Wissen Research analyzed that the global blood glucose monitoring devices market was valued at USD 16.5 billion in 2024 and is projected to reach USD 25.4 billion by 2030, expected to grow at a CAGR of 7.5% during the forecast period, 2025-2030.

Global blood glucose monitoring market is anticipated to reach USD 25.4 billion by 2030 from USD 16.5 billion in 2024, growing at an annualized rate of 7.5% during the forecast period, 2025-2030 | Europe’s blood glucose monitoring market is experiencing steady growth, driven by the increasing prevalence of diabetes and a growing geriatric population requiring continuous monitoring. The region also benefits from strong healthcare infrastructure and significant investments in diabetes care technologies, particularly in countries like Germany, France, and the UK, alongside comprehensive reimbursement policies supporting advanced monitoring systems. | Asia-Pacific The Asia-Pacific blood glucose monitoring market is expanding rapidly, fueled by a diabetes epidemic driven by rising obesity, sedentary lifestyles, and genetic predisposition, coupled with improving healthcare access, rising disposable incomes, and growing awareness about diabetes management. |

The blood glucose monitoring market is experiencing significant transformation, propelled by a growing demand for accurate, convenient, and connected monitoring solutions essential for effective diabetes management across diverse patient profiles, including those with Type 1, Type 2, and gestational diabetes. | Global Investment in the blood glucose monitoring sector are heavily focused on enhancing sensor accuracy and longevity, developing less invasive and fully non-invasive measurement techniques, integrating advanced software for data analytics, predictive alerts, and integration with insulin delivery systems (creating hybrid and fully closed-loop systems), and advancing connectivity features for remote patient monitoring and telehealth integration. |

Drivers: Rising Prevalence of Diabetes Globally

The primary driver for the blood glucose monitoring system market is the rapidly increasing prevalence of diabetes worldwide. According to the International Diabetes Federation and recent market analyses, over 537 million adults had diabetes in 2021, and this number is projected to rise significantly in the coming decades. The growing patient population necessitates regular blood glucose monitoring to manage diabetes effectively. As the number of diagnosed diabetes cases grows, there is a higher demand for both traditional self-monitoring devices and advanced continuous glucose monitoring (CGM) systems that provide real-time data for better disease management. This surge in diabetes cases has propelled manufacturers to innovate and improve device accuracy, convenience, and integration with smartphones and healthcare systems.

Opportunities: Technological Advancements in Continuous Glucose Monitoring

Technological innovation represents a significant market opportunity, particularly in continuous glucose monitoring (CGM) systems. CGMs offer real-time, continuous tracking of glucose levels without frequent finger pricks, providing comprehensive data to users and healthcare providers. Advancements include improved sensor accuracy, longer sensor life, smaller and more comfortable devices, and integration with smartphones and digital health platforms. These improvements promote better patient adherence and proactive disease management, which can reduce severe complications from diabetes. The integration of CGMs with telemedicine and electronic health records enhances data-driven personalized care. Given ongoing research and development efforts by key players such as Abbott and Medtronic, there is strong potential to capture a larger market share in both developed and emerging regions.

Challenges: High Cost and Accessibility Barriers

One of the major challenges hindering market growth is the high cost associated with advanced blood glucose monitoring systems, especially continuous glucose monitors. The sophisticated technology, sensor replacement requirements, and limited insurance coverage in many regions make these devices less accessible to a broad range of patients, particularly in developing countries. The cost barrier restricts adoption despite the clinical benefits. Additionally, users face discomfort due to sensor insertions and replacement frequency, which impacts compliance. There is also a challenge related to the overwhelming amount of data generated by CGMs, which requires patient education and healthcare provider support for effective use. Regulatory complexities and reimbursement issues further restrict market penetration. Addressing these cost and usability challenges is critical for expanding accessibility and maximizing the impact of glucose monitoring technologies on diabetes management.

The blood glucose monitoring system market is one of the cornerstones of diabetes care and management; it plays an important role in providing both the patient and healthcare provider with key information required for effective glycemic control. The blood glucose monitoring system market was estimated to be valued at USD 16.5 billion in 2024 is expected high growth for both the industry, as well as the market as whole, as it is projected to grow at a CAGR of around 7.5% over the projected period, and exceed USD 25.4 billion by 2030. This growth cannot be understated, and is mainly driven by increasing global prevalence of diabetes mellitus (both Type 1 and Type 2, which is epidemic), and the need for regular and constant blood glucose monitoring. Other key market drivers include both the geriatric population who statistically have an increased predisposition for diabetes, increasing healthcare expenditure and disposable income in developing countries which lead to greater accessibility to monitoring technology.

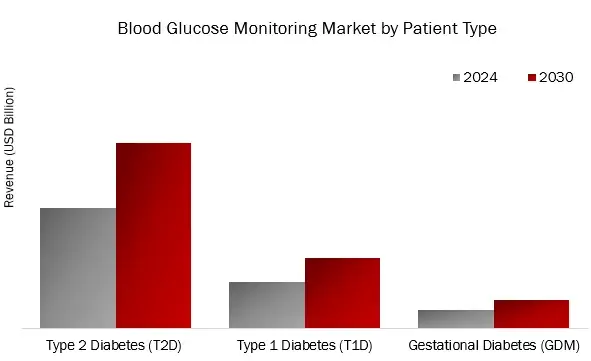

Type 2 Diabetes held the largest market share in the blood glucose monitoring market by patient type in 2024.

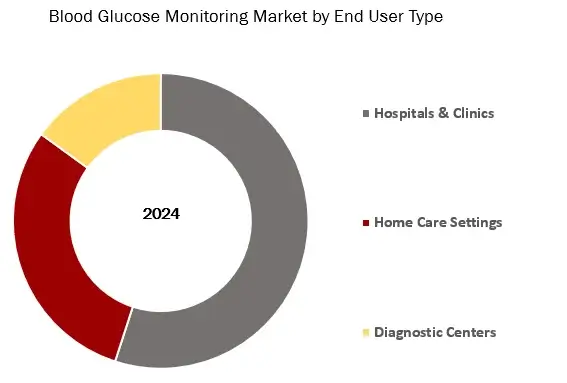

Hospitals & Clinics held the largest share in the blood glucose monitoring market by end user in 2024.

Asia Pacific will show the highest growth rate in blood glucose monitoring market forecast period. (2025-2030)

The Asia Pacific region demonstrates strong real-world indicators validating its high growth potential in the blood glucose monitoring system market between 2025 and 2030. As of 2023, more than 300 million people in this region were living with diabetes, with countries like China, India, and Malaysia reporting some of the highest prevalence rates globally. For instance, India alone has seen its diabetic population triple over the past two decades to 74 million cases in 2023. This growing number of diabetes patients has created a significant demand for effective diabetes management tools, including blood glucose monitoring systems. In terms of usage, self-monitoring blood glucose (SMBG) devices dominate the market in Asia Pacific due to their affordability and ease of use compared to continuous glucose monitoring (CGM) devices, which see lower adoption primarily because of cost barriers in many countries of this region. Despite lower penetration of advanced CGM technology, the region actively invests in expanding access to blood glucose monitoring through government initiatives and non-profit programs distributing glucometers and test strips along with insulin. Additionally, digital diabetes management solutions, including remote blood glucose monitoring and AI-powered apps, are rapidly gaining traction, driven by increasing smartphone penetration and telehealth initiatives across the region. Countries like India and Australia have introduced national digital health policies facilitating integration of glucose monitoring data into healthcare ecosystems, enabling more personalized and real-time diabetes care.

Major players operating in blood glucose monitoring (bgm) market are:

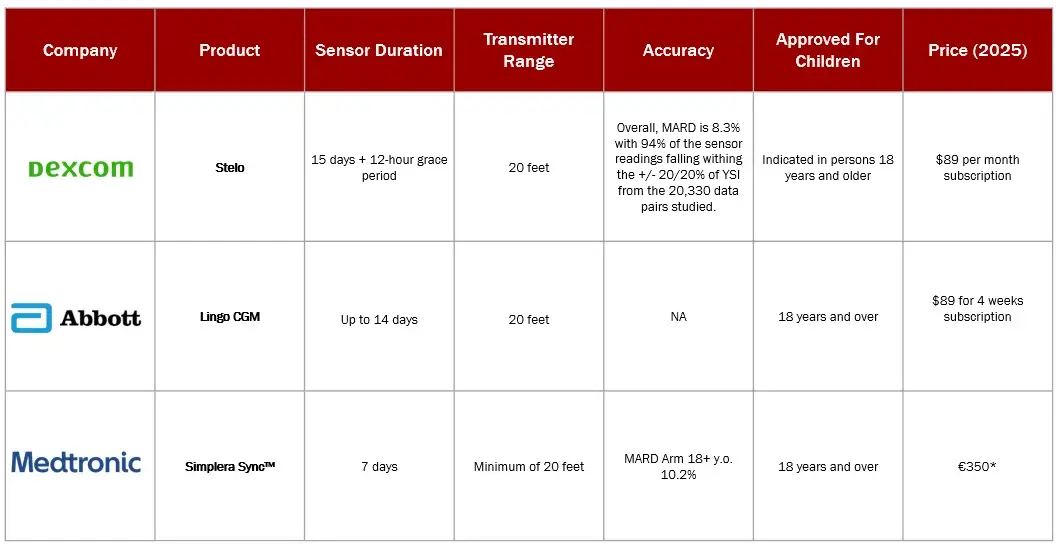

Note: The price given above is from the company’s websites or third-party websites.

*Currently, Simplera Sync™ is only available in Europe, and is expected to be released in the US in the fall of 2025.

Sources: Secondary Research

“The integration of continuous glucose monitoring (CGM) sensor data with dedicated mobile applications and cloud platforms is facilitating automated trend analysis, real-time alerts for hypo/hyperglycaemia, and long-term pattern identification, augmenting clinician oversight and potentially improving diabetes management efficacy and patient engagement.”

Endocrinologist – Academic Medical Center (North America)

“The miniaturization of non-invasive glucose monitoring technologies and the development of less invasive wearable sensors are facilitating more comfortable and convenient self-monitoring for patients, potentially increasing adherence to monitoring protocols and improving long-term glycaemic control outcomes.”

Senior Product Manager, Diabetes Care Division – Medical Device Manufacturer (Europe)

“The integration of blood glucose data with electronic health records (EHRs) and telehealth platforms is facilitating seamless data sharing between patients and healthcare providers, enabling remote monitoring and timely intervention, potentially improving clinical decision-making and reducing emergency room visits related to acute glycaemic events.”

Chief Medical Information Officer – Integrated Healthcare System (Asia-Pacific)

“The increasing utilization of artificial intelligence (AI) algorithms to analyze complex glucose data patterns from CGM devices is facilitating personalized insulin dosing recommendations and predictive insights for upcoming glucose fluctuations, augmenting clinician guidance and potentially improving treatment personalization and overall diabetes management success.”

Director of Digital Health – Independent Diabetes Technology Consultant (Global)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. BLOOD GLUCOSE MONITORING MARKET: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. REGULATORY SCENARIO & TRENDS

4.5. NEED GAP ANALYSIS

4.6. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.7. CASE STUDY ANALYSIS

4.8. TECHNOLOGY ANALYSIS

4.9. TRADE ANALYSIS

4.10. INDUSTRY TRENDS

4.11. PRICING ANALYSIS

4.12. REIMBURSEMENT SCENARIO

4.13. USE OF AI IN BLOOD GLUCOSE MONITORING DEVICE

4.14. PORTER’S FIVE FORCES ANALYSIS

4.15. IMPACT OF US TARIFF [2025]

4.16. REGULATORY LANDSCAPE

4.16.1. NORTH AMERICA

4.16.2. EUROPE

4.16.3. ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

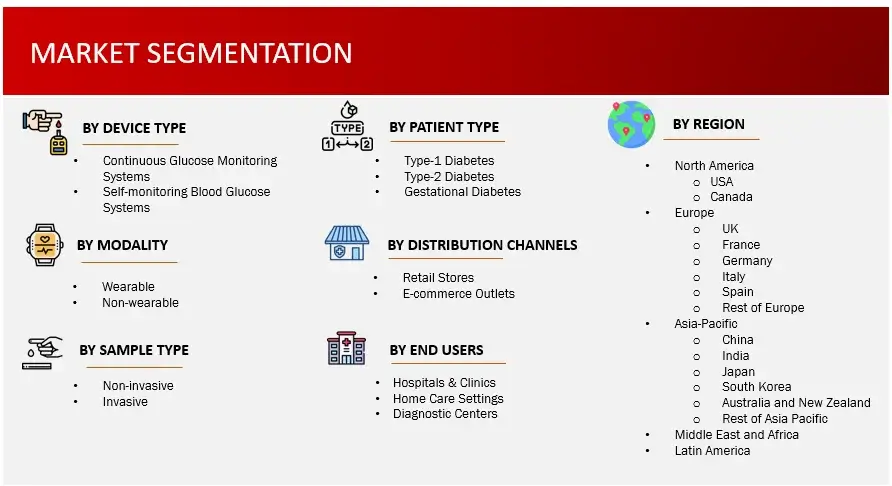

6. GLOBAL BLOOD GLUCOSE MONITORING MARKET, BY DEVICE TYPE (2024-2030, USD MILLION)

6.1. CONTINUOUS GLUCOSE MONITORING (CGM) SYSTEMS

6.1.1.SENSORS

6.1.2.TRANSMITTERS & RECEIVERS

6.1.3.INSULIN PUMPS

6.2. SELF-MONITORING BLOOD GLUCOSE (SMBG) SYSTEMS

6.2.1.BLOOD GLUCOSE METERS

6.2.2.TEST STRIPS

6.2.3.LANCETS

7. GLOBAL BLOOD GLUCOSE MONITORING MARKET, BY MODALITY (2024-2030, USD MILLION)

7.1. WEARABLE

7.2. NON-WEARABLE

8. GLOBAL BLOOD GLUCOSE MONITORING MARKET, BY PATIENT TYPE (2024-2030, USD MILLION)

8.1. TYPE-1 DIABETES

8.1.1.ADULTS

8.1.2.PEDIATRICS

8.2. TYPE-2 DIABETES

8.2.1.ADULTS

8.2.2.PEDIATRICS

8.3. GESTATIONAL DIABETES

9. GLOBAL BLOOD GLUCOSE MONITORING MARKET, BY DISTRIBUTION CHANNEL TYPE (2024-2030, USD MILLION)

9.1. RETAIL STORES

9.2. E-COMMERCE OUTLETS

10. GLOBAL BLOOD GLUCOSE MONITORING MARKET, BY SAMPLE TYPE (2024-2030, USD MILLION)

10.1. NON-INVASIVE

10.2. INVASIVE

11. GLOBAL GLUCOSE MONITORING SYSTEMS MARKET, BY END USERS (2024-2030, USD MILLION)

11.1. HOSPITALS & CLINICS

11.2. HOME CARE SETTINGS

11.3. DIAGNOSTIC CENTERS

12. GLOBAL BLOOD GLUCOSE MONITORING MARKET, BY REGION (2024-2030, USD MILLION)

12.1. NORTH AMERICA

12.1.1. US

12.1.2. CANADA

12.2. EUROPE

12.2.1. GERMANY

12.2.2. FRANCE

12.2.3. SPAIN

12.2.4. ITALY

12.2.5. UK

12.2.6. REST OF THE EUROPE

12.3. ASIA-PACIFIC

12.3.1. CHINA

12.3.2. JAPAN

12.3.3. INDIA

12.3.4. AUSTRALIA AND NEW ZEALAND

12.3.5. SOUTH KOREA

12.3.6. REST OF THE ASIA-PACIFIC

12.4. MIDDLE EAST AND AFRICA

12.5. LATIN AMERICA

13. COMPETITIVE ANALYSIS

13.1. PRODUCT PIPELINE: BLOOD GLUCOSE MONITORING DEVICES

13.2. KEY PLAYERS FOOTPRINT ANALYSIS

13.3. MARKET SHARE ANALYSIS (2023/2024)

13.4. REGIONAL SNAPSHOT OF KEY PLAYERS

13.5. R&D EXPENDITURE OF KEY PLAYERS

14. COMPANY PROFILES

14.1. ABBOTT LABORATORIES (US)

14.1.1. BUSINESS OVERVIEW

14.1.2. PRODUCT PORTFOLIO

14.1.3. FINANCIAL SNAPSHOT

14.1.4. RECENT DEVELOPMENTS

14.1.4.1. MERGER/ACQUISITIONS

14.1.4.2. PRODUCT APPROVAL/LAUNCHES

14.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

14.3. DEXCOM, INC. (US)

14.4. NOVO NORDISK A/S (DENMARK)

14.5. F. HOFFMANN-LA ROCHE LTD (SWITZERLAND)

14.6. ASCENSIA DIABETES CARE HOLDINGS AG (SWITZERLAND)

14.7. JOHNSON & JOHNSON (US)

14.8. GLYSENS INCORPORATED (US)

14.9. NOVA BIOMEDICAL CORPORATION (US)

14.10. TERUMO CORPORATION (JAPAN)

14.11. SANOFI A.S. (FRANCE)

14.12. LIFESCAN IP HOLDINGS, LLC (US),

14.13. OTHER PLAYERS

14.13.1. B. BRAUN SE (GERMANY)

14.13.2. MENARINI DIAGNOSTICS S.R.L. (ITALY)

14.13.3. SENSEONICS, INC. (US)

14.13.4. YPSOMED AG (SWITZERLAND)

14.13.5. NIPRO CORPORATION (JAPAN)

14.13.6. ARKRAY INC. (JAPAN)

14.13.7. PRODIGY DIABETES CARE (US)

14.13.8. ACON LABORATORIES (US)

15. APPENDIX

15.1. INDUSTRY SPEAK

15.2. QUESTIONNAIRE/DISCUSSION GUIDE

15.3. AVAILABLE CUSTOM WORK

15.4. ADJACENT STUDIES

15.5. AUTHORS.

16. REFERENCES

Glucose monitoring devices market is a range of products and technologies used for the quantification and analysis of blood glucose to treat diabetes and other metabolic diseases. Glucose monitoring is used to diagnose and monitor glycemic control in diabetes, prevent hypoglycemia and hyperglycemia incidents, and inform treatment decisions, offering benefits such as real-time results, continuous monitoring, and actionable information for individualized care. The market caters to various segments such as healthcare providers, home care environments, clinical laboratories, and fitness and wellness businesses, including such parts as glucose meters, continuous glucose monitoring (CGM) systems, test strips, sensors, and insulin delivery integration. Minimally invasive sensors, wireless connectivity, and AI-based predictive analysis are some of the prime market features. The market is fueled by growing global prevalence of diabetes, rising demand for non-invasive monitoring, and advancements in sensor precision and data integration technology. New trends such as implantable glucose sensors, smartphone-connected platforms, and closed-loop insulin delivery systems are driving innovation and adoption across the world.

FIGURE: BLOOD GLUCOSE MONITORING MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the blood glucose monitoring market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the blood glucose monitoring market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the blood glucose monitoring market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major developers offering various blood glucose monitoring will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of blood glucose monitoring market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size using the market size estimation processes the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the blood glucose monitoring industry.