Wissen Research analyzed that the global HIV diagnostics market was valued at USD 2.4 billion in 2024 and is projected to reach USD 3.4 billion by 2030, expected to grow at a CAGR of 6.2 % during the forecast period, 2025-2030.

HIV Diagnostics Market: Lucrative Opportunities

Global HIV diagnostics market is anticipated to reach USD 3.4 billion by 2030 from USD 2.4 billion in 2024, growing at an annualized rate of 6.2% during the forecast period, 2025-2030 | North America maintains a dominant position in the HIV diagnostics market in terms of value, driven by high healthcare expenditure, advanced laboratory infrastructure supporting sophisticated testing (NATs, genotyping), significant R&D investment by key players, stringent regulatory standards ensuring test quality, and a substantial disease burden requiring continuous monitoring. | Asia-Pacific The HIV diagnostics market in the Asia-Pacific region is experiencing significant growth, driven by the large and diverse HIV burden across the region, substantial investments by governments and international organizations in HIV testing and treatment programs, expanding access to diagnostic services in both urban and rural areas, increasing healthcare infrastructure development, and growing public health initiatives aimed at controlling the epidemic. |

Advances in HIV diagnostics, such as highly sensitive nucleic acid tests (NATs) for early detection and viral load monitoring, sophisticated fourth-generation immunoassays reducing the window period, and the development of rapid point-of-care (POC) and self-testing technologies, are enabling faster, more accessible, and accurate diagnosis and management of HIV infection globally. | Global investment and research in HIV diagnostics are heavily focused on enhancing the accessibility and speed of testing through improved POC devices and self-tests, reducing the cost of NATs and viral load monitoring, developing assays for better differentiation of HIV types/strains, improving early infant diagnosis methods, and integrating diagnostics with treatment and prevention programs to combat the ongoing pandemic effectively. |

Strategic Activities Within the HIV Diagnostics Market

Drivers: Escalating Global HIV Prevalence and Need for Lifelong Monitoring.

The substantial and significant global burden of HIV/AIDS fundamentally fuels the entire HIV diagnostics market. The extensive population of people living with HIV necessitates continuous monitoring through regular Viral Load and CD4+ T-cell tests to effectively manage treatment and prevent drug resistance, creating a constant high demand for these services. Additionally, the continuous need for screening programs to detect new infections and track the epidemic drives demand for initial diagnostic tests like antibody/antigen assays. This multi-factional demand solidifies the market’s significant size and growth potential.

For instance, with an estimated 40.8 million people living with HIV worldwide in 2024 and 1.3 million new infections that year, according to WHO and UNAIDS. This large population necessitates lifelong monitoring through regular viral load (VL) and CD4+ T-cell count testing to guide treatment, assess immune status, and prevent drug resistance, as recommended by international guidelines. Despite progress, significant gaps remain—in 2024, 87% of people with HIV knew their status, 77% were on treatment, and just 73% achieved viral suppression—underscoring the ongoing need for robust diagnostic services.

Opportunities: Expansion of Point-of-Care (POC) and Self-HIV Testing.

This presents a major opportunity for new entrants to potentially bypass some of the entrenched competition in the laboratory-based diagnostics space. The shift towards POC and self-testing addresses unmet needs related to speed, access, privacy, and scalability, especially in remote or resource-limited areas where laboratory infrastructure is weak. New players can focus R&D and marketing efforts on innovative, user-friendly, potentially lower-cost POC devices or self-test formats. Success in this segment can allow entrants to capture market share directly at the patient or community level, building brand recognition and establishing a foothold without necessarily competing head-on with giants in the complex lab instrument market initially. Regulatory pathways for self-tests, while stringent, are becoming clearer, presenting a defined path to market.

Challenges: Significant Capital and Infrastructure Barriers for Advanced Diagnostics

A major challenge facing the HIV diagnostics market, particularly concerning advanced testing like Nucleic Acid Tests (NATs) for viral load and early infant diagnosis, is the substantial cost and infrastructure required. The high price of sophisticated NAT instruments, the ongoing expense of specialized reagents, and the need for robust laboratory infrastructure (including temperature control, power supply, and trained technical staff) create barriers. These challenges are particularly acute in low- and middle-income countries (LMICs) where the HIV burden is highest but resources are often limited. Overcoming these barriers is crucial for ensuring widespread access to the most critical monitoring tools, as the financial and logistical demands can restrict the scale and scope of advanced diagnostic implementation, impacting effective patient management and public health surveillance.

The global HIV diagnostics market, a critical component of public health and clinical care focused on the detection, monitoring, and management of HIV infection, represents a significant and evolving segment within the broader in vitro diagnostics industry. This market is driven by its essential role in disease control, patient treatment, blood safety, and prevention efforts. Valued at approximately USD 2.4 billion in 2024, the HIV diagnostics market is projected to reach around USD 3.4 billion by 2030, reflecting a Compound Annual Growth Rate (CAGR) of approximately 6.2% during the forecast period. This expansion is supported by continuous technological advancements and sustained global efforts against the epidemic. Innovations include highly sensitive Nucleic Acid Tests (NATs) for early diagnosis and viral load monitoring, sophisticated fourth-generation immunoassays reducing the diagnostic window, and the significant development and adoption of Point-of-Care Testing (POC) devices and self-testing kits for greater accessibility and speed. The market also encompasses sophisticated software for laboratory information management, data tracking, and patient monitoring, which is crucial for effective HIV care programs. The essential nature of key consumables, such as test kits (RDTs, NAT reagents), controls, and collection materials, ensures a continuous demand alongside the instruments. These advancements, coupled with expanding applications in comprehensive patient management, early infant diagnosis, treatment monitoring, and global health initiatives aimed at achieving epidemic control, are broadening the scope, efficiency, and accessibility of HIV diagnostics worldwide.

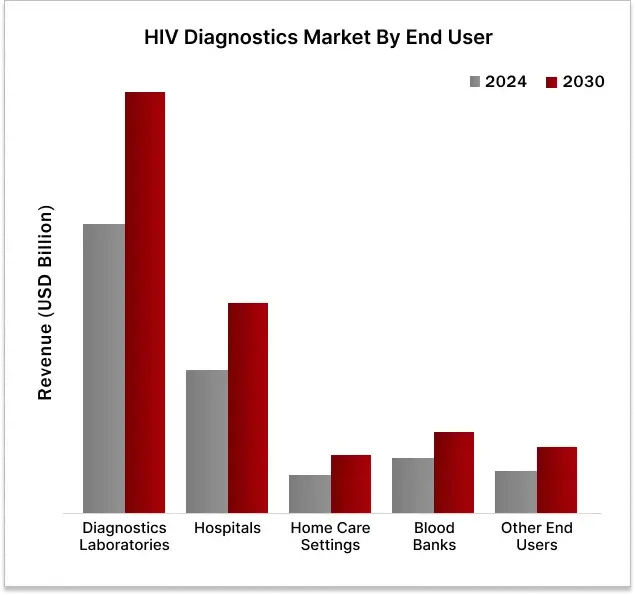

Diagnostics Laboratories dominated the HIV Diagnostics Market by End User in 2024

collection centers, which require mandatory HIV screening for blood safety, often rely heavily on laboratory-based assays capable of high-volume processing. While hospitals perform significant testing, much of it might be sent to central lab facilities. POC testing and home testing represent growing niches but currently serve a smaller volume compared to the comprehensive testing performed in dedicated diagnostic laboratories, which process millions of HIV tests annually globally.

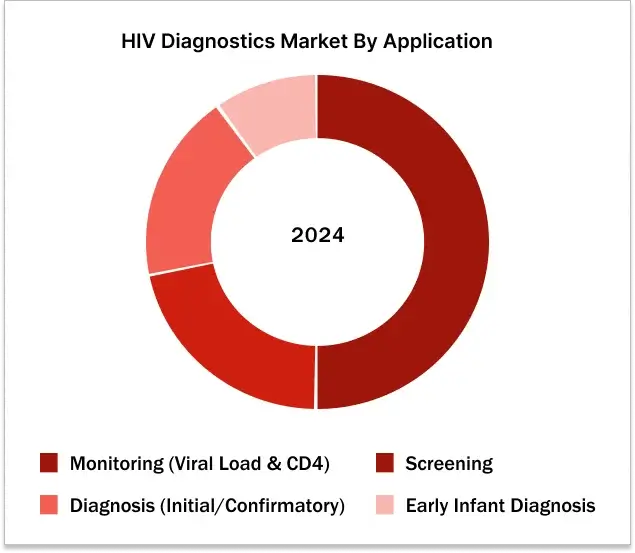

Monitoring tests dominated the HIV diagnostics market by application in 2024.

of PLHIV needing regular follow-up. The increasing focus on achieving and maintaining viral suppression as a key public health goal also underscores the importance of high monitoring capabilities. Consequently, despite the importance of screening and early infant diagnosis, the aggregate volume and frequency of VL tests performed for monitoring purposes solidify its position as the largest application segment in the HIV diagnostics market in 2024.

Asia Pacific poised for the highest growth rate in the HIV diagnostics market (2025-2030)

The HIV diagnostics market is projected to show highest growth, particularly in the Asia-Pacific region, during the forecast period (2025-2030), driven by a powerful confluence of economic, and healthcare-related factors. Key drivers fuelling this expansion include the substantial and, in some areas, increasing burden of HIV/AIDS across the diverse countries within Asia Pacific. This high disease prevalence creates a continuous and growing demand for diagnostic testing, from initial screening to vital viral load and CD4 monitoring for patients on Antiretroviral Therapy (ART). Concurrently, there is a marked increase in disposable incomes and rising healthcare expenditure in major economies like China and India, enabling greater public and private investment in healthcare infrastructure, including laboratories and clinics capable of performing advanced HIV diagnostics, particularly nucleic acid tests (NATs) and viral load monitoring.

Furthermore, strong commitment and funding from national governments and international organizations (like PEPFAR, Global Fund) are critical, supporting expanded access to testing services, procurement of diagnostic kits, and strengthening of healthcare systems. The region is also witnessing a heightened focus on achieving UNAIDS targets, which necessitates widespread testing and effective monitoring to ensure treatment success and prevent transmission. Rising regulatory standards aimed at ensuring blood safety and quality control in diagnostics further mandate the adoption and expansion of HIV testing capabilities. Additionally, increasing awareness campaigns and reduced stigma, albeit varying by country, are encouraging more individuals to get tested. The establishment of regional operations by global diagnostics companies and ongoing efforts to improve access to affordable, high-quality diagnostics, including point-of-care and self-testing options suitable for diverse healthcare settings, further stimulate market growth and innovation in the Asia Pacific HIV diagnostics sector.

INDUSTRY SPEAK: KEY INSIGHTS FROM PRIMARY INTERVIEWS

“Rapid, antibody-based HIV tests are becoming increasingly integrated into community health programs and outreach initiatives in high-burden regions, significantly lowering the barrier to initial diagnosis and facilitating linkage to care.”

Head of Global Health Initiatives – Non-Profit Diagnostics Organization (North America)

“The adoption of dried blood spot (DBS) samples for HIV viral load testing is expanding access in remote and resource-limited areas, overcoming logistical challenges associated with sample transport and storage.”

Chief Medical Informatics Officer – Large Academic Medical Center (Europe)

“Next-Generation Sequencing (NGS) technologies are gaining traction in specialized HIV diagnostic labs for detecting drug resistance mutations, informing personalized antiretroviral therapy selection for complex cases.”

Vice President, Molecular Diagnostics – Clinical Laboratory Provider (Asia-Pacific)

“The increasing availability and use of integrated platforms capable of simultaneously screening for HIV and other key STIs (like Syphilis and Hepatitis B/C) are improving screening efficiency and comprehensive patient management in high-risk populations.”

Director of Clinical Operations – Public Health Laboratory (Global)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. HIV DIAGNOSTICS MARKET: OVERVIEW

4.1.1. INTRODUCTION

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. REGULATORY SCENARIO & TRENDS

4.5. NEED GAP ANALYSIS

4.6. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.7. REIMBURSEMENT SCENARIO

4.8. TRADE ANALYSIS

4.9. INDUSTRY TRENDS

4.10. TECHNOLOGIES ANALYSIS

4.11. PORTER’S FIVE FORCES ANALYSIS

4.12. REGULATORY LANDSCAPE

4.12.1. NORTH AMERICA

4.12.2. EUROPE

4.12.3. ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. GLOBAL HIV DIAGNOSTICS MARKET, BY PRODUCT (2024-2030, USD MILLION)

6.1. INSTRUMENTS

6.2. REAGENTS & KITS

6.3. SOFTWARE

7. GLOBAL HIV DIAGNOSTICS MARKET, BY TESTS TYPE (2024-2030, USD MILLION)

7.1. ANTIBODY TESTS

7.2. ANTIGENS TESTS

7.2.1.P24 ANTIGEN ASSAY

7.3. NUCLEIC ACID TESTS (NATS) / MOLECULAR TESTS

7.3.1.HIV RNA DETECTION TESTS

7.3.2.HIV DNA DETECTION TESTS

7.4. COMBINATION TESTS (ANTIGEN-ANTIBODY)

8. GLOBAL HIV DIAGNOSTICS MARKET, BY TESTING MODE (2024-2030, USD MILLION)

8.1. LABORATORY-BASED DIAGNOSTICS

8.2. SELF-TESTING KITS

9. GLOBAL HIV DIAGNOSTICS MARKET, BY APPLICATION (2024-2030, USD MILLION)

9.1. SCREENING

9.2. DIAGNOSIS

9.3. MONITORING

9.4. EARLY INFANT DIAGNOSIS

10. GLOBAL HIV DIAGNOSTICS MARKET, BY END USERS (2024-2030, USD MILLION)

10.1. HOSPITALS

10.2. DIAGNOSTICS LABORATORIES

10.3. BLOOD BANKS

10.4. HOME CARE SETTINGS

10.5. OTHER END USERS

11. GLOBAL HIV DIAGNOSTICS MARKET, BY REGION (2024-2030, USD MILLION)

11.1. NORTH AMERICA

11.1.1. US

11.1.2. CANADA

11.2. EUROPE

11.2.1. GERMANY

11.2.2. FRANCE

11.2.3. SPAIN

11.2.4. ITALY

11.2.5. UK

11.2.6. REST OF THE EUROPE

11.3. ASIA-PACIFIC

11.3.1. CHINA

11.3.2. JAPAN

11.3.3. INDIA

11.3.4. AUSTRALIA AND NEW ZEALAND

11.3.5. SOUTH KOREA

11.3.6. REST OF THE ASIA-PACIFIC

11.4. MIDDLE EAST AND AFRICA

11.5. LATIN AMERICA

12. COMPETITIVE ANALYSIS

12.1. PRODUCT PIPELINE: HIV DIAGNOSTICS

12.2. KEY PLAYERS FOOTPRINT ANALYSIS

12.3. MARKET SHARE ANALYSIS (2023/2024)

12.4. REGIONAL SNAPSHOT OF KEY PLAYERS

12.5. R&D EXPENDITURE OF KEY PLAYERS

13. COMPANY PROFILES

13.1. F. HOFFMANN-LA ROCHE LTD. (SWITZERLAND)

13.1.1. BUSINESS OVERVIEW

13.1.2. PRODUCT PORTFOLIO

13.1.3. FINANCIAL SNAPSHOT

13.1.4. RECENT DEVELOPMENTS

13.1.4.1. MERGER/ACQUISITIONS

13.1.4.2. PRODUCT APPROVAL/LAUNCHES

13.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

13.2. SIEMENS HEALTHINEERS (GERMANY)

13.3. DANAHER CORPORATION (US)

13.4. ABBOTT LABORATORIES (US)

13.5. GRIFOLS, S.A.(SPAIN)

13.6. BIO-RAD LABORATORIES INC. (US)

13.7. HOLOGIC, INC. (US)

13.8. OTHER PLAYERS

13.8.1. BIOMÉRIEUX (FRANCE)

13.8.2. QIAGEN (GERMANY)

13.8.3. BD (US)

13.8.4. TRINITY BIOTECH (IRELAND)

13.8.5. ORASURE TECHNOLOGIES, INC. (US)

13.8.6. BIOSYNEX SA (FRANCE)

13.8.7. WONDFO (CHINA)

13.8.8. GETEIN BIOTECH, INC. (CHINA)

13.8.9. MERIL LIFE SCIENCES PVT. LTD. (INDIA)

13.8.10. ACCUBIOTECH CO., LTD. (CHINA)

13.8.11. BIOLYTICAL LABORATORIES INC. (CANADA)

13.8.12. BIO LAB DIAGNOSTICS (I) PRIVATE LIMITED (INDIA)

13.8.13. ALPINE BIOMEDICALS PVT LTD. (INDIA)

13.8.14. MOLBIO DIAGNOSTICS PVT. LTD. (INDIA)

13.8.15. FORTRESS DIAGNOSTICS (UK)

13.8.16. ADVACARE PHARMA (ACCQUICK) (US)

13.8.17. ADALTIS S.R.L. (ITALY)

14. APPENDIX

14.1. INDUSTRY SPEAK

14.2. QUESTIONNAIRE/DISCUSSION GUIDE

14.3. AVAILABLE CUSTOM WORK

14.4. ADJACENT STUDIES

14.5. AUTHORS

15. REFERENCES

Market Definition: HIV/AIDS Diagnostics

The HIV Diagnostics market represents a critical and specialized segment within the clinical diagnostics industry, exclusively focused on detecting, identifying, and monitoring the Human Immunodeficiency Virus (HIV). This market is fundamental to managing the HIV epidemic, enabling timely diagnosis, initiation of antiretroviral therapy (ART), monitoring treatment success, and preventing transmission. It encompasses instruments, reagents, consumables, and software specifically designed for HIV testing.

These diagnostic techniques provide essential information about the presence, stage, and viral activity of HIV infection through methods that typically detect the body’s immune response (HIV antibodies), components of the virus (HIV antigens, like p24), or the virus’s genetic material (HIV RNA or DNA). Key technologies employed include HIV Antibody/Antigen Tests using immunoassay formats for initial screening, Rapid Diagnostic Tests (RDTs) for quick point-of-care results, Nucleic Acid Tests (NATs) using Polymerase Chain Reaction (PCR) to directly detect and quantify viral load for early diagnosis and treatment monitoring, and specific HIV Confirmatory Tests to verify positive results.

Additionally, while a hematology parameter, CD4+ T lymphocyte counting via Flow Cytometry is a cornerstone HIV diagnostic and monitoring tool assessing immune system damage. These systems employ techniques like antigen-antibody binding, genetic material amplification, and cell surface marker identification, combined with specific HIV reagents, to process biological samples (primarily blood) and provide accurate results regarding infection status, viral activity, and immune health, directly supporting patient care and public health strategies for HIV.

FIGURE: HIV/AIDS DIAGNOSTICS MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the HIV diagnostics market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the HIV diagnostics market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research will be conducted after acquiring knowledge about the HIV diagnostics market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major developers offering various HIV diagnostics will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of HIV diagnostics will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the HIV diagnostics industry.