS (South Korea)

13.11.19. SIASUN ROBOT & AUTOMATION CO., LTD (China)

13.11.20. ROBOTWORX (US)

14. APPENDIX

14.1. INDUSTRY SPEAK

14.2. QUESTIONNAIRE/DISCUSSION GUIDE

14.3. AVAILABLE CUSTOM WORK

14.4. ADJACENT STUDIES

14.5. AUTHORS

15. REFERENCES

The market for industrial robotics is a wide variety of programmable, automated equipment that is capable of undertaking repetitive, high-precision, and dangerous jobs in the manufacturing and industrial sectors. The robots are used in a wide array of industries such as automotive, electronics, metals, food & beverages, pharmaceuticals, and logistics to automate tasks like assembly, welding, painting, material handling, packaging, and inspection. The range spans a broad portfolio of robot models, such as articulated, SCARA, delta, Cartesian, and cobots, offered in fixed and mobile forms. It is provided as a single unit or integrated into larger automation solutions, with implementation models from conventional on-premise deployments to sophisticated, cloud-based platforms. Industrial robots are designed to increase productivity, enhance product quality, lower operational expenses, and improve workplace safety. Market expansion is driven by continued developments in robotics technology e.g., artificial intelligence, machine vision, and IoT connectivity along with escalating labor costs, growing need for flexible production, and worldwide movement toward smart factories and Industry 4.0 transformation.

FIGURE: INDUSTRIAL ROBOTICS MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the industrial robotics market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the industrial robotics market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the industrial robotics market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major developers offering various industrial robotics will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of industrial robotics market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the industrial robotics industry.