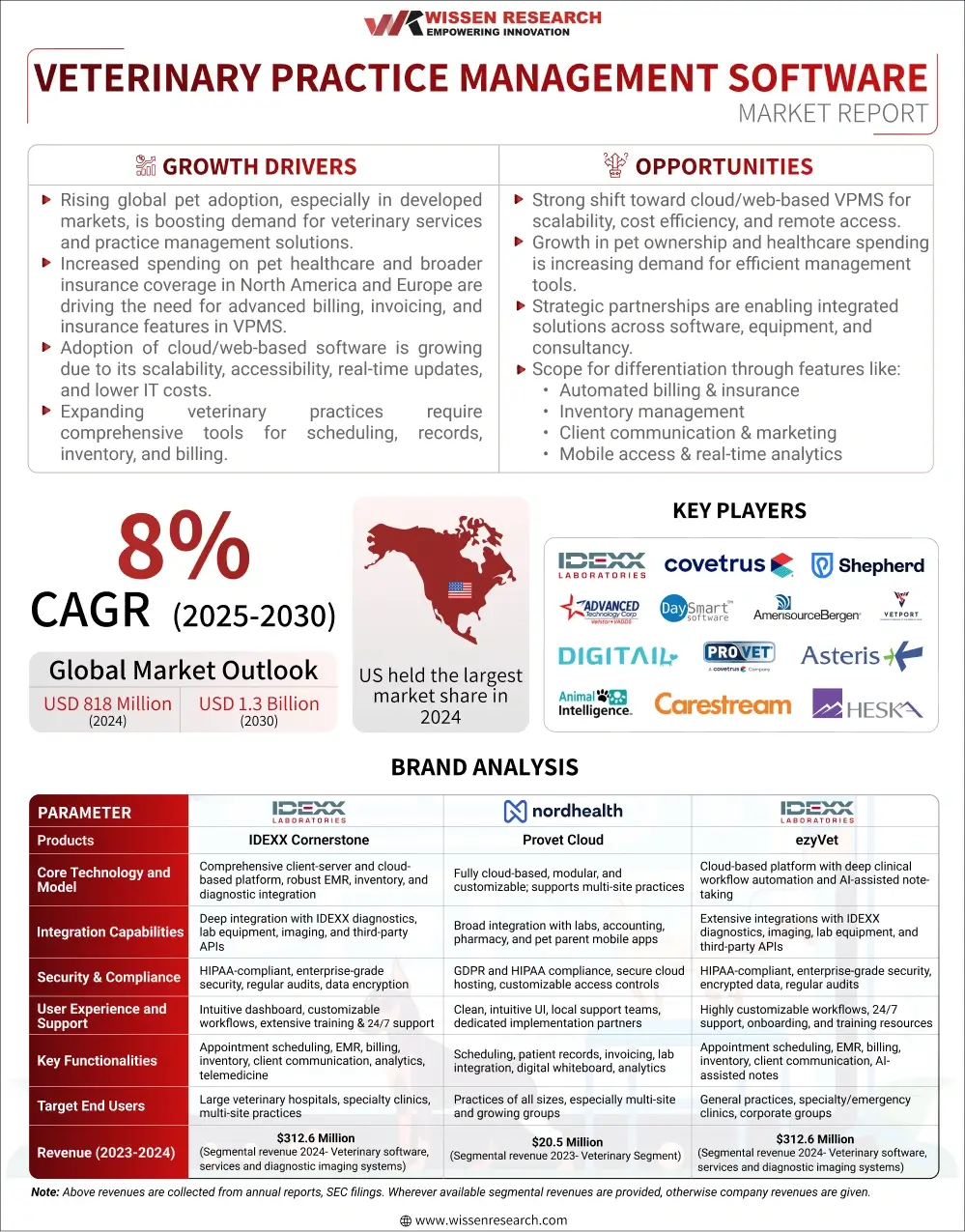

Wissen Research analyzed that the global veterinary practice management software market was valued at USD 818 million in 2024 and is projected to reach USD 1.3 billion by 2030, growing at a CAGR of 8% during the forecast period, 2025-2030.

The key growth drivers of the veterinary practice management software market are increasing pet ownership and corresponding healthcare spending, technological innovations such as cloud-based models and AI integration, increasing demand for niche veterinary services, strategic collaborations between software developers and equipment manufacturers, and increased animal health spending with the growing adoption of pet insurance.

Challenges here include high costs of implementation and maintenance constraining small-practice uptake, data security and privacy issues in managing sensitive patient data, complexity in integrating with current processes and legacy systems, regulatory uncertainties across geographies, and limited infrastructure and awareness in emerging markets

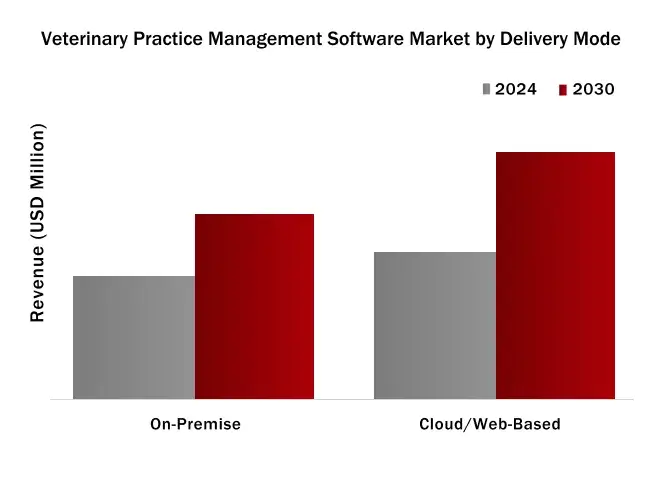

Cloud/web-based segment held the largest share in the market since 2023 and during the forecast period, with North America dominating the regional market share.

Global Veterinary Practice Management Software market is anticipated to reach USD 1.3 billion by 2030 from USD 818 million in 2024, growing at an annualized rate of 8% during the period, 2025-2030 | Asia Pacific is the fastest-growing region, led by China, India, and Australia, where rising pet ownership, expanding veterinary education, and government initiatives are fueling demand for modern, mobile-first software solutions tailored to local needs | Trans-Atlantic North America maintains market leadership, driven by high pet ownership, advanced veterinary services, and regulatory support, while Europe and Canada are seeing growth from integrated cloud solutions and telehealth adoption; emerging markets in Latin America, the Middle East, and Africa are opening new opportunities as digital veterinary care gains traction |

The veterinary practice management software market is being transformed by rapid adoption of AI-powered diagnostics, cloud-based platforms, and integrated telemedicine features, enabling clinics to streamline workflows, enhance patient care, and offer remote consultations | Investment in cloud infrastructure and mobile technologies is accelerating the shift toward scalable, SaaS-based veterinary software, supporting real-time data access, automated client communication, and seamless integration with diagnostic equipment and wearable devices. The industry faces challenges from limited adoption among small practices due to cost and technology hesitancy, as well as regional disparities in digital infrastructure and regulatory frameworks that impact deployment and interoperability |

Drivers: Transforming Veterinary Care Through AI and Cloud Adoption

Spurring adoption of cloud-based and AI-powered veterinary practice management software is revolutionizing clinic operations, facilitating real-time data access, automated processes, and integration with telemedicine and diagnostic equipment. Increased global pet ownership, elevated animal health spending, and demand for more efficient, individualized veterinary care are driving market expansion.

Opportunities: Expanding Horizons in Emerging Veterinary Markets

Accelerated digitalization across emerging economies particularly Asia Pacific, driven by China, India, and Australia is opening new growth paths. Growing veterinary infrastructure, government initiatives for animal healthcare, and demand for mobile-first, locally customized solutions are providing major opportunities for software vendors to tap untapped markets and broaden offerings.

Challenges: Cost, Compliance, and Integration Barriers in Adoption

Significant implementation and maintenance expenses, especially for small and standalone clinics, continue to be a stumbling block to adoption. Concerns about data privacy, complexity of integrating with existing systems, and variations in regional regulatory structures further make deployment challenging and restrict market entry in specific geographies.

The global veterinary practice management software market, encompassing on-premise and cloud-based solutions for veterinary clinics, animal hospitals, and specialty care providers, is undergoing robust expansion fueled by rising pet ownership, digital transformation in animal healthcare, and growing demand for efficient, integrated practice operations. Valued at USD 818 million in 2024, the market is projected to reach USD 1.3 billion by 2030, growing at a CAGR of 8%. Key growth drivers include increased animal health expenditure, the adoption of telemedicine and cloud-based platforms, and the need for comprehensive software to streamline patient records, billing, scheduling, and client engagement. North America leads in adoption, while Asia Pacific is emerging as the fastest-growing region due to rapid digitalization and expanding veterinary infrastructure.

Cloud/Web-based segment dominated the Veterinary Practice Management Software Market by Delivery Mode in 2024

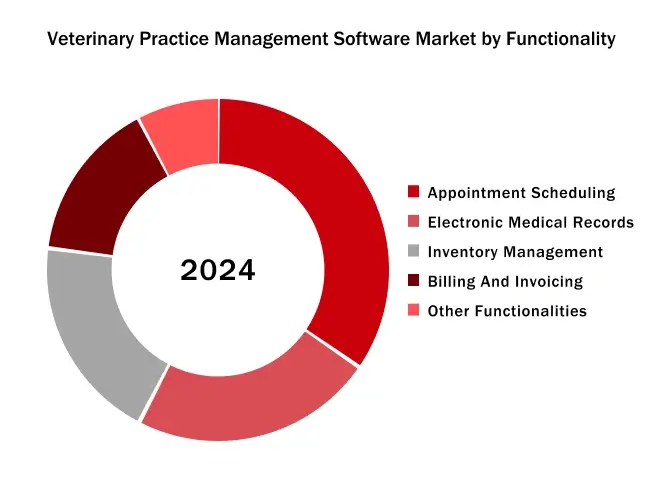

Appointment Scheduling Segment held the largest market share in 2024, accounting for a significant market share in Veterinary Practice Management Software market by Functionality

North America held the largest market share in Veterinary Practice Management Software Market in the forecast period (2025-2030)

North America accounted for the greatest share in the veterinary practice management software market during the forecast period due to a number of important factors. The region is advantaged by high rates of pet ownership, superior veterinary healthcare infrastructure, and strong preventive animal care focus. For instance, large veterinary networks such as Banfield Pet Hospital and VCA Animal Hospitals within the U.S. leverage advanced software platforms to maintain patient files, automate appointment scheduling, and support telemedicine, allowing for productive operations in hundreds of locations. Moreover, the availability of prominent software companies such as IDEXX Laboratories and Covetrus, coupled with widespread usage of cloud-based and telemedicine solutions, further consolidates North America’s position as a leading player in this market.

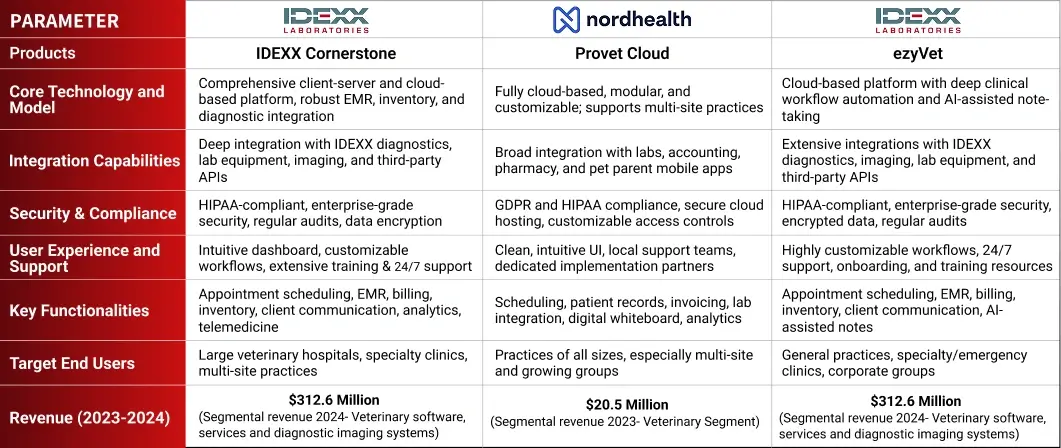

Major players operating in Veterinary Practice Management Software market are:

Note: Above revenues are collected from annual reports, SEC filings. Wherever available segmental revenues are provided, otherwise company revenues are given.

Sources: Secondary Research

PRIMARY INSIGHTS FROM KEY OPINION LEADERS

“Cloud-based and AI-powered solutions are rapidly replacing legacy on premise systems, enabling clinics to automate workflows, integrate telemedicine, and deliver data-driven care”

Chief Technology Officer – Leading Veterinary Software Firm (Europe)

“Rising pet ownership and increased animal health spending are driving demand for comprehensive, integrated software that streamlines scheduling, EMR, billing, and client communications.”

Director, Veterinary Practice Operations – Major Animal Health Group (Asia-Pacific)

“Interoperability and real-time analytics have become critical, with clinics seeking platforms that connect seamlessly to lab systems, imaging, and wearable devices for improved diagnostics and operational insights.”

VP, Product Development – Veterinary IT Solutions Provider (North American)

“Strategic investments and partnerships—such as cloud launches and telehealth integrations—are accelerating market growth, as providers recognize that robust practice management software is now essential for competitiveness and regulatory compliance”

Head of Strategy – Global Animal Health Innovator (Asia Pacific)

Sources: Primary Research and Wissen Research Analysis.

Note: Above mention is non-exhaustive samples of the primary insights.

Particulars | Details |

Report | Veterinary Practice Management Software Market |

Forecast Period | 2025-2030 |

Base Year | 2024 |

Format | |

Market Size (2024) | USD 818 Million |

CAGR (2025-2030) | 8% |

Number of Pages | 165 |

Number of Tables | 155 |

Number of Figures | 34 |

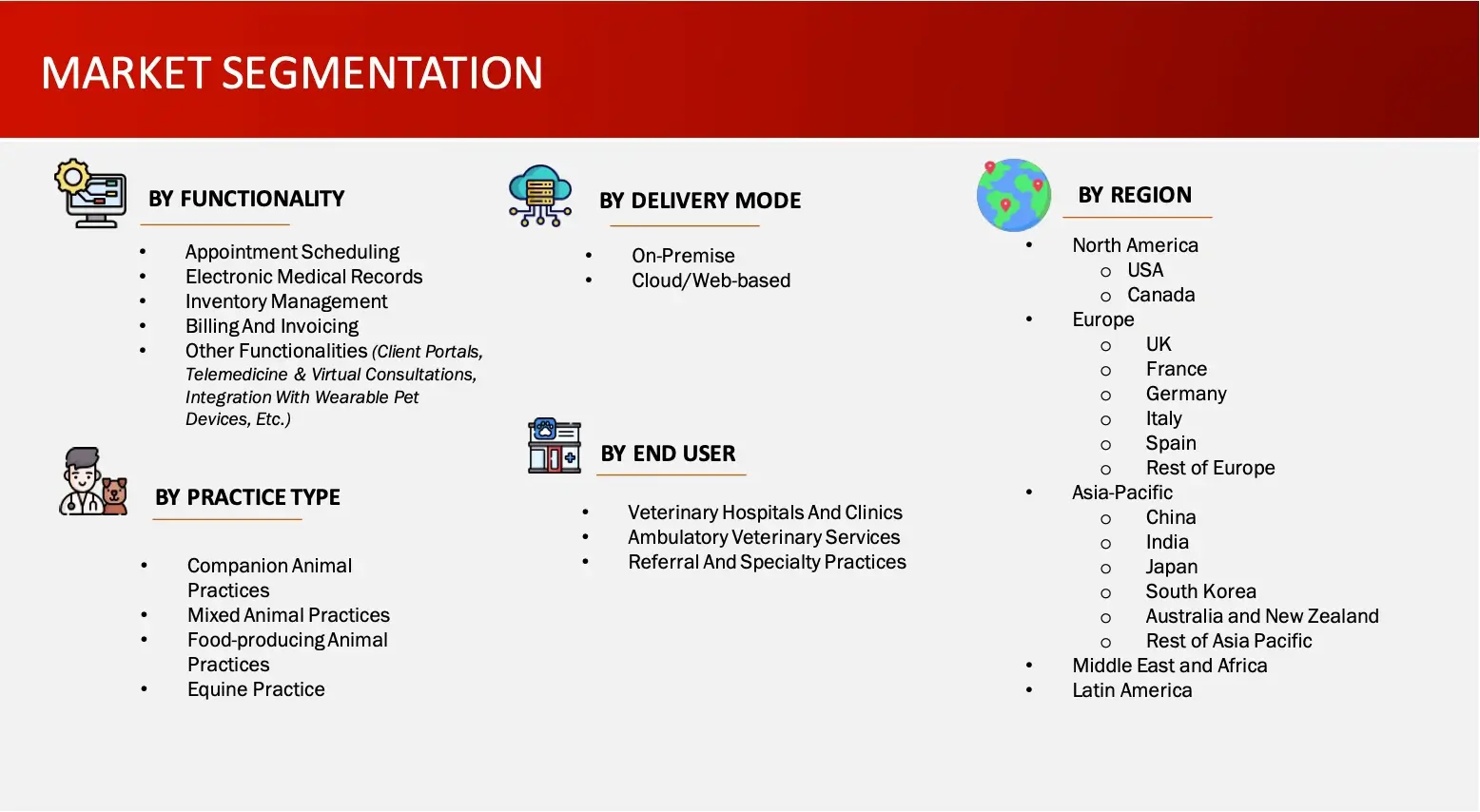

Key Segments | Veterinary Practice Management Software Market Functionality Outlook (Appointment Scheduling, Electronic Medical Records, Inventory Management, Billing and Invoicing, Other Functionalities) Other Functionalities include Client Portals, Telemedicine & Virtual Consultations, Integration with Wearable Pet Devices, etc. Veterinary Practice Management Software Market Practice Type Outlook (Companion Animal Practices, Mixed Animal Practices, Food-producing Animal Practices, Equine Practice) Veterinary Practice Management Software Market Delivery Mode Outlook (On-Premise, Cloud/Web-based) Veterinary Practice Management Software Market End User Outlook (Veterinary Hospitals and Clinics, Ambulatory Veterinary Services, Referral and Specialty Practices) |

Regions Covered | § North America: US and Canada § Europe: Germany, UK, France, Italy, Spain, and Rest of the Europe § Asia-Pacific: China, Japan, India, South Korea, Australia and New Zealand, and Rest of the Asia-Pacific § Latin America § Middle East and Africa |

Key Players Covered (Majority Share Holders) | Idexx Laboratories, Inc. (US), Covetrus, Inc. (US), Hippo Manager Software, Inc. (US), Advanced Technology Corp. (US), Vetport LLC. (US), Daysmart Software (US), Amerisourcebergen Corporation (US), Animal Intelligence Software Inc. (US), Firmcloud Corp. (US), Clien Trax (US), Ezofficesystems Ltd. (Canada), Shepherd Veterinary Software (US), Digitail (Romania), Provet (Nordhealth) (Finland), Onwardvet (US), Asteris (US), Carestream Health (US), Heska Corporation (Mars Inc.) (US) |

Other Players | Oehm Und Rehbein GMBH (Germany), Vetstoria (UK), Instinct Science, LLC (US), Planmeca OY (Finland) |

1. INTRODUCTION

1.1. KEY OBJECTIVES

1.2. DEFINITIONS

1.2.1. IN SCOPE

1.2.2. OUT OF SCOPE

1.3. SCOPE OF THE REPORT

1.4. SCOPE RELATED LIMITATIONS

1.5. KEY STAKEHOLDERS

2. RESEARCH METHODOLOGY

2.1. RESEARCH APPROACH

2.2. RESEARCH METHODOLOGY / DESIGN

2.3. MARKET SIZE ESTIMATION APPROACHES

2.3.1. SECONDARY RESEARCH

2.3.2. PRIMARY RESEARCH

2.3.2.1. KEY INSIGHTS FROM INDUSTRY EXPERTS

2.4. DATA VALIDATION & TRIANGULATION

2.5. ASSUMPTIONS OF THE STUDY

3. EXECUTIVE SUMMARY & PREMIUM CONTENT

3.1. GLOBAL MARKET OUTLOOK

3.2. KEY MARKET FINDINGS

4. MARKET OVERVIEW

4.1. VETERINARY PRACTICE MANAGEMENT SOFTWARE: OVERVIEW

4.1.1. INTRODUCTION

4.1.2.KEY FEATURES AND FUNCTIONALITIES

4.1.3.BENEFITS FOR VETERINARY PRACTICE MANAGEMENT SOFTWARES

4.1.4.TYPES OF VETERINARY PRACTICE MANAGEMENT SOFTWARE

4.2. MARKET DYNAMICS

4.2.1. MARKET DRIVERS

4.2.2. MARKET OPPORTUNITIES

4.2.3. RESTRAINTS/CHALLENGES

4.3. END USER PERCEPTION

4.4. NEED GAP ANALYSIS

4.5. SUPPLY CHAIN / VALUE CHAIN ANALYSIS

4.6. INDUSTRY TRENDS

4.7. PORTER’S FIVE FORCES ANALYSIS

4.8. REGULATORY LANDSCAPE

4.8.1.NORTH AMERICA

4.8.2.EUROPE

4.8.3.ASIA PACIFIC

5. PATENT ANALYSIS

5.1. TOP ASSIGNEES

5.2. GEOGRAPHY FOCUS OF TOP ASSIGNEES

5.3. LEGAL STATUS

5.4. TECHNOLOGY EVOLUTION

5.5. KEY PATENTS

5.6. PATENT TRENDS AND INNOVATIONS

6. GLOBAL VETERINARY PRACTICE MANAGEMENT SOFTWARE MARKET BY FUNCTIONALITY (2025-2030, USD MILLION)

6.1. APPOINTMENT SCHEDULING

6.2. ELECTRONIC MEDICAL RECORDS

6.3. INVENTORY MANAGEMENT

6.4. BILLING AND INVOICING

6.5. OTHER FUNCTIONALITIES (CLIENT PORTALS, TELEMEDICINE & VIRTUAL CONSULTATIONS, INTEGRATION WITH WEARABLE PET DEVICES, ETC.)

7. GLOBAL VETERINARY PRACTICE MANAGEMENT SOFTWARE MARKET BY PRACTICE TYPE (2025-2030, USD MILLION)

7.1. COMPANION ANIMAL PRACTICES

7.2. MIXED ANIMAL PRACTICES

7.3. FOOD-PRODUCING ANIMAL PRACTICES

7.4. EQUINE PRACTICE

8. GLOBAL VETERINARY PRACTICE MANAGEMENT SOFTWARE MARKET BY DELIVERY MODE (2025-2030, USD MILLION)

8.1. ON-PREMISE

8.2. CLOUD/WEB-BASED

9. GLOBAL VETERINARY PRACTICE MANAGEMENT SOFTWARE MARKET BY END-USER (2025-2030, USD MILLION)

9.1. VETERINARY HOSPITALS AND CLINICS

9.2. AMBULATORY VETERINARY SERVICES

9.3. REFERRAL AND SPECIALTY PRACTICES

10. GLOBAL VETERINARY PRACTICE MANAGEMENT SOFTWARE MARKET BY REGION (2025-2030, USD MILLION)

10.1. NORTH AMERICA

10.1.1. US

10.1.2. CANADA

10.2. EUROPE

10.2.1. GERMANY

10.2.2. FRANCE

10.2.3. SPAIN

10.2.4. ITALY

10.2.5. UK

10.2.6. REST OF THE EUROPE

10.3. ASIA-PACIFIC

10.3.1. CHINA

10.3.2. JAPAN

10.3.3. INDIA

10.3.4. AUSTRALIA AND NEW ZEALAND

10.3.5. SOUTH KOREA

10.3.6. REST OF THE ASIA-PACIFIC

10.4. MIDDLE EAST AND AFRICA

10.5. LATIN AMERICA

11. COMPETITIVE ANALYSIS

11.1. PRODUCT PIPELINE: VETERINARY PRACTICE MANAGEMENT SOFTWARES

11.2. KEY PLAYERS FOOTPRINT ANALYSIS

11.3. MARKET SHARE ANALYSIS (2023/2024)

11.4. REGIONAL SNAPSHOT OF KEY PLAYERS

11.5. R&D EXPENDITURE OF KEY PLAYERS

12. COMPANY PROFILES

12.1. IDEXX LABORATORIES, INC. (US)

12.1.1. BUSINESS OVERVIEW

12.1.2. PRODUCT PORTFOLIO

12.1.3. FINANCIAL SNAPSHOT

12.1.4. RECENT DEVELOPMENTS

12.1.4.1. MERGER/ACQUISITIONS

12.1.4.2. PRODUCT APPROVAL/LAUNCHES

12.1.4.3. PARTNERSHIP/COLLABORATIONS/AGREEMENTS

12.1.4.4. EXPANSIONS

12.2. COVETRUS, INC. (US)

12.3. HIPPO MANAGER SOFTWARE, INC. (US)

12.4. ADVANCED TECHNOLOGY CORP. (US)

12.5. VETPORT LLC. (US)

12.6. DAYSMART SOFTWARE (US)

12.7. AMERISOURCEBERGEN CORPORATION (US)

12.8. ANIMAL INTELLIGENCE SOFTWARE INC. (US)

12.9. FIRMCLOUD CORP. (US)

12.10. CLIEN TRAX (US)

12.11. EZOFFICESYSTEMS LTD. (Canada)

12.12. SHEPHERD VETERINARY SOFTWARE (US)

12.13. DIGITAIL (Romania)

12.14. PROVET (NORDHEALTH) (Finland)

12.15. ONWARDVET (US)

12.16. ASTERIS (US)

12.17. CARESTREAM HEALTH (US)

12.18. HESKA CORPORATION (MARS INC.) (US)

12.19. OTHER PLAYERS

12.19.1. OEHM UND REHBEIN GMBH (Germany)

12.19.2. VETSTORIA (UK)

12.19.3. INSTINCT SCIENCE, LLC (US)

12.19.4. PLANMECA OY (Finland)

13. APPENDIX

13.1. INDUSTRY SPEAK

13.2. QUESTIONNAIRE/DISCUSSION GUIDE

13.3. AVAILABLE CUSTOM WORK

13.4. ADJACENT STUDIES

13.5. AUTHORS

14. REFERENCES

The veterinary practice management software market comprises specialized software solutions designed to help veterinary clinics, hospitals, and specialized care facilities efficiently manage their daily operations. These solutions integrate various functionalities such as appointment scheduling, electronic medical records, billing and invoicing, inventory management, and client communication. The market includes both on-premise and cloud/web-based delivery models, catering to different veterinary practice types including companion animal, mixed animal, food-producing animal, and equine practices. The software aims to streamline workflows, enhance patient care, reduce errors, and improve operational efficiency while supporting features like telemedicine and remote consultations. Driven by rising pet ownership, technological advancements such as AI and cloud computing, and increasing demand for specialized veterinary services, the market is witnessing significant global growth and digital transformation across veterinary practices.

FIGURE: VETERINARY PRACTICE MANAGEMENT SOFTWARE MARKET SEGMENTS

Sources: Company Websites and Wissen Research Analysis

Key Stakeholders

Key Study Objectives

Research Methodology

The objective of the study is to analyze the key market dynamics such as drivers, opportunities, challenges, restraints, and key player strategies. To track company developments such as product launches and approvals, expansions, and collaborations of the leading players, the competitive landscape of the veterinary practice management software market to analyze market players on various parameters within the broad categories of business and product strategy. Top-down and bottom-up approaches will be used to estimate the market size. To estimate the market size of segments and sub segments the market breakdown and data triangulation will be used.

FIGURE: RESEARCH DESIGN

Sources: Wissen Research Analysis

Research Approach

Collecting Secondary Data

The secondary research data collection process involves the usage of secondary sources, directories, databases, annual reports, investor presentations, and SEC filings of companies. Secondary research will be used to identify and collect information useful for the extensive, technical, market-oriented, and commercial study of the veterinary practice management software market. A database of the key industry leaders will also be prepared using secondary research.

Collecting Primary Data

The primary research data will be conducted after acquiring knowledge about the veterinary practice management software market scenario through secondary research. A significant number of primary interviews will be conducted with stakeholders from both the demand side and supply side (including various industry experts, such as Directors, Chief X Officers (CXOs), Vice Presidents (VPs) from business development, marketing and product development teams, product manufacturers) across major countries of North America, Europe, Asia Pacific, and Rest of the World. Primary data for this report was collected through questionnaires, emails, and telephonic interviews.

Market Size Estimation

All major developers offering various veterinary practice management software will be identified at the global/regional level. Revenue mapping will be done for the major players, which will further be extrapolated to arrive at the global market value of each type of segment. The market value of veterinary practice management software market will also split into various segments and sub segments at the region level based on:

Research Design

After arriving at the overall market size-using the market size estimation processes-the market will be split into several segments and sub segment. To complete the overall market engineering process and arrive at the exact statistics of each market segment and sub segment, the data triangulation, and market breakdown procedures will be employed, wherever applicable. The data will be triangulated by studying various factors and trends from both the demand and supply sides in the veterinary practice management software market.